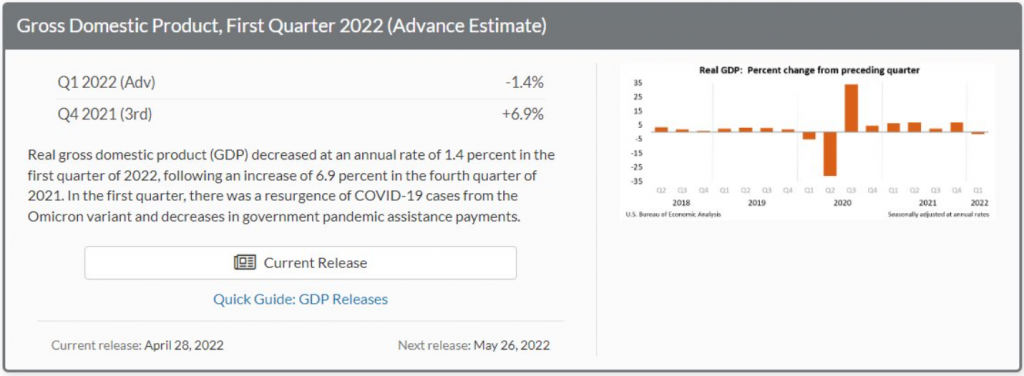

Post-war collapse theme intact:

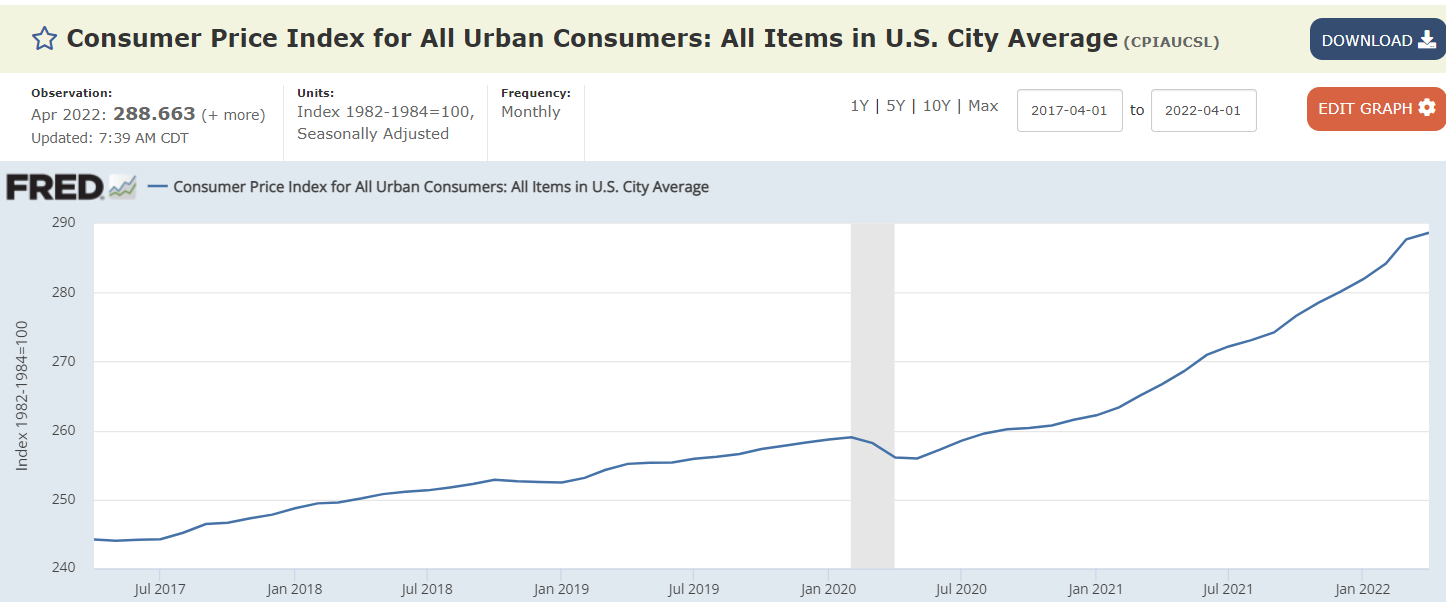

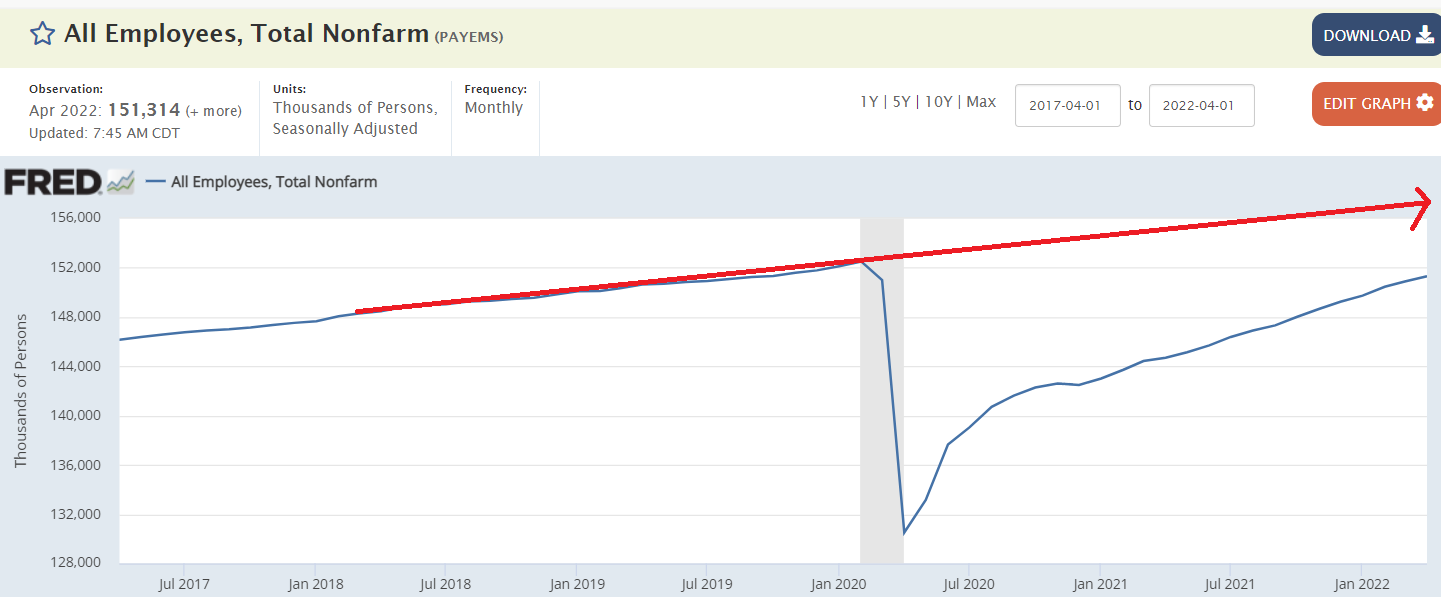

Falling back to the pre-Covid war trend line:

