So I see this:

More Signs of Sturdy Growth: Consumer Spending Rises

March 29 (Reuters) — U.S. consumer spending rose in February and income rebounded, further signs economic activity accelerated in the first quarter, even though part of the increase in consumption reflected higher gasoline prices.

The Commerce Department said on Friday consumer spending increased 0.7 percent last month after an upwardly revised 0.4 percent rise in January. Spending had previously been estimated to have increased 0.2 percent in January.

Economists polled by Reuters had expected spending, which accounts for about 70 percent of U.S. economic activity, to increase 0.6 percent last month.

After adjusting for inflation, spending was up 0.3 percent after advancing by the same margin in January.

While Americans paid 35 cents more for gasoline last month, they also bought long-lasting goods such as automobiles and spent more on services, thanks to a bounce-back in income growth.

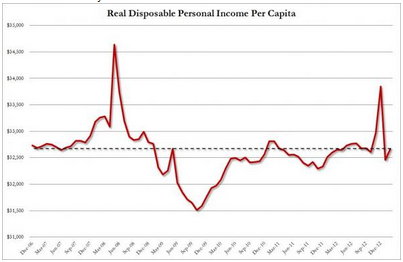

Income increased a healthy 1.1 percent after tumbling 3.7 percent in January.

“Both numbers are consistent with a continued recovery of the U.S. economy,” said Kathy Lien, managing director at BK Asset Management in New York.

A sustained pace of steady job gains is starting to boost wages, which should help to provide some cushion for households from higher taxes and support economic growth.

Personal income in December was sharply higher because of a rush to pay dividends and bonuses before tax hikes took effect this year. That also skewed data for January.

A 2 percent payroll tax cut expired on Jan. 1 and tax rates for wealthy Americans also went up. Data ranging from employment to factory activity has so far shown little sign the tighter fiscal policy has been a major drag on the economy.

First-quarter GDP growth estimates currently range as high as a 3.2 percent annual rate. The economy grew at only a 0.4 percent pace in the fourth quarter.

INFLATION GENERALLY MUTED

Last month, the income at the disposal of households after inflation and taxes increased 0.7 percent in February after dropping 4.0 percent in January.

With income growth outpacing spending, the saving rate – the percentage of disposable income households are socking away – rose to 2.6 percent from 2.2 percent in January.

The higher gasoline prices pushed up inflation, with a price index for consumer spending rising 0.4 percent after being flat for two straight months. February’s increase in the PCE index was the largest since August.

But a core reading that strips out food and energy costs rose only 0.1 percent after increasing 0.2 percent in January, showing no sign of underlying inflation pressures.

Over the past 12 months, inflation has risen 1.3 percent after rising by the same margin in the period through January.

Core prices were up 1.3 percent, well below the Federal Reserve’s 2 percent target. They also had risen 1.3 percent in the 12 months through January.

The benign inflation picture should give the U.S. central bank room to continue with its monetary stimulus as it seeks to boost job growth.

The Fed said last week it would maintain its monthly $85 billion purchases of mortgage and Treasury bonds until it saw a substantial improvement in the job market.

Then this: