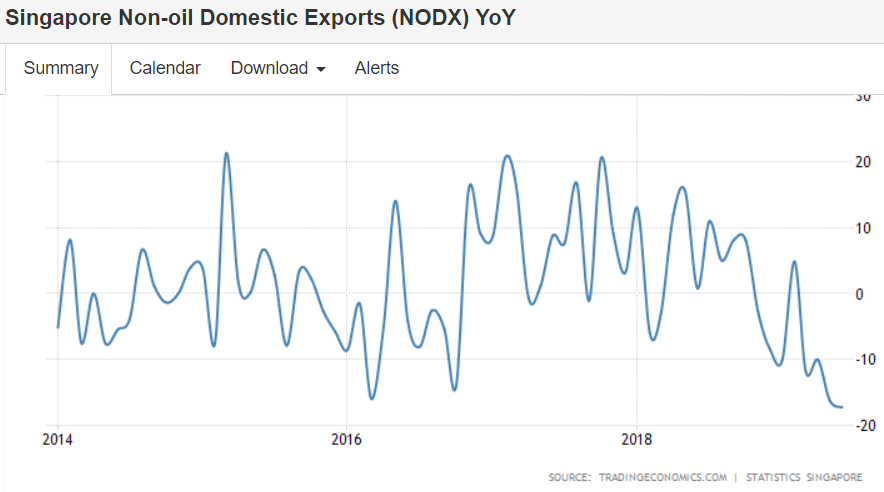

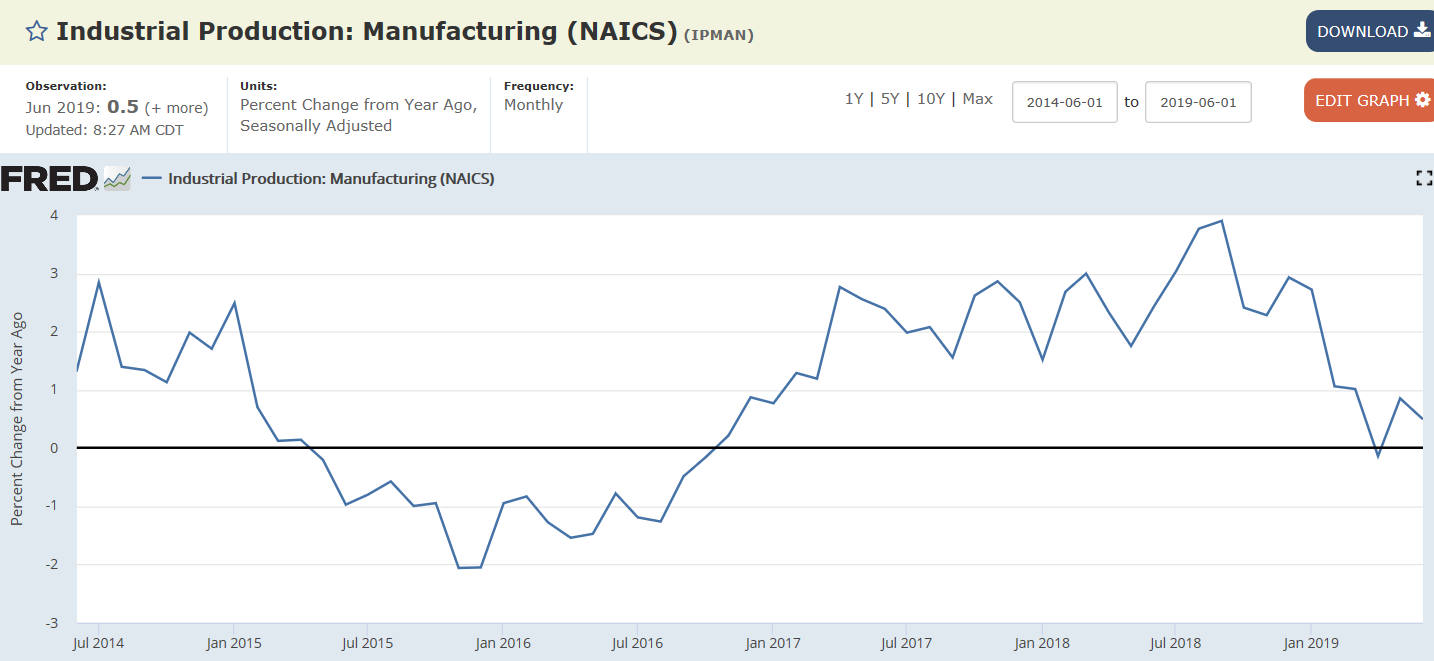

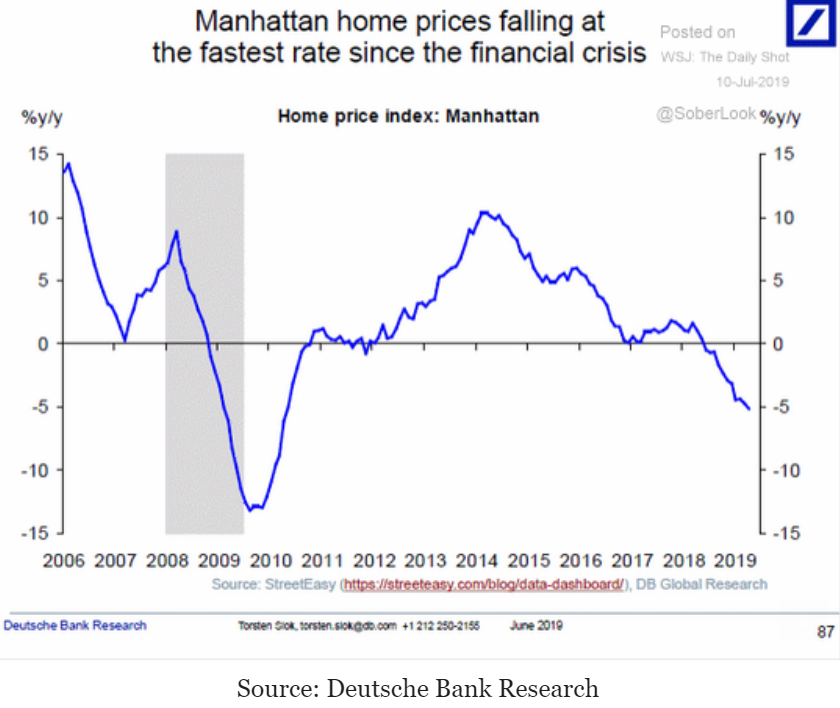

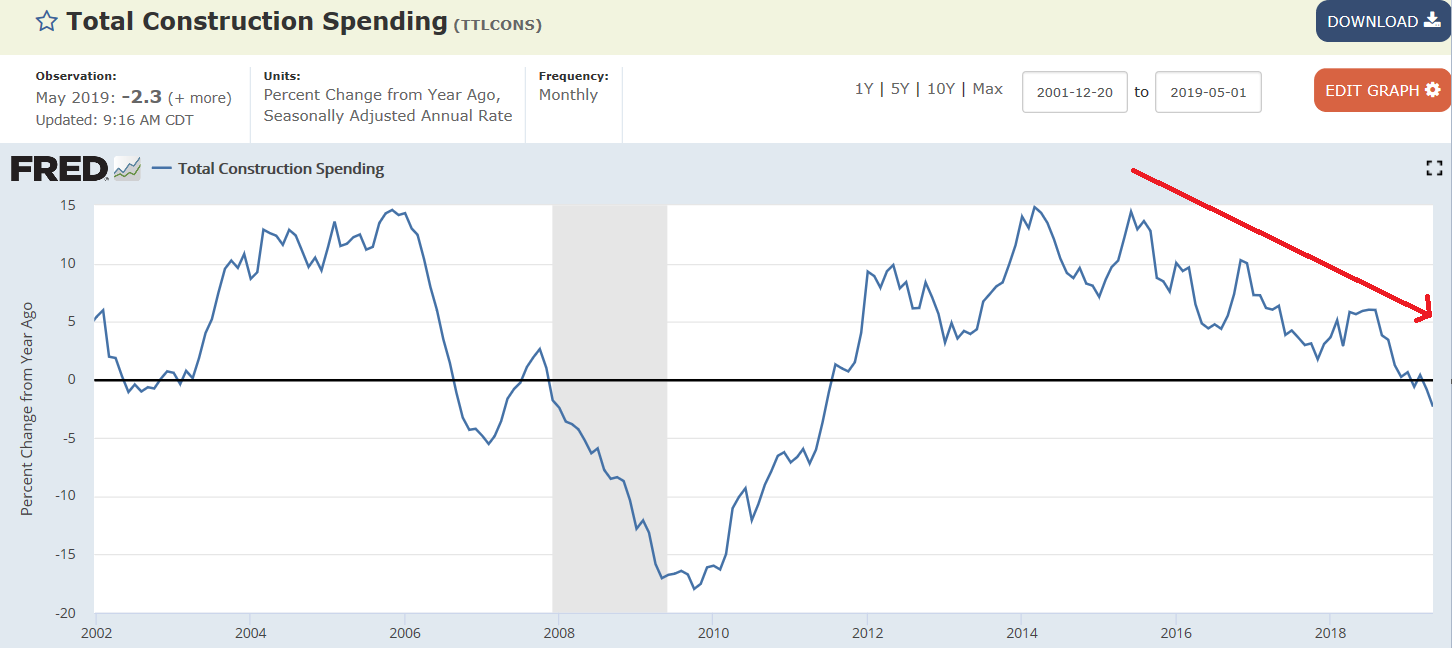