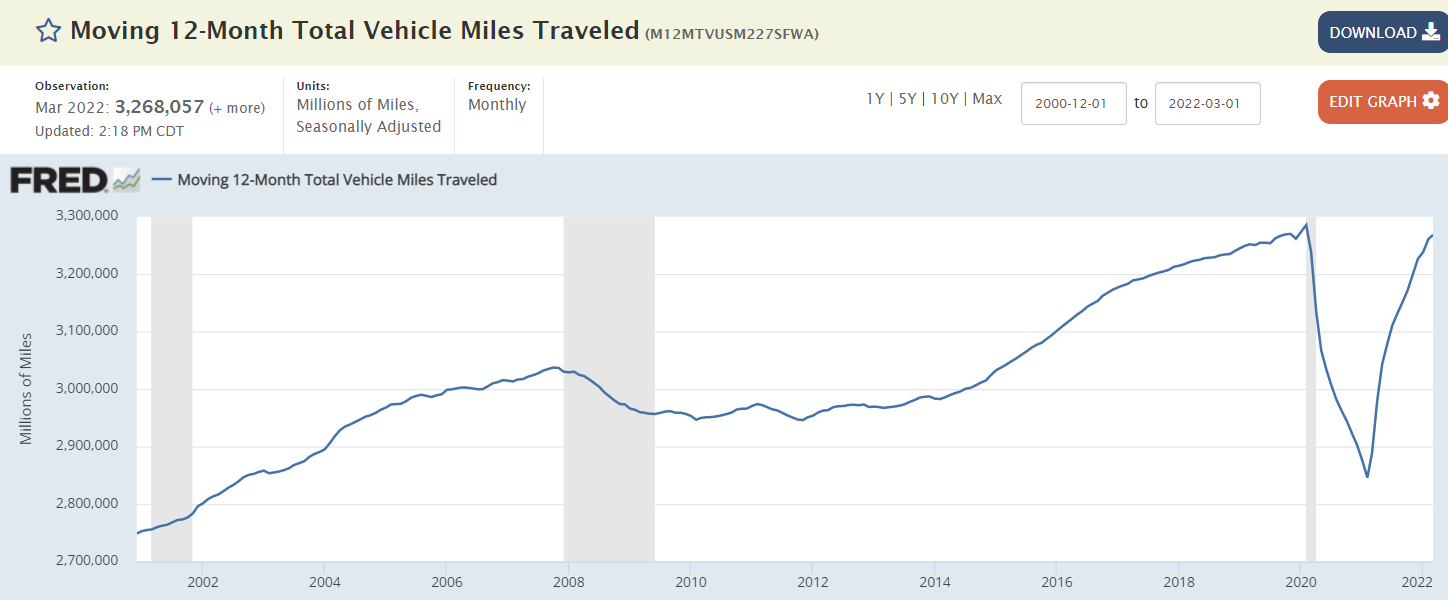

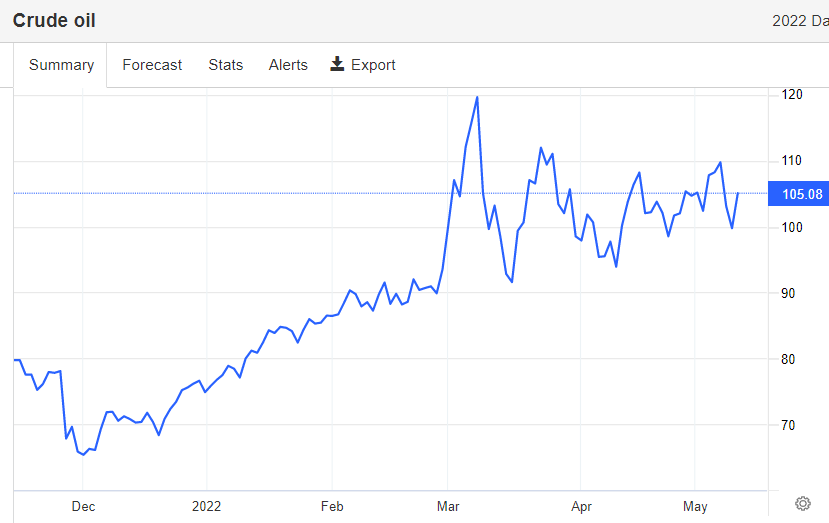

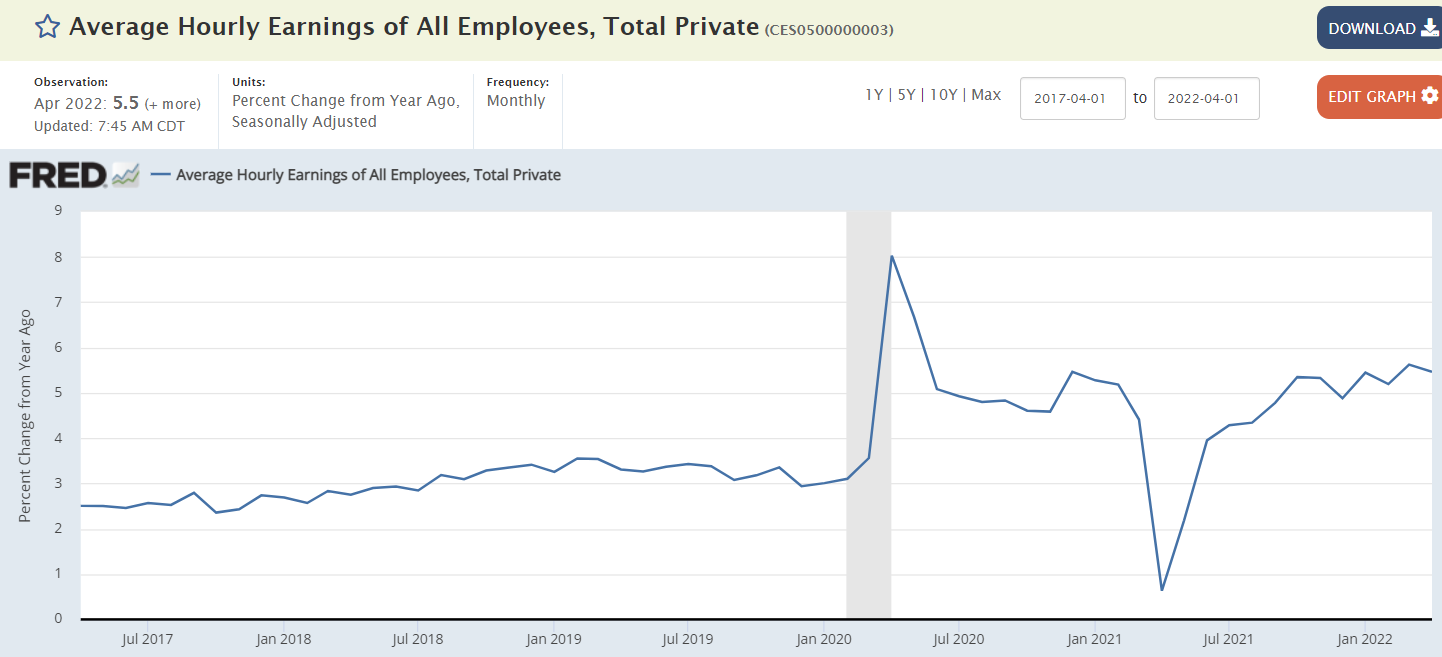

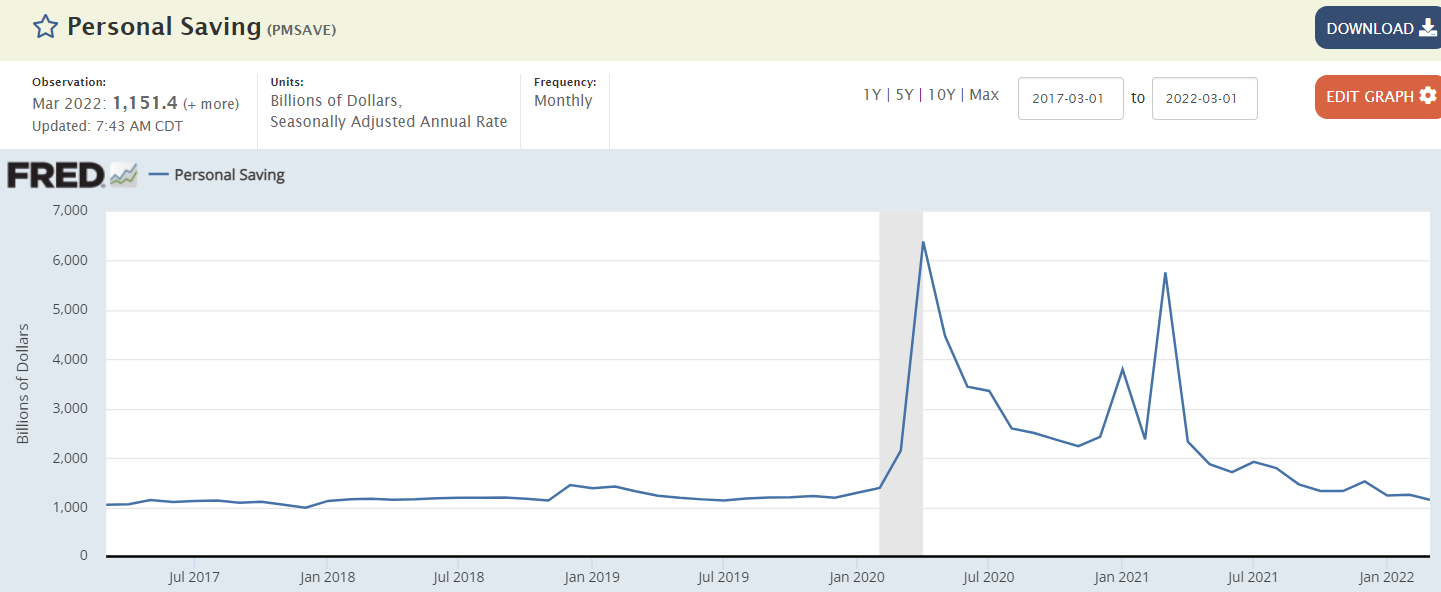

We’re back burning fuel with abandon:

