I tend to agree with this update from Art.

The global equity sell off seems beyond anything related to the S&P downgrade

and more likely China and commodity related. Note the recent fall in the $A for example.

There’s a new post on our site discussing the terrible performance of Asian stock markets this morning, on the first major trading day following Standard & Poor’s downgrade of the U.S. government’s credit rating. The media is widely assuming the selloff in Asia is all related to the downgrade, but I think that’s a pretty flimsy argument. Seems more likely to be related to China and/or Europe. We’ll have a better idea once European markets open. The post is linked and excerpted below. If you have any questions or concerns, let me know. Have a great week!

Asia Down Big: US Downgrade or China Cracking?

Market chatter has been focused on the impact that Standard & Poor’s downgrade of U.S. government’s credit rating on Friday afternoon would have on markets this week. If you follow our blog, you already know where we stand on S&P’s decision—it’s an utter joke. And while other markets have shown some volatility since Friday, it didn’t seem to have much of a negative impact. That’s as we expected.

However, Asian markets sold off brutally at the start of this week’s trading. The knee-jerk media interpretation is that it’s S&P-driven, but that’s not a satisfying explanation in my view. Given how the sell-offs are unfolding, it looks like it could be China-related. The Shanghai stock market is now officially in bear market territory, and smart market watchers have been predicting that China could soon experience a financial crisis, as its system is reportedly quite levered-up and fragile.

If so, this is NOT good for the global economic and risky asset outlooks. Throw one more nut on the bear claw. And China is a big nut—a lot of companies around the world depend on demand out of China, either directly or indirectly, to support current operating performance. Take that down significantly and stock market valuations suddenly look a lot richer.

Of course, it could be Europe too. And we’ve recently seen short-term interest rates go negative, an occurrence that presaged the last global financial crisis. We’re keeping a close eye on things as they unfold.

+++

In other news, Friday saw what appeared to be rather healthy payrolls and consumer credit reports. However, digging below the headlines, temporary hirings (along with measures of temp help demand from other sources) are still falling, and they tend to lead payrolls higher or lower. And underlying trends in consumer confidence indicate that the notable jump in consumer credit, though it could run for another few quarters, should be short-lived.

Work that I did with some of our strategy models over the weekend indicates that recession is going to be almost a sure thing as July and August data is fed in, and we’re currently predicting a start date between February 2012 and January 2013. Also looks, based on NYSE margin data, like the S&P 500 could fall another 10% to 30% from here, with a bear market running from May 2011 (some would date it back to 2007) through as late as mid-2013. A bear market starting roughly half a year before recession would fit historical patterns rather well, unfortunately.

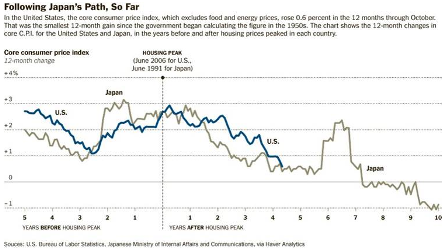

One piece that is arguing emphatically against recession is the Treasury curve, which is still historically steep after last week’s flattening. However, (1) Japan’s first follow-on recession started with the term spread at around 200 basis points (unheard of up until then) and it has had two additional recessions without its yield curve ever inverting, and (2) we simply don’t expect term spreads to have much predictive power in a zero interest rate environment. Interbank funding in the U.S. is still at safe levels, but there are definitely incipient signs of stress. Everything else is on the verge of triggering a recession warning.

Depending upon what unfolds in China, Europe, and the upcoming U.S. austerity negotiations (and the ever-present unknown unknowns), recession could unfold far sooner and faster than almost anyone thinks. Forceful policy actions could do a great deal to stem the tide, but there seems to be almost no political will to do anything, probably due to the mistaken belief that governments everywhere are ‘out of bullets’.

At levels below 900 on the S&P500, we would probably start to lean heavily toward equities—unless a balanced budget amendment to the U.S. Constitution makes significant progress, in which case we’ll recommend cash and long-term Treasuries across all or most of our clients’ accounts.

Best regards,

Art

IMPORTANT DISCLOSURES: Symmetry Capital Management, LLC (“SCM”) is a Pennsylvania registered investment advisor that offers discretionary investment management to individuals and institutions. This publication is for informational, educational, and entertainment purposes only. It is not an offer to sell or a solicitation to buy securities, or to engage in any investment strategy. The firm and some of its clients hold some positions that are expected to increase in value if stock markets decline.