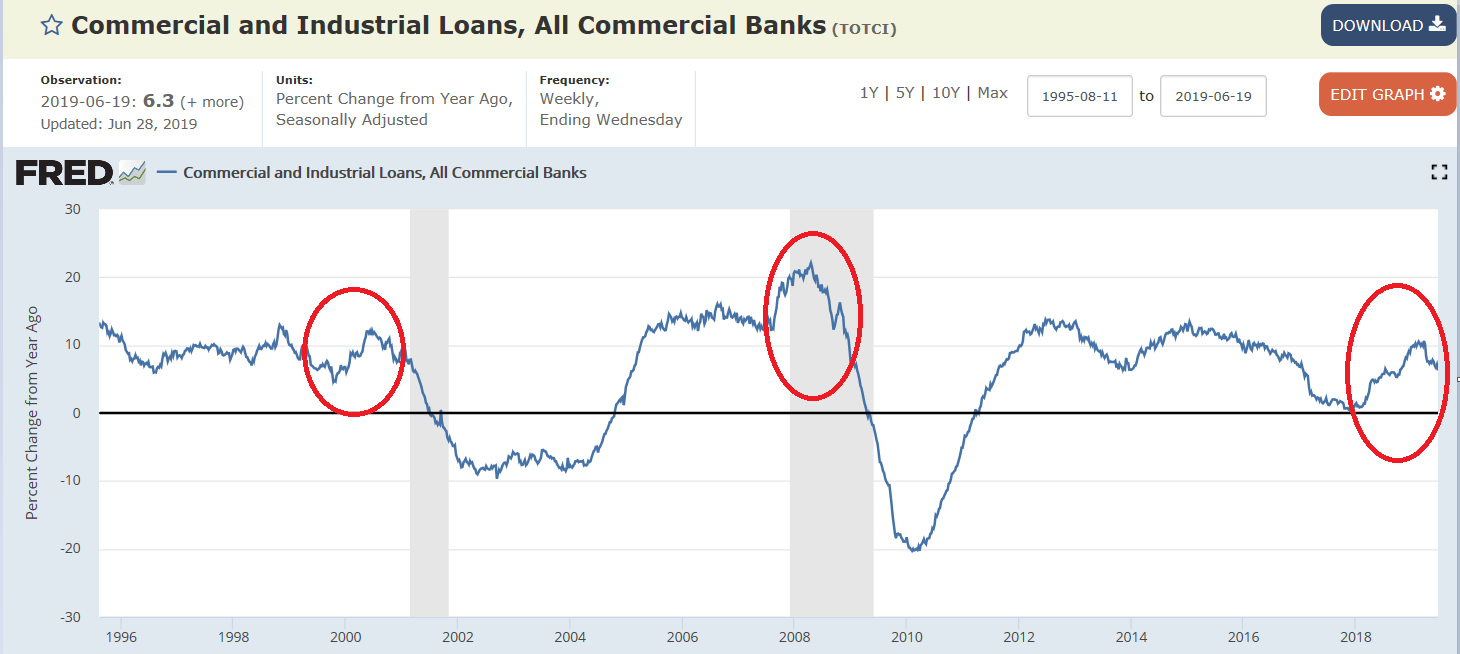

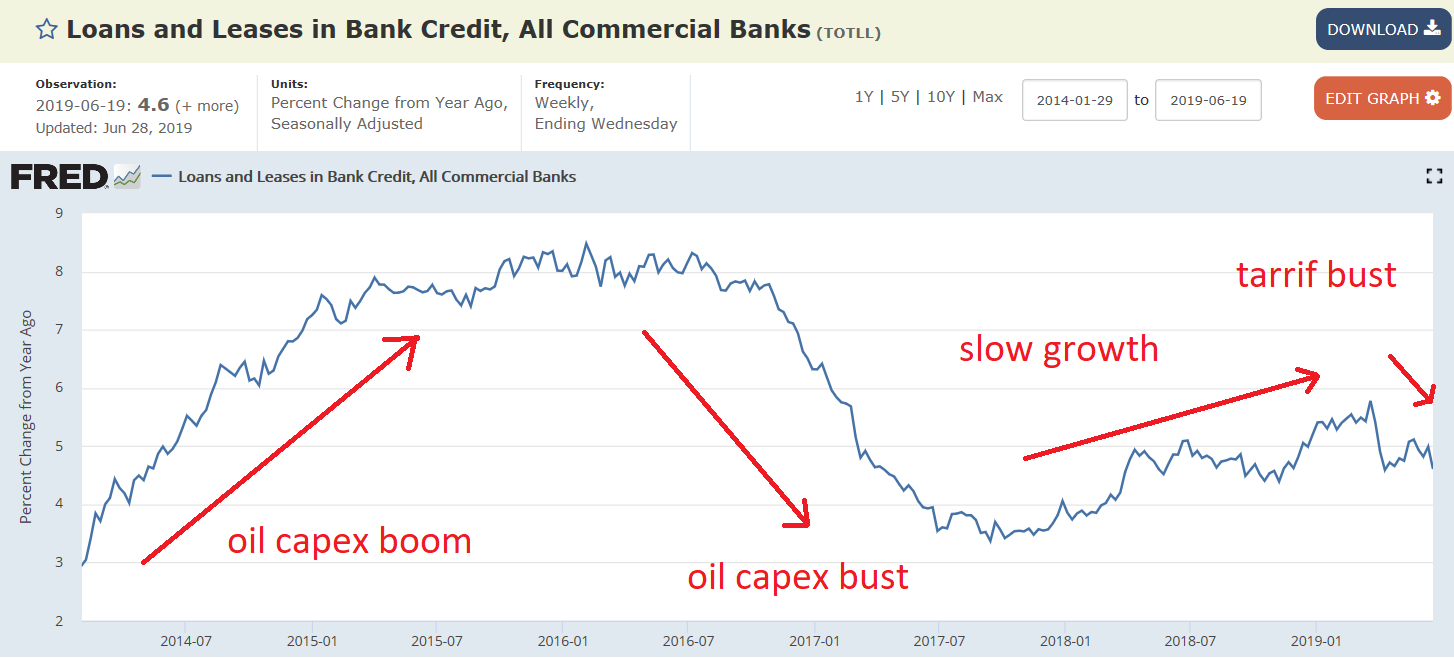

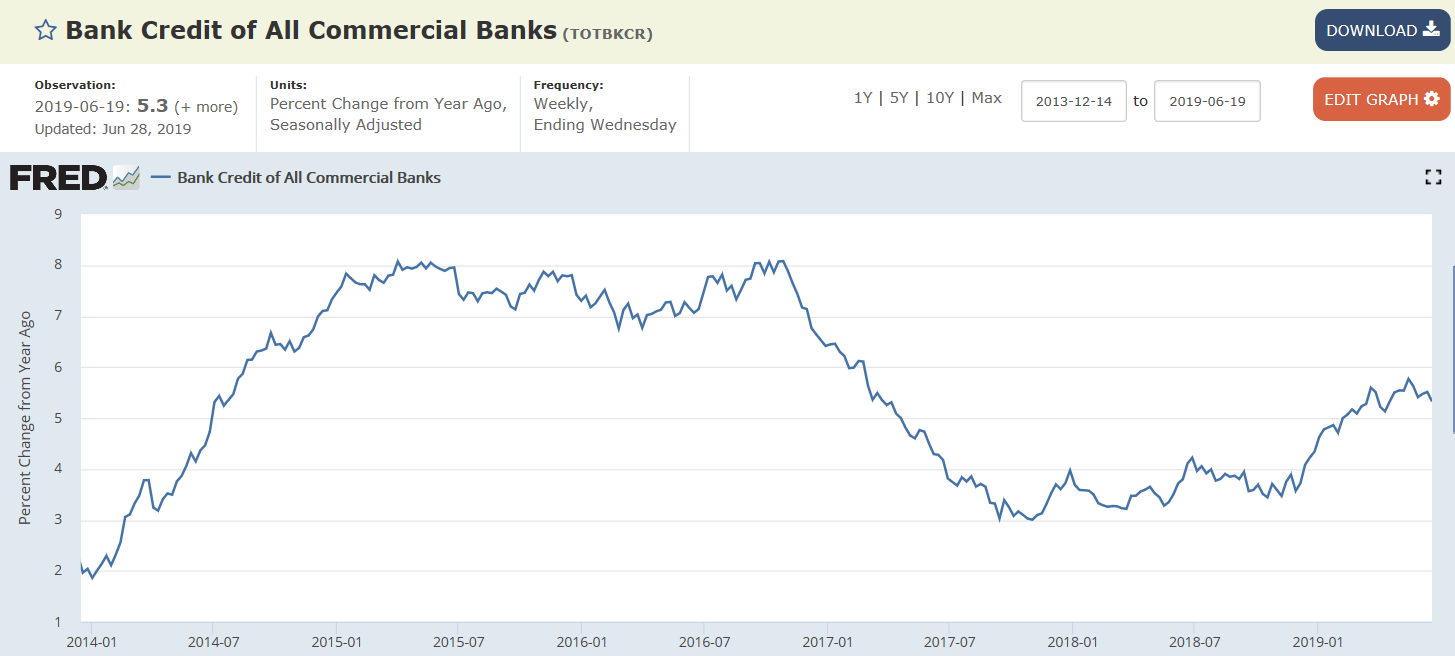

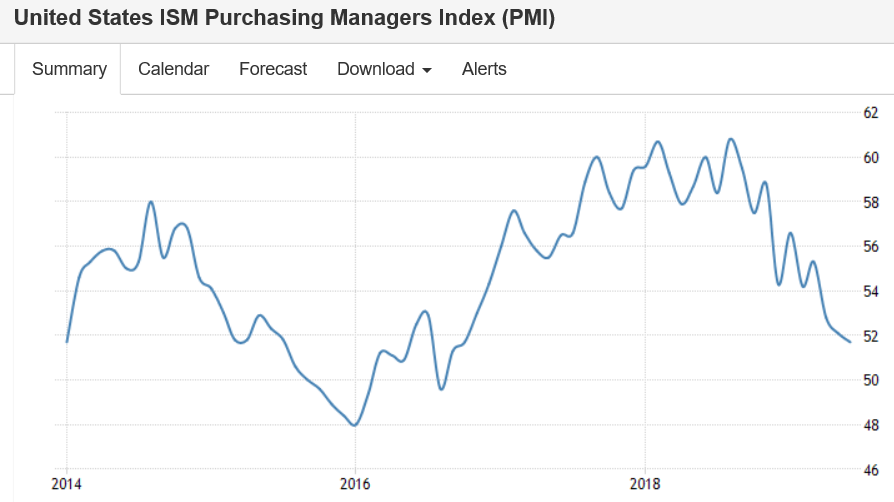

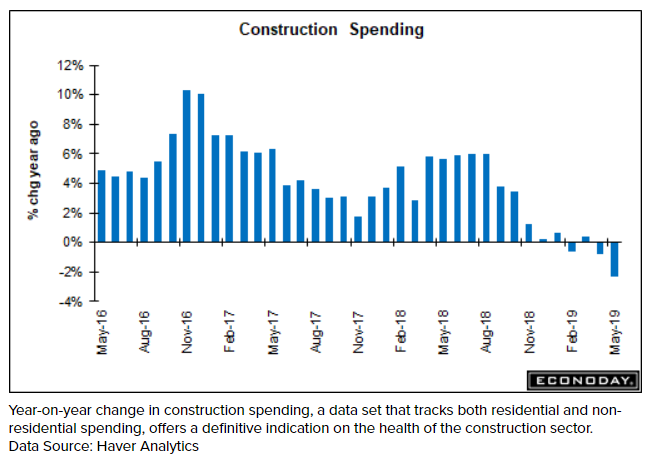

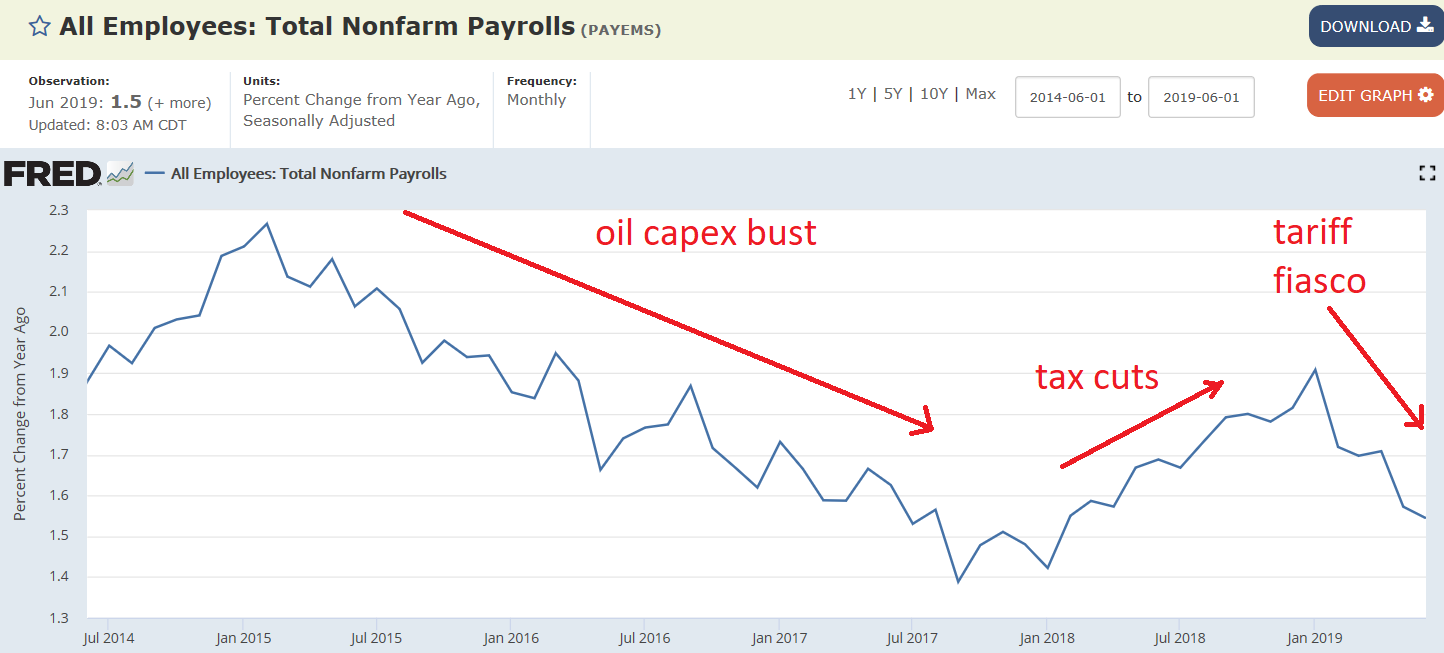

The annual rate of change continues to take a dive:

Highlights

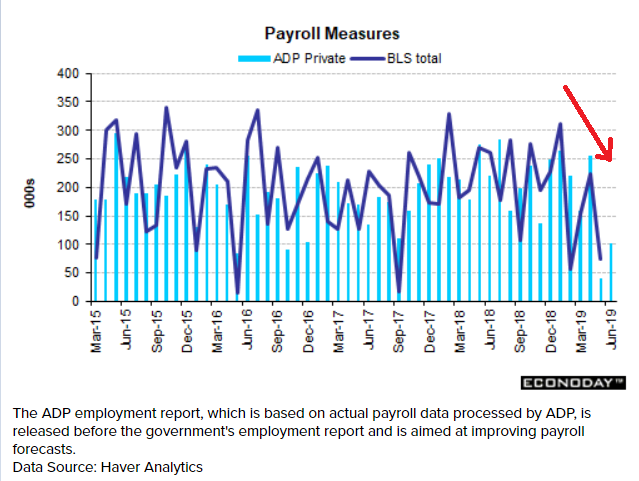

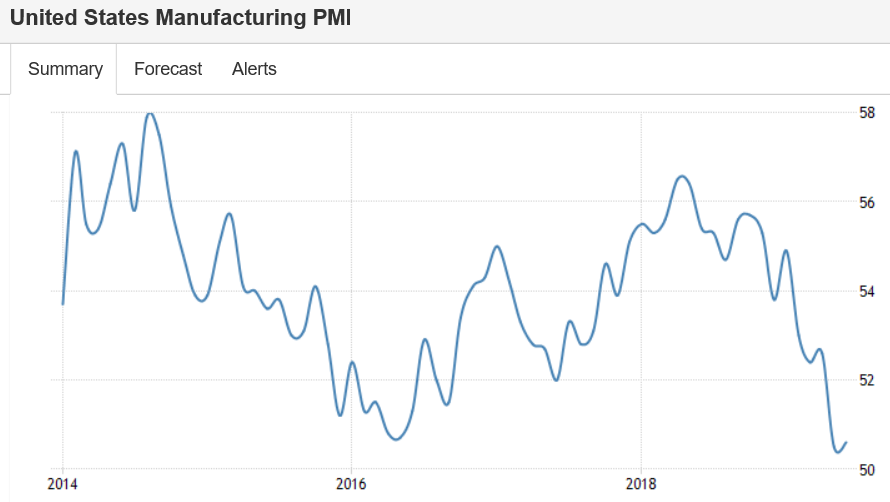

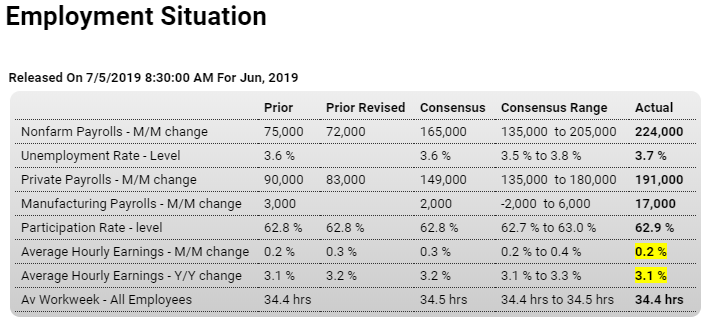

There’s still time to cancel your rate-cut party. Nonfarm payrolls shot 224,000 higher in June and well beyond Econoday’s consensus range where the high forecast was 205,000. There are no flukes in this report underscored by a 17,000 jump for what has been an uneven manufacturing sector that Federal Reserve policy makers are watching with concern. Payrolls at professional & business services jumped 51,000 as employers scramble to meet demand with contractors. Government payrolls, up 33,000, were also a large contributor to June’s growth.

Continuing evidence that dementia is setting in:

“In June of 1775, the Continental Congress created a unified Army out of the Revolutionary Forces encamped around Boston and New York, and named after the great George Washington, commander in chief. The Continental Army suffered a bitter winter of Valley Forge, found glory across the waters of the Delaware and seized victory from Cornwallis of Yorktown.

“Our Army manned the air, it rammed the ramparts, it took over the airports, it did everything it had to do, and at Fort McHenry, under the rocket’s red glare it had nothing but victory. And when dawn came, their star-spangled banner waved defiant.”

‘In 2016, before his election, Trump suggested it might be time to stage a return: “Bringing back the gold standard would be very hard to do—but boy, would it be wonderful. We’d have a standard on which to base our money.” This might be dismissed as a throwaway comment, if not for Trump’s desire to put the likes of Cain, Moore, and now Shelton on the Fed board, giving a goldbug a seat at the table to steer the most powerful country’s monetary policy.’