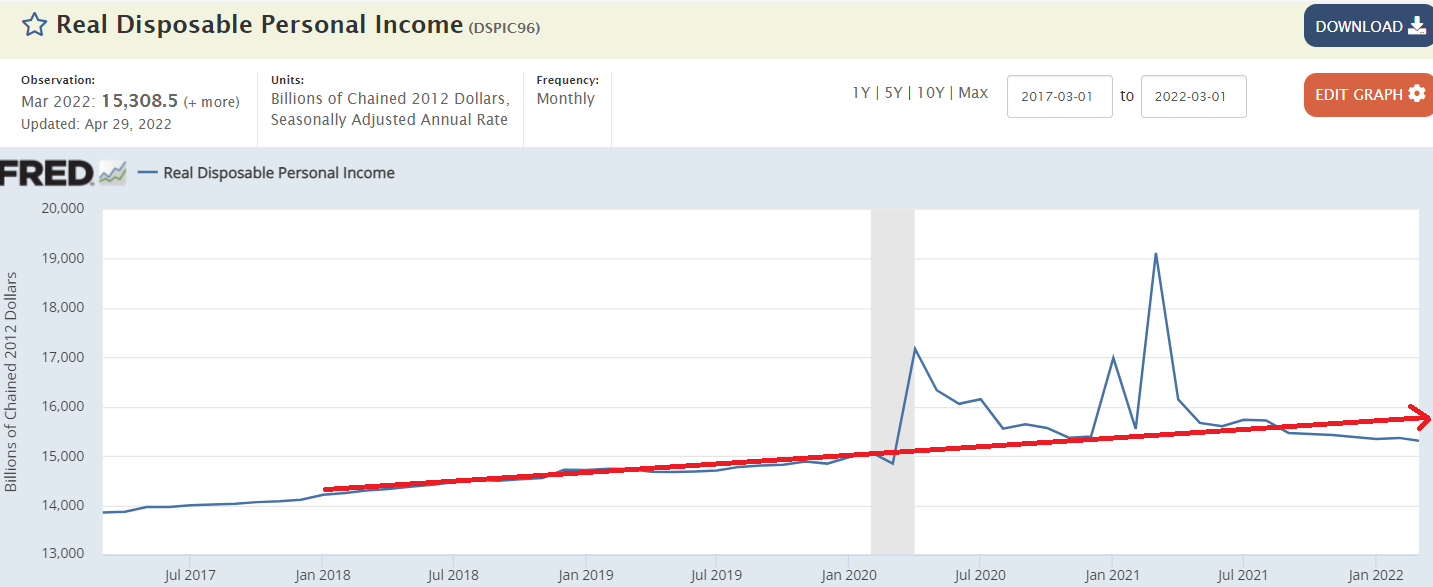

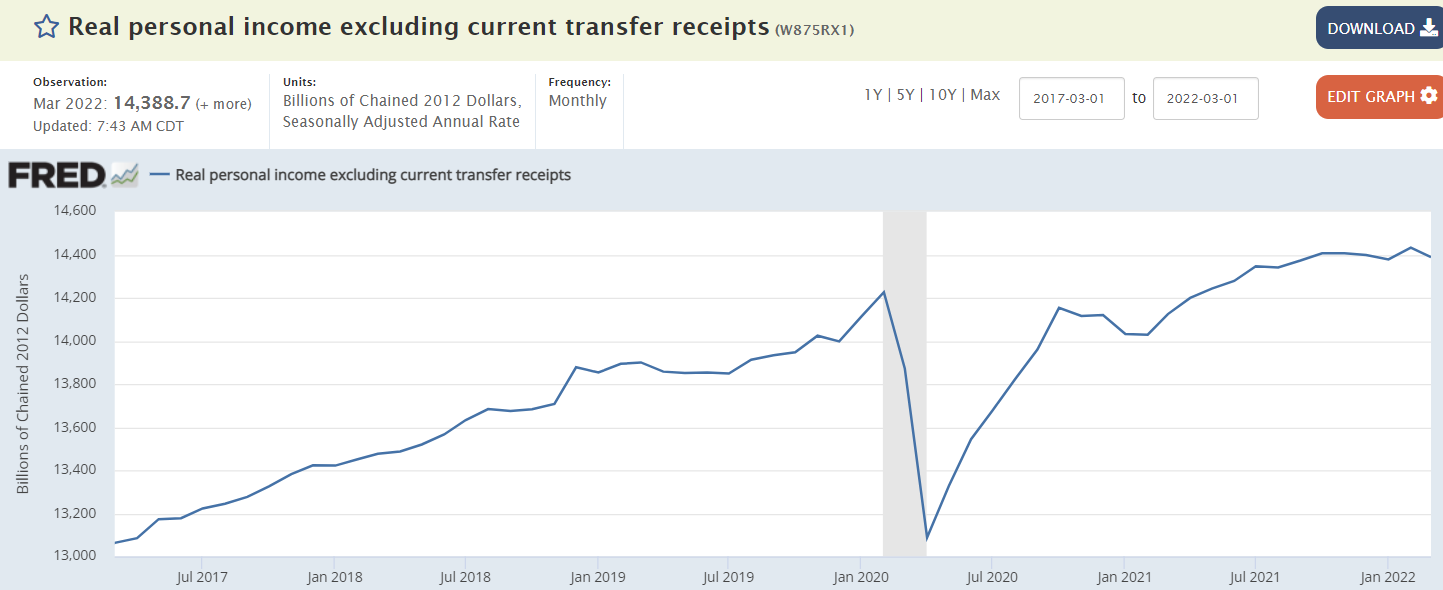

Not growing when adjusted for inflation:

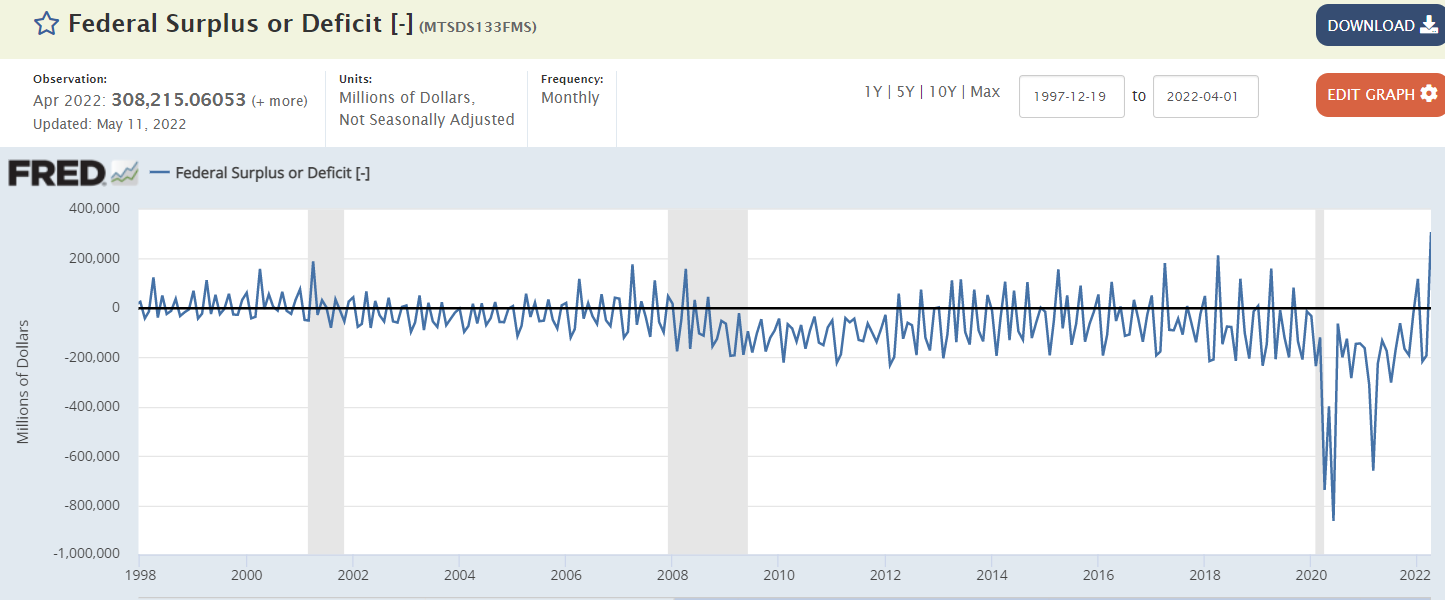

The US posted a budget surplus of USD 308 billion in April of 2022, the highest on record, switching from a USD 226 billion gap in the same period last year and above market expectations of a USD 226 billion surplus. April has traditionally been a budget surplus month due to the traditional April 15 tax filing deadline, except in 2009, 2010 and 2011 after a financial crisis, and in 2020 and 2021 due to the Covid-19 pandemic. Receipts jumped 97 percent to an all-time high of USD 864 billion, underpinned by tax receipts on the back of a strong economic recovery. At the same time, outlays slumped 16 percent to USD 555 billion, reflecting lower spending for COVID-19 relief. For the first seven months of the 2022 fiscal year, the US federal deficit was at USD 360 billion, a 81 percent decline from the same period of fiscal 2021. source: Financial Management Service, US Treasury Monthly Treasury Statement

My take is we’ve had a one time upward adjustment in prices due to increased costs from Covid-related supply issues, along with supply side disruptions from the Trump/Biden tariffs.

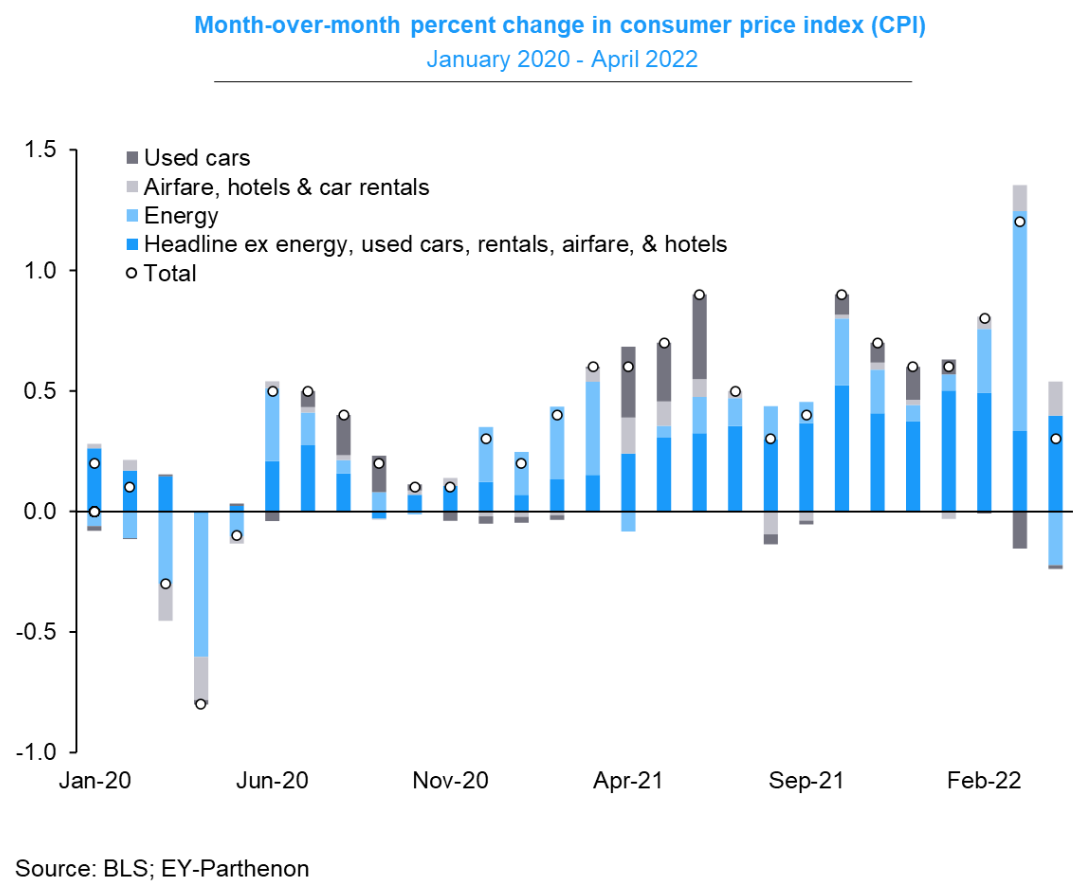

Prices seem to have begun to level off and go sideways, which would mean CPI increases returning to the lower, pre-Covid monthly increases:

However, if energy costs don’t level off and instead rise dramatically, CPI will be dragged upward as well:

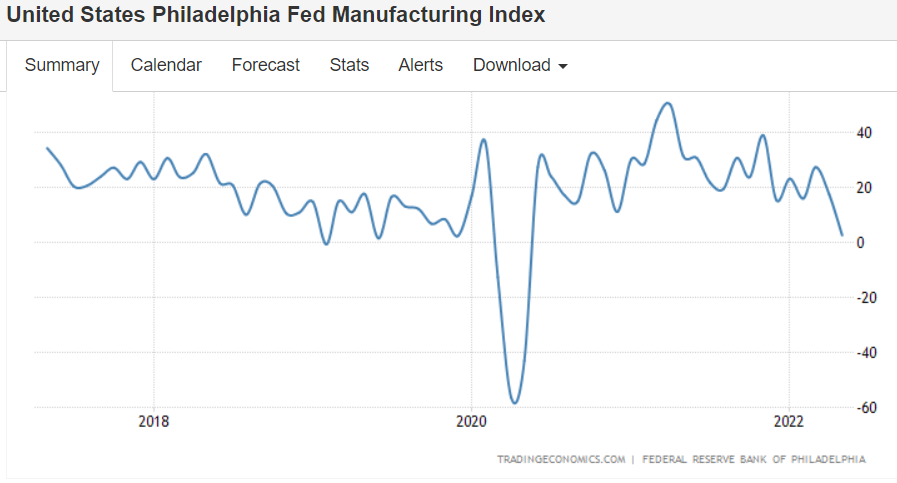

Typical post war recession type of outcome, as previously discussed:

One reason for the low unemployment in the US is that for a lot of people you need a job to get health insurance:

https://tradingeconomics.com/united-states/jobless-claims

Reported inflation will fall rapidly unless energy prices increase from current levels,

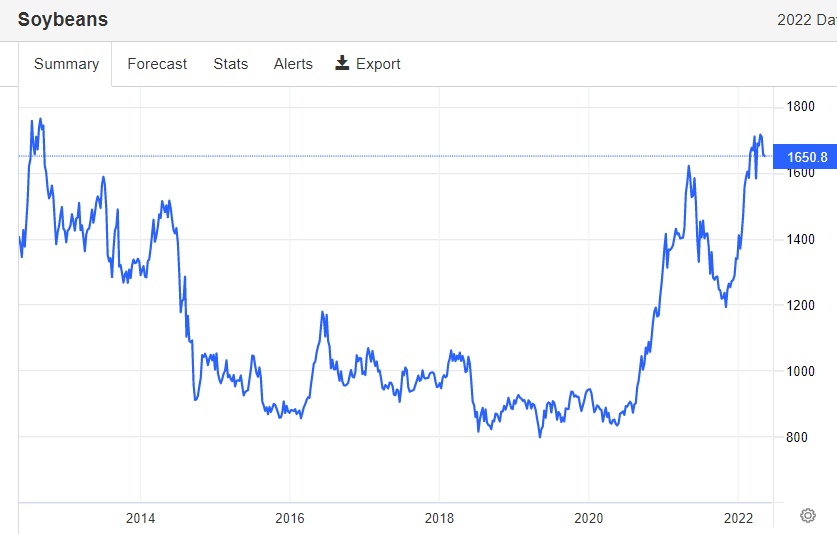

which is likely given current Saudi OSP’s and EU responses to the war:

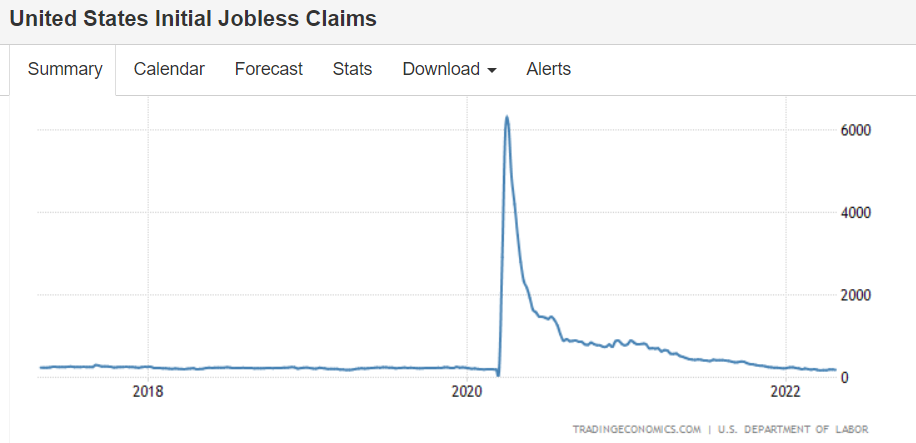

A bit of an uptick but still trending lower:

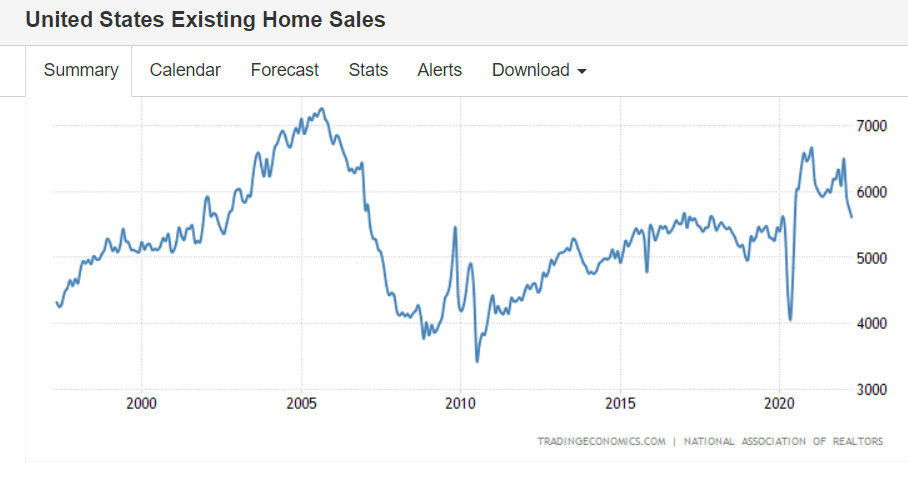

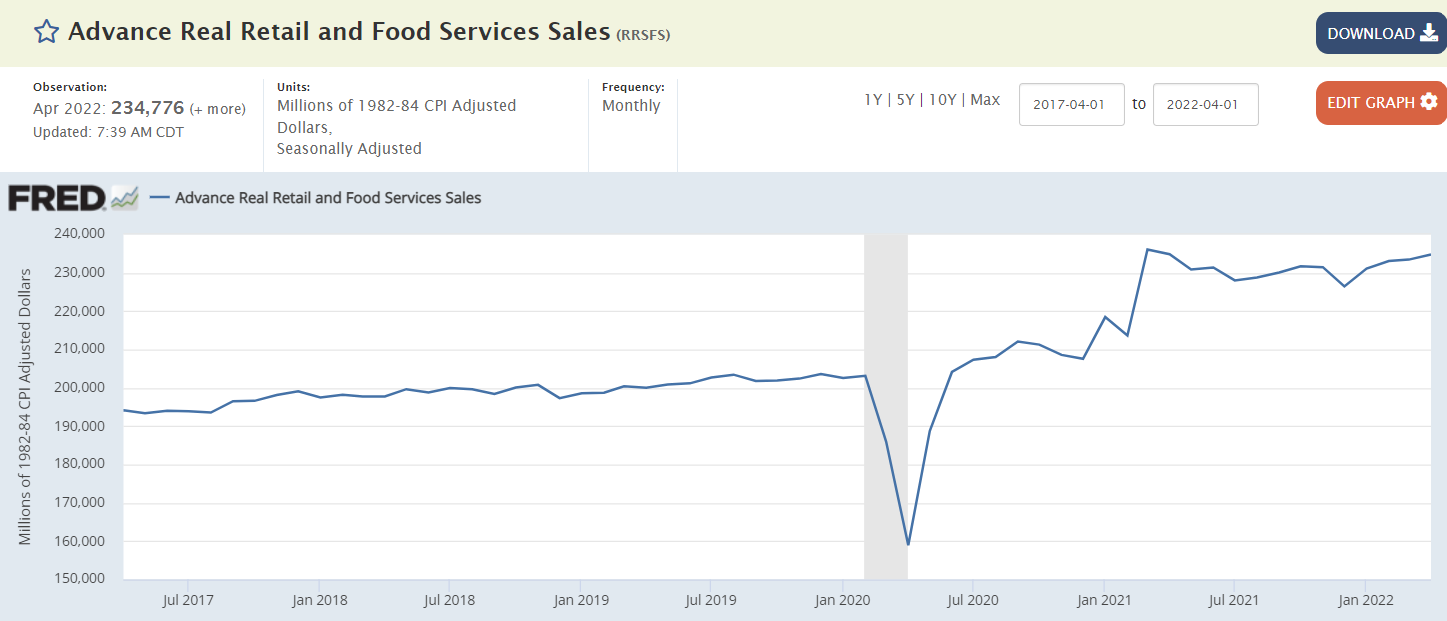

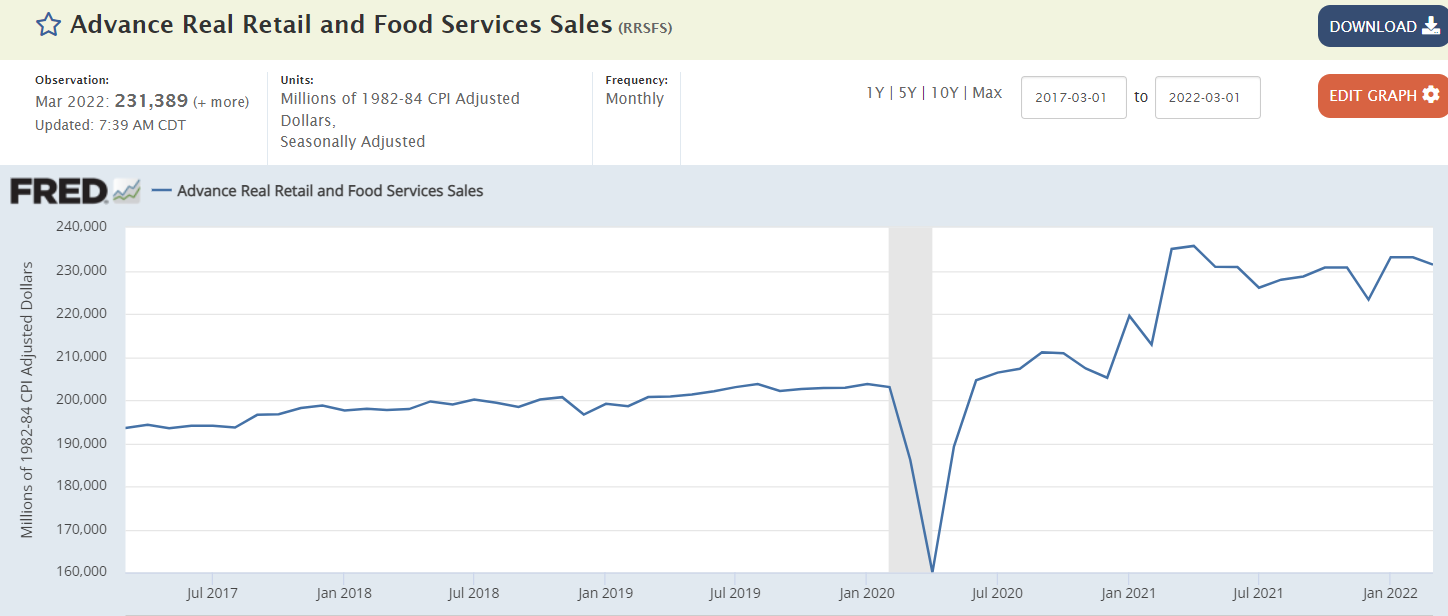

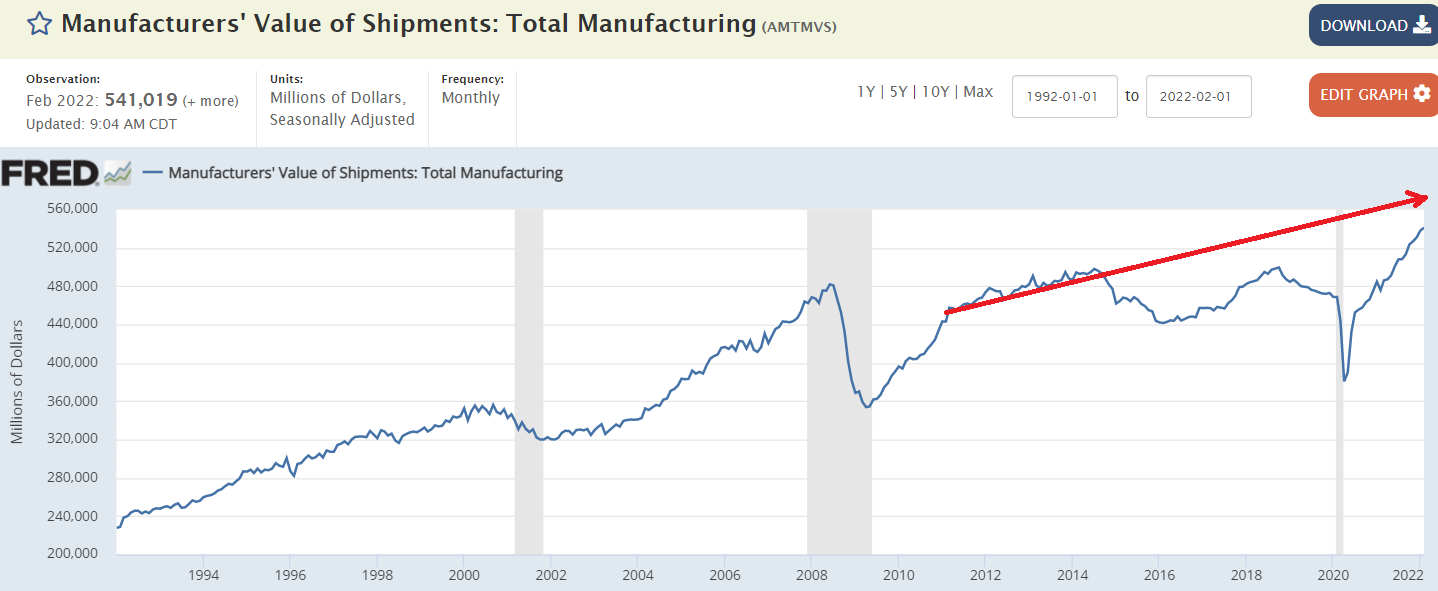

Sales going sideways on an inflation adjusted basis:

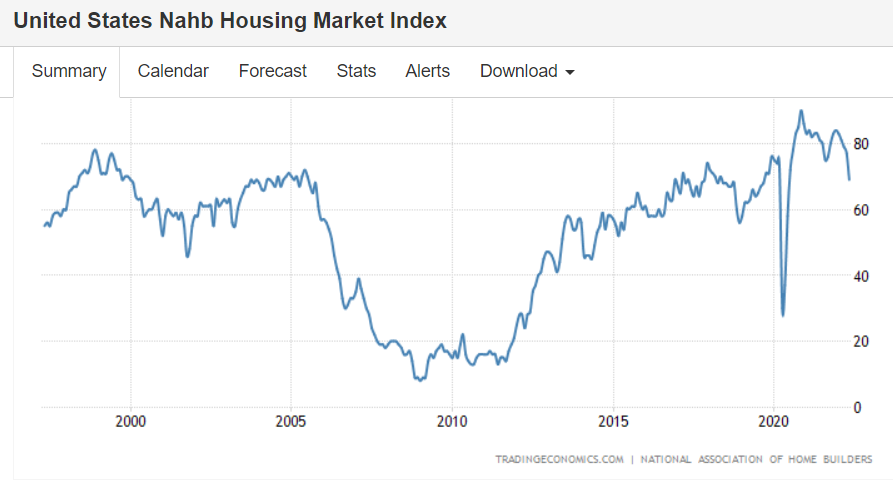

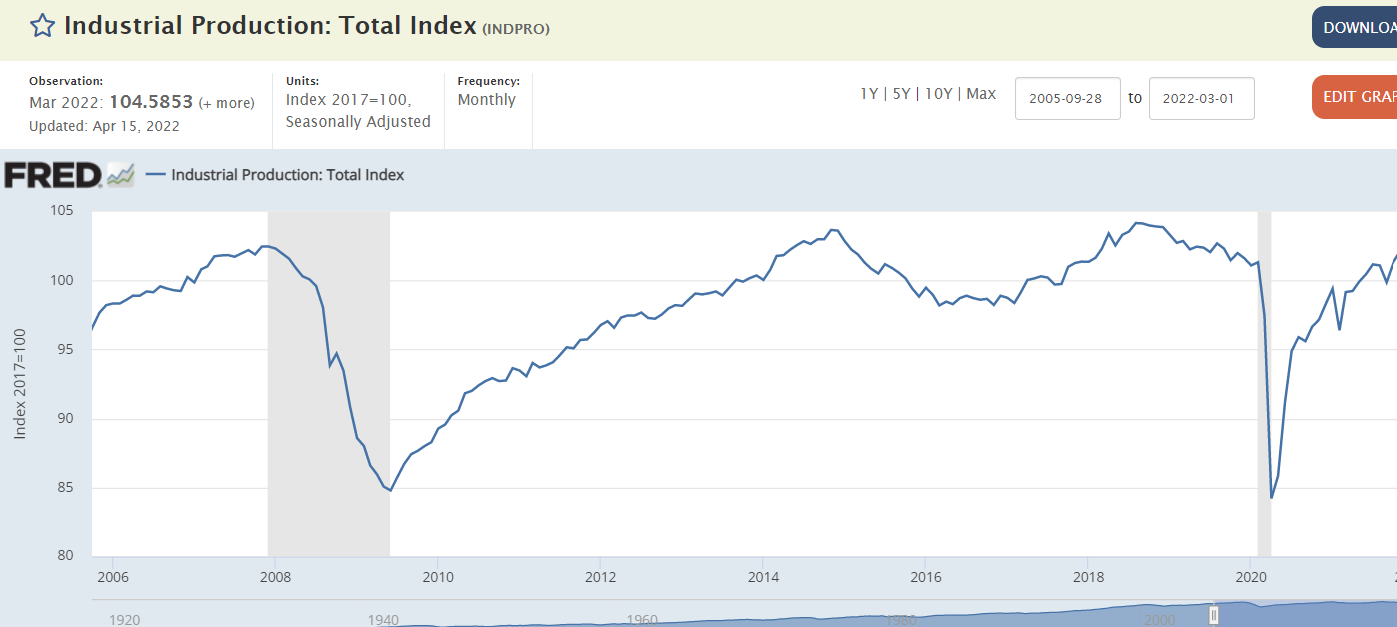

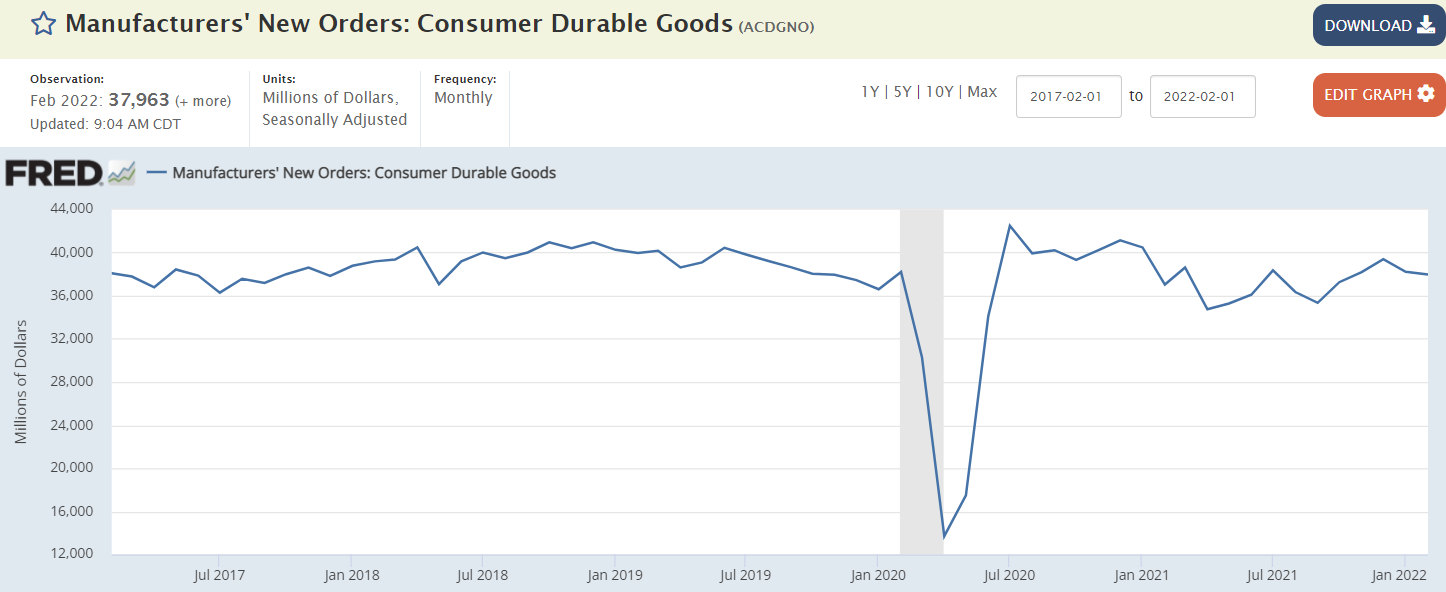

This sector seems to be doing ok:

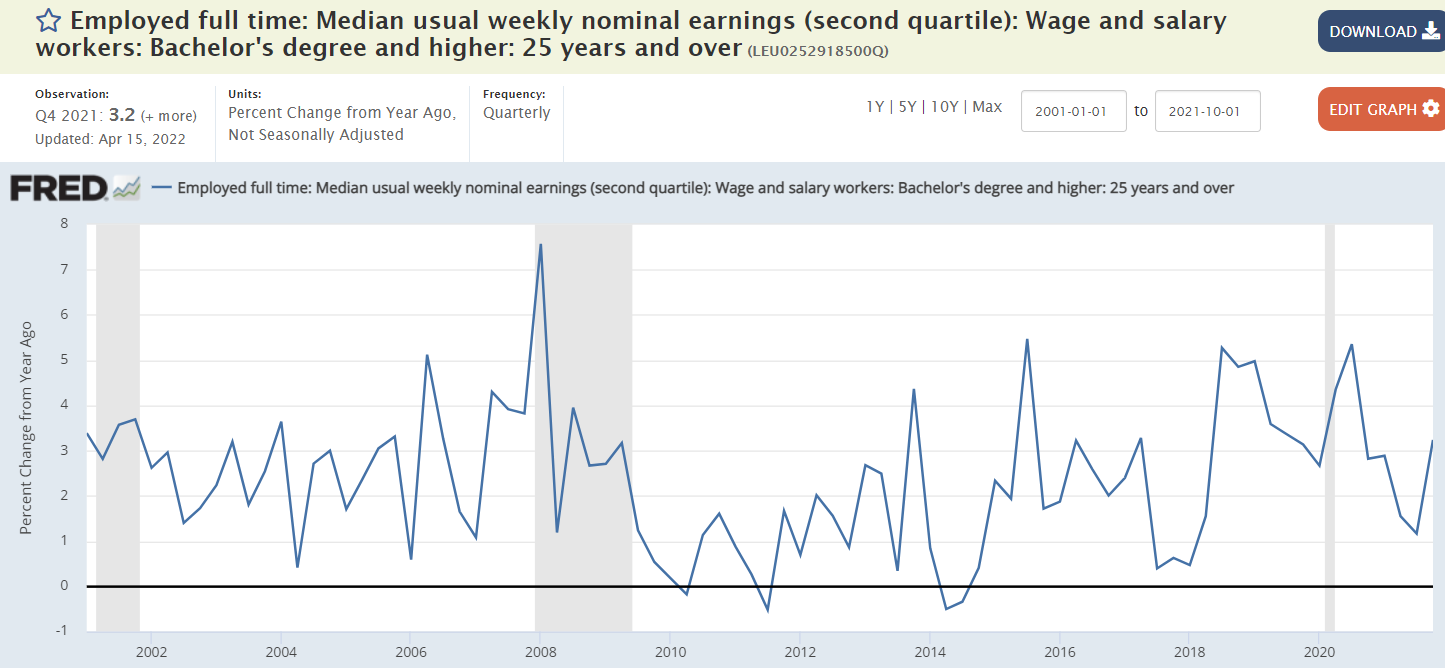

Not keeping up with inflation so probably not causing it:

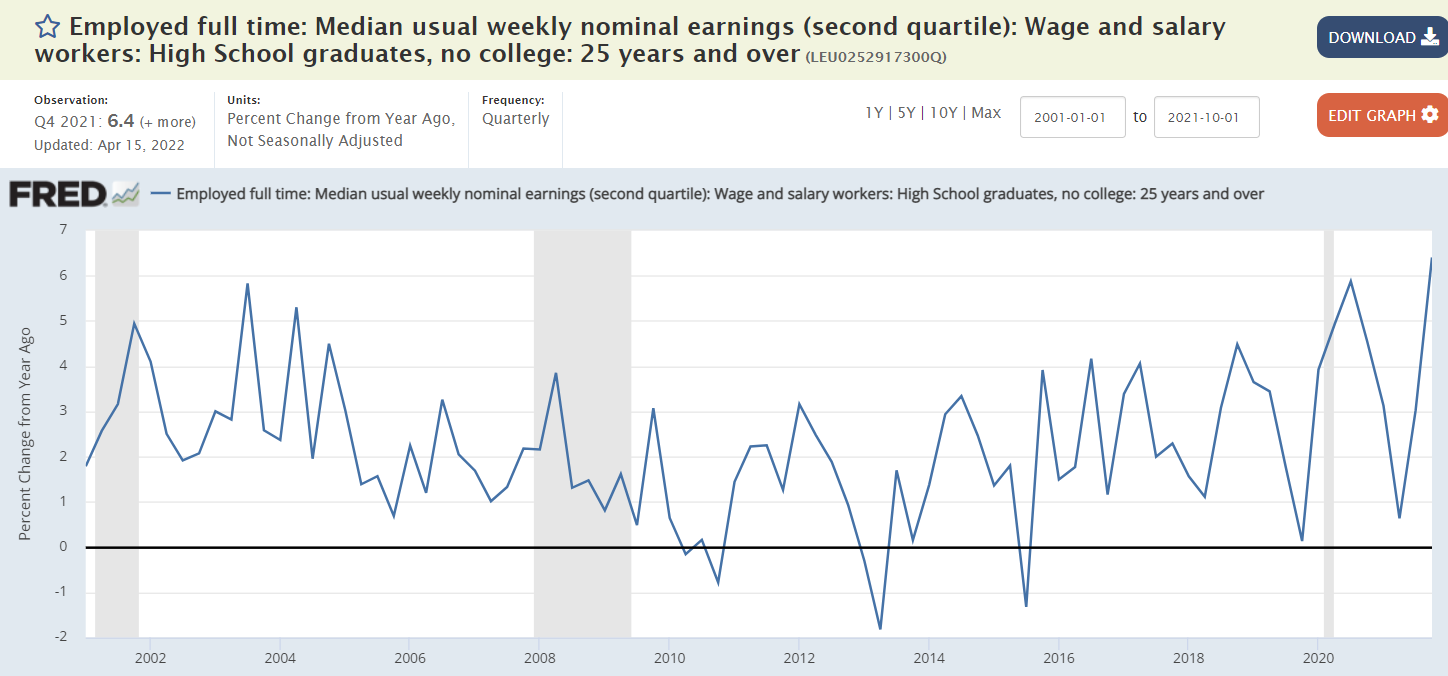

Lowest income earners (no college) have been catching up some, but also lagging inflation:

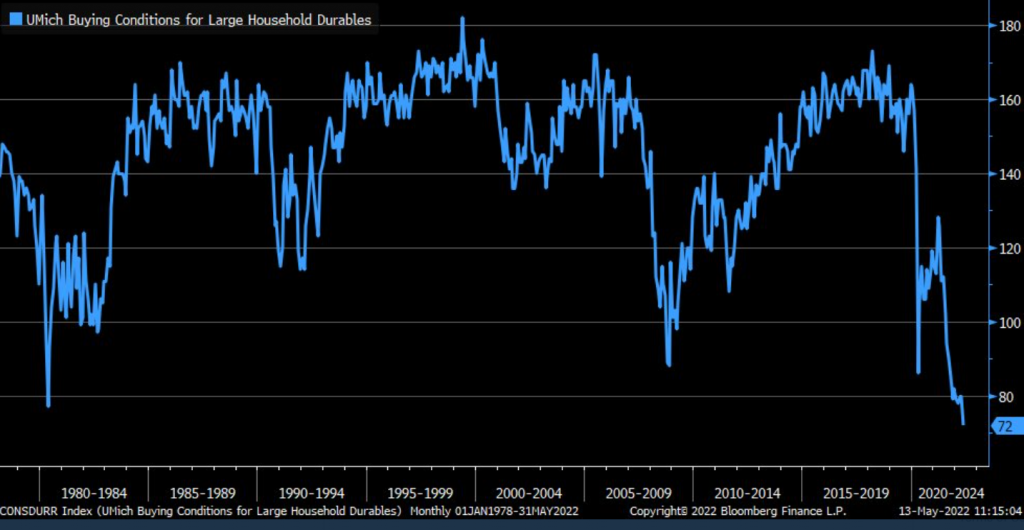

This component is going nowhere:

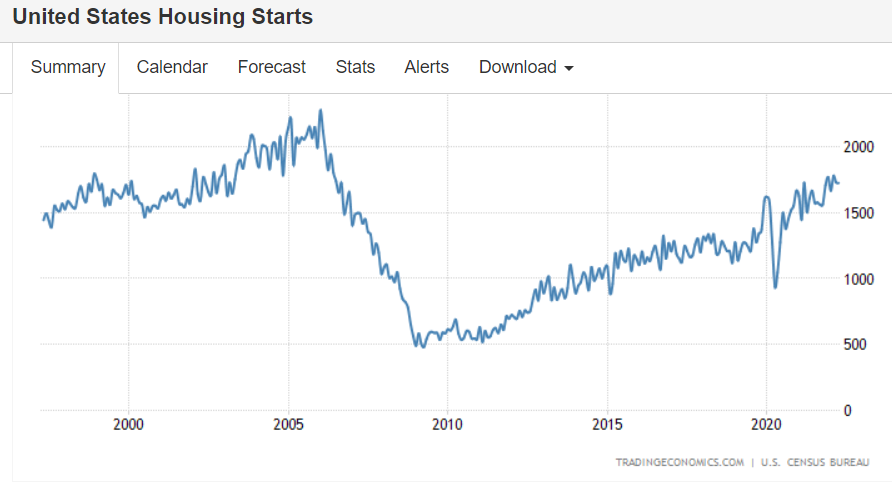

Still trying to catch up from the oil capex collapse of 2016 and covid collapse:

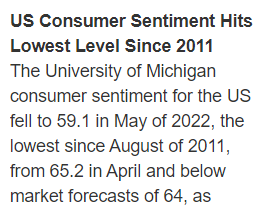

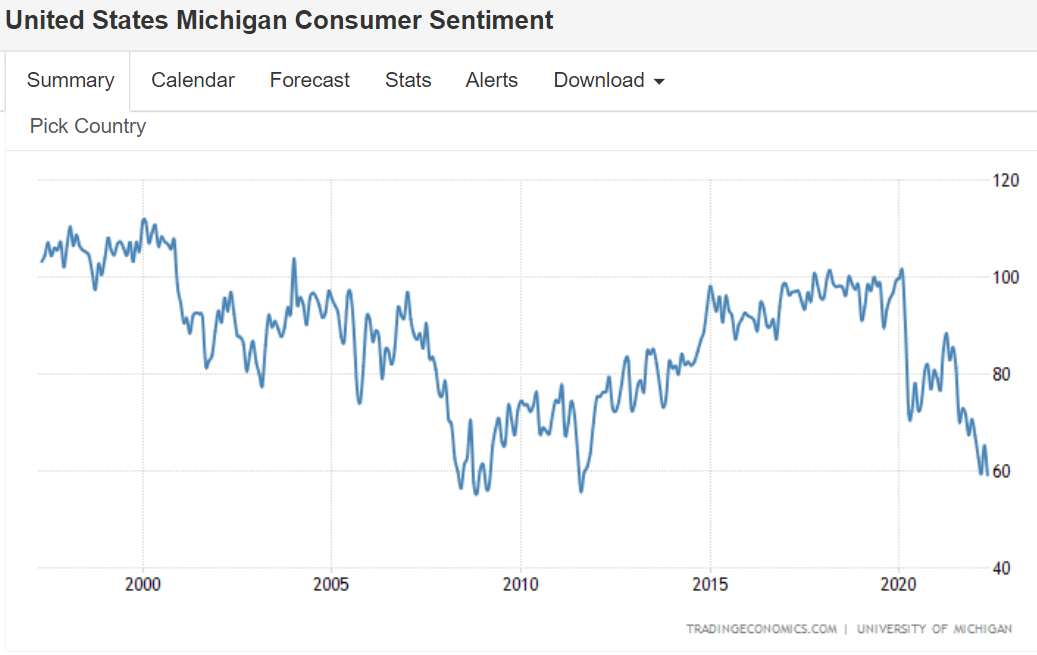

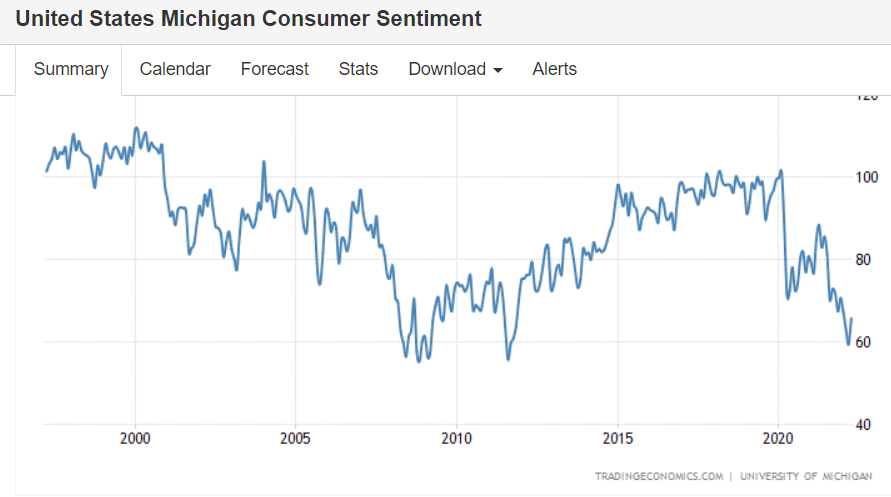

Not good:

This is an all time low as people scramble to get extra jobs to deal with higher prices,

like paying rent, for example:

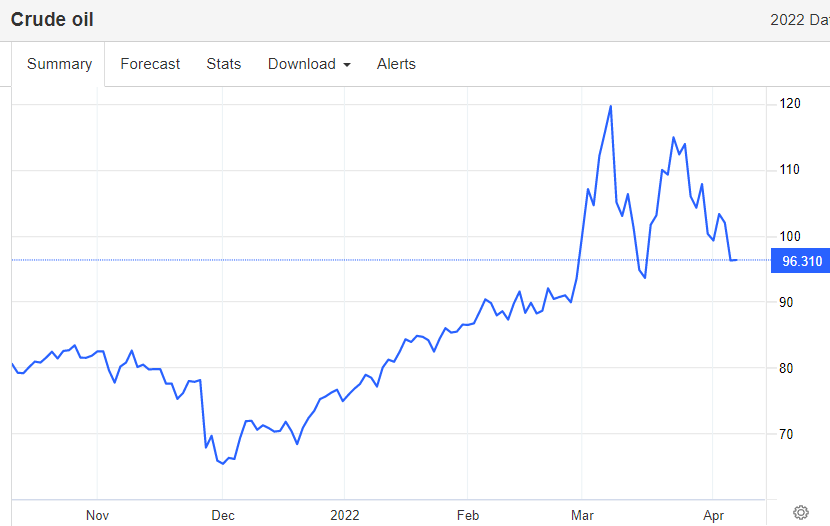

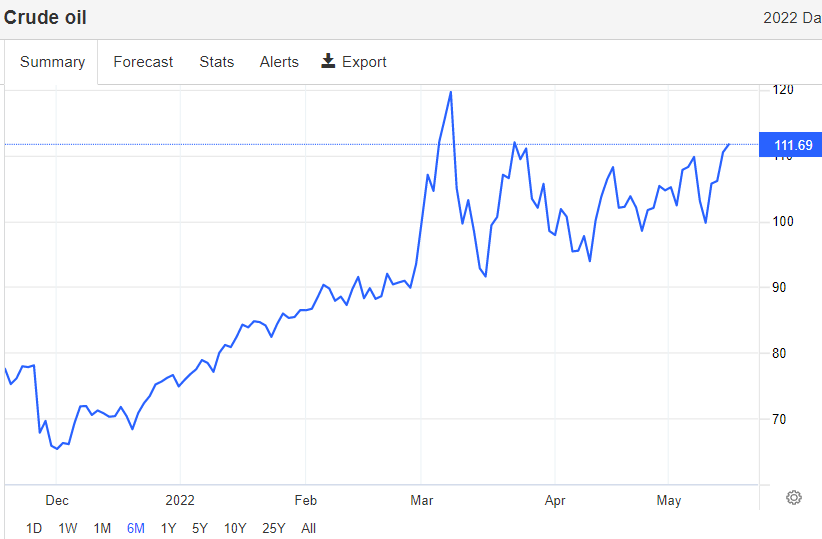

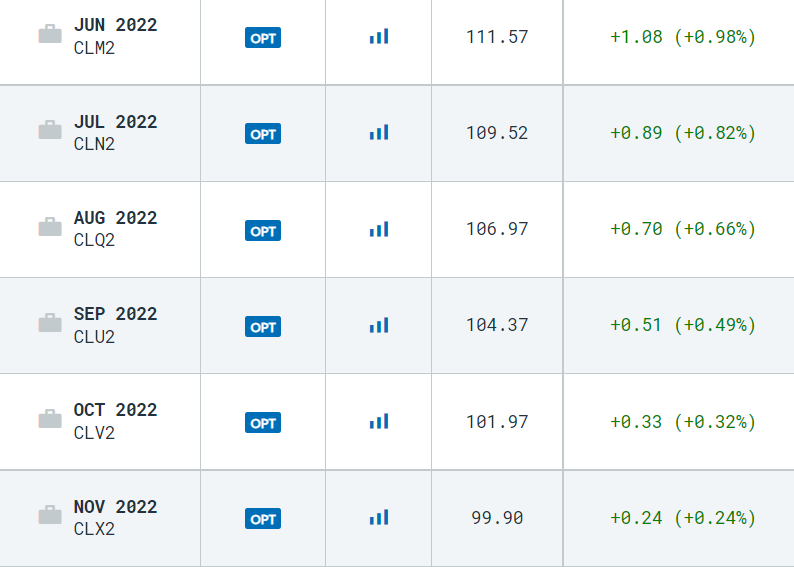

Oil prices taking a breather with the announcements of releases from strategic petroleum reserves.

Price direction, however, is instead set by Saudi OSP premiums to benchmarks which were just raised for the 3rd month and this time to record highs.

This puts a relentless upward bias to prices until Saudi pricing changes, and will propel what’s call inflation as well. And the higher prices can also trigger a sharp recession: