The reason the Fed is talking hike is because they believe the continued modest growth is reducing the excess capacity in the economy, and they are concerned about hitting the wall of full employment with their 0 rate policy and multi $ trillion portfolio, both of which they believe to be highly accommodative.

That is, they believe the car is creeping along in the fog towards what they believe is a wall with their foot on what they believe is the accelerator, and they want to lighten the pressure on the presumed accelerator before they hit the presumed wall.

However, they also know the growth in employment is only very slightly staying ahead of population growth, and, likewise, most all of the drop in the rate of unemployment is due a drop in the labor force participation rate, and not to employment growth. And they also know most of the newly employed were not considered in the labor force when they were hired, raising questions about what the labor force participation rate is actually measuring. And further evidence of a continued high level of slack are the continuing low levels of wage increases, as well as low reported inflation readings in general, which remain well below Fed targets 6 years into their 0 rate and QE initiatives.

And then there is the counterfactual, with their models telling them the economy would have been a whole lot worse without their accommodative policies. Believing that suggests that any backing off from current policy risks a substantial setback.

My conclusion- no telling what they might do. These are human beings navigating in a fog with an inapplicable map, and they think the brake pedal (lowering rates) is the gas pedal.

San Francisco Fed’s Williams Sees Rate Increase ‘This Year,’ If Risks Dissipate

By Jon Hilsenrath and Michael S. Derby

July 1 (WSJ) — “All of the data that we have had up until now has been, I think, encouraging. It …has been about as good, or better, than I was expecting, in terms of the U.S. economy,” San Fran Fed president John Williams said. “But there are some pretty significant—and I would say have now grown larger—headwinds that have developed.” The change in financial conditions since the July Fed meeting, in the form of falling stock prices and a rising dollar, “have been pretty big,” he said. “It’s not the case that nothing has changed since our last [policy] meeting.”

Sure looks to me like most everything peaked when oil prices collapsed:

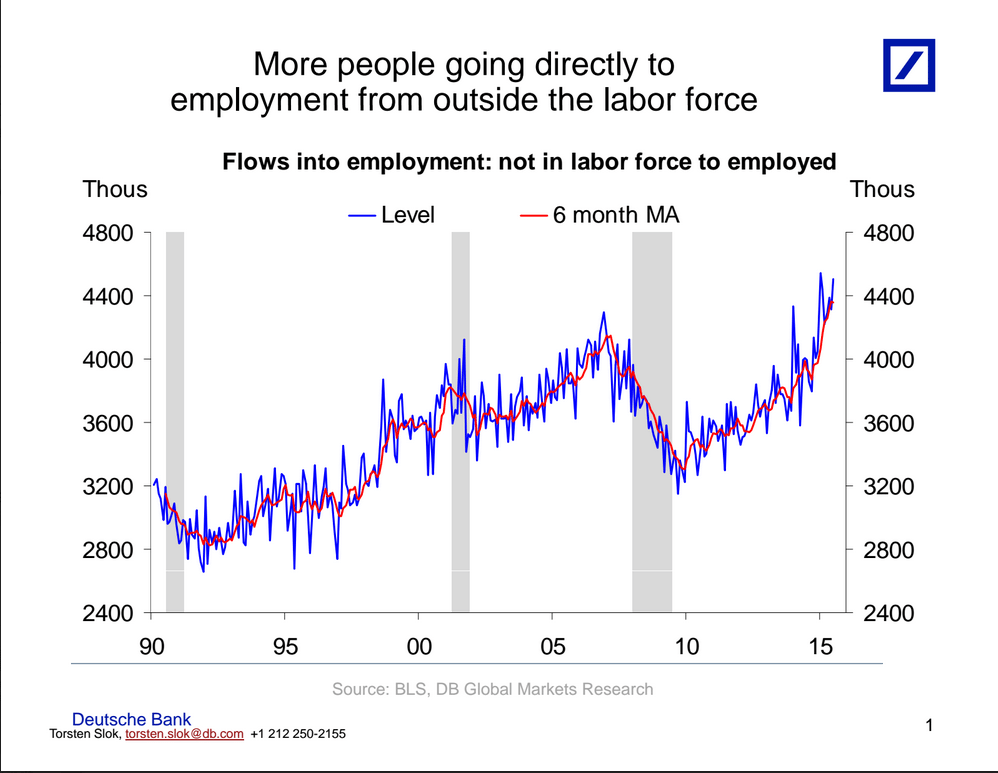

So, interesting how the jobs are coming from ‘outside the labor force’ when it’s been the presumed and unique ‘shrinking labor force’ that’s resulted in most of the decline in the unemployment rates:

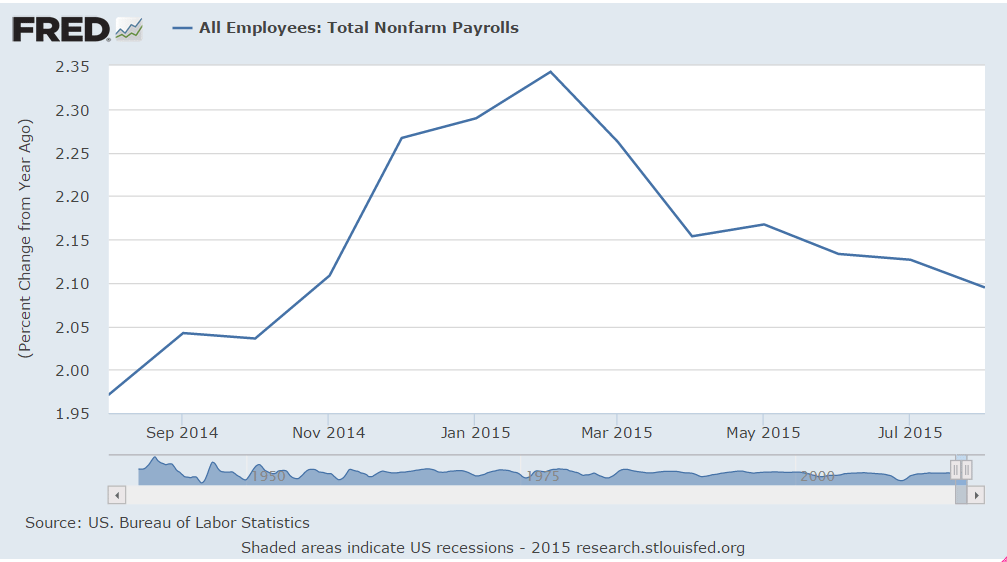

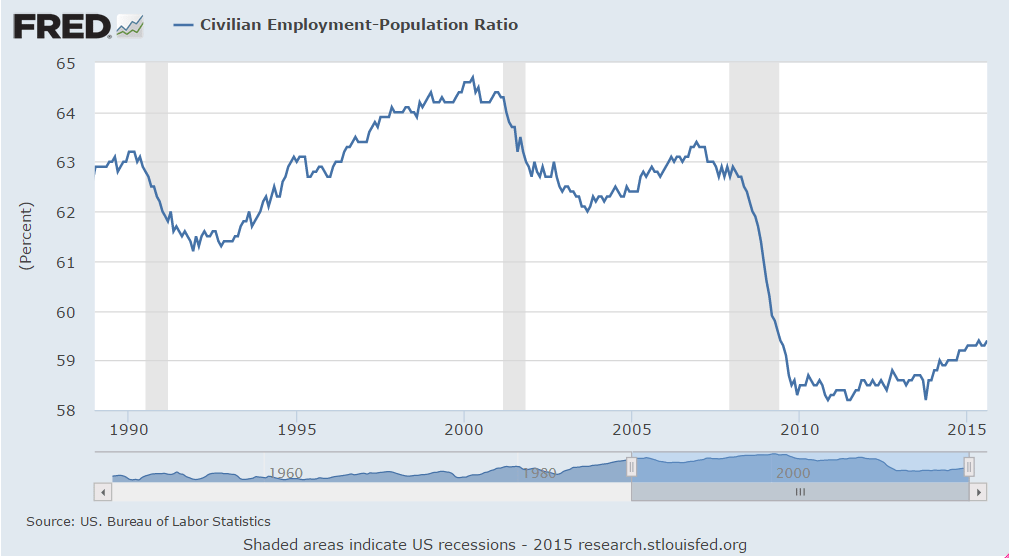

Employment growth has been nearly matched by population growth, so, again, it’s only via the ‘shrinking labor force’ argument that there’s been ‘improvement’:

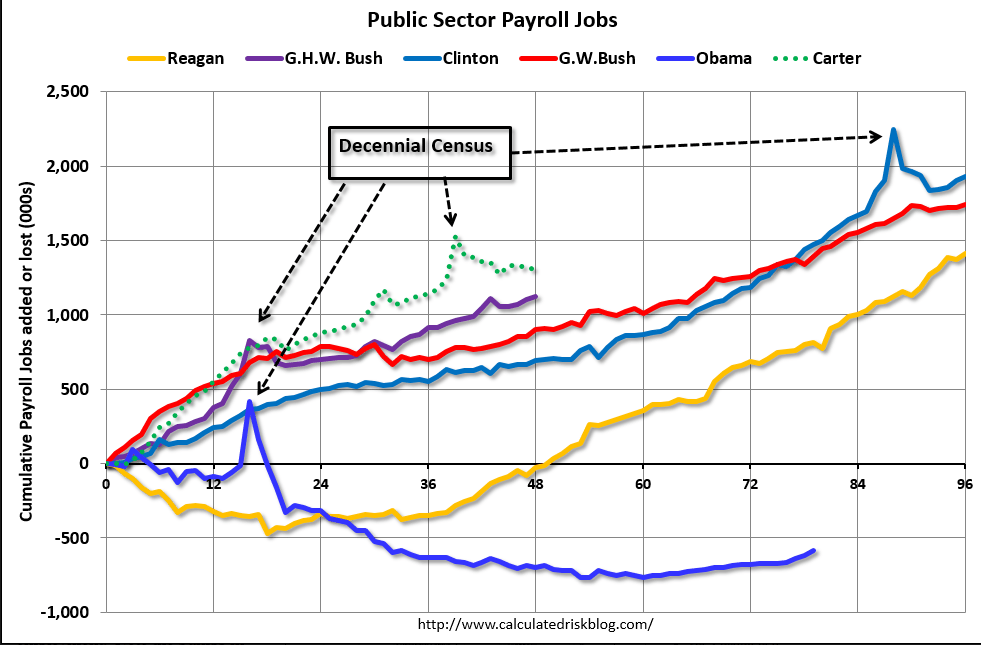

President Obama remains the all time Tea Party hero when it comes to reducing the size of govt:

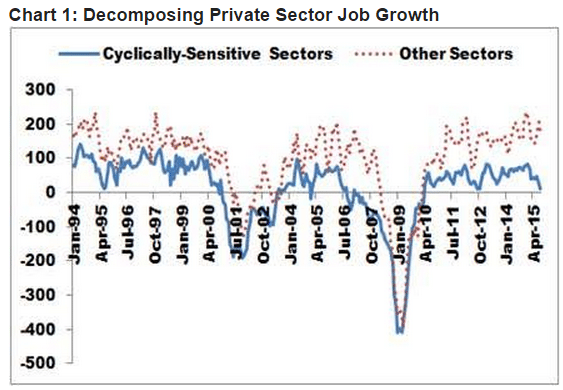

From RHB- you can see which one leads:

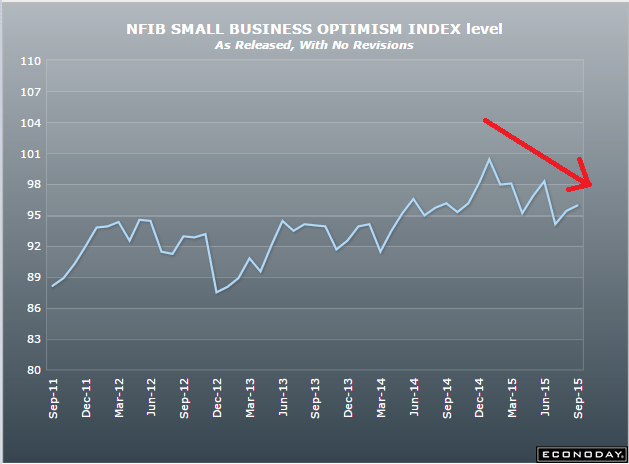

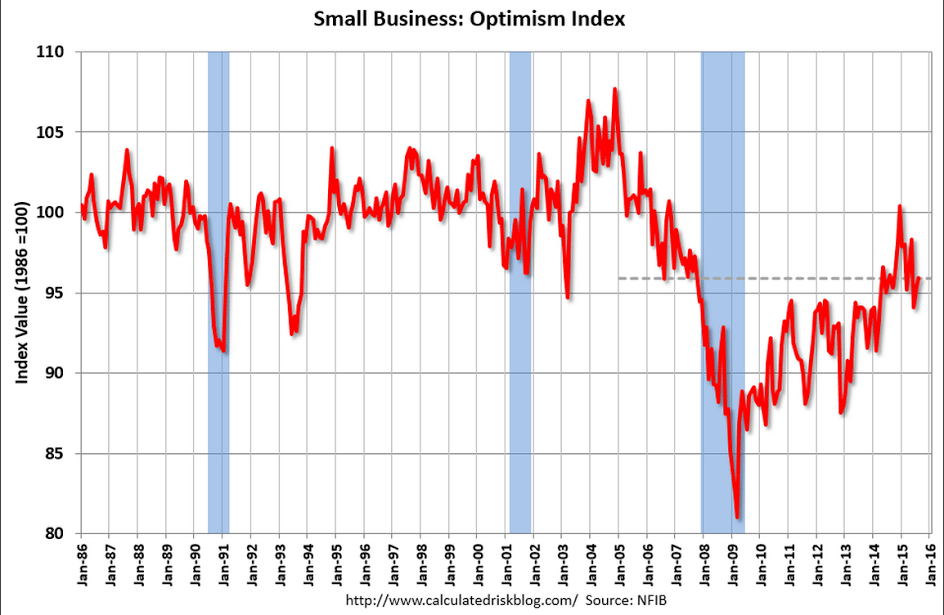

NFIB Small Business Optimism Index

Highlights

A solid gain in job openings and a solid bounce back for earnings trends helped lift the small business optimism 4 tenths to 95.9 vs Econoday expectations for 96.0. The index shows no immediate effect from troubles in China and global volatility. Hiring, capital spending and inventory investment plans firmed slightly, collectively adding 2 points. But the two outlook components collectively declined 4 points in readings that do not point to a big second-half finish for the economy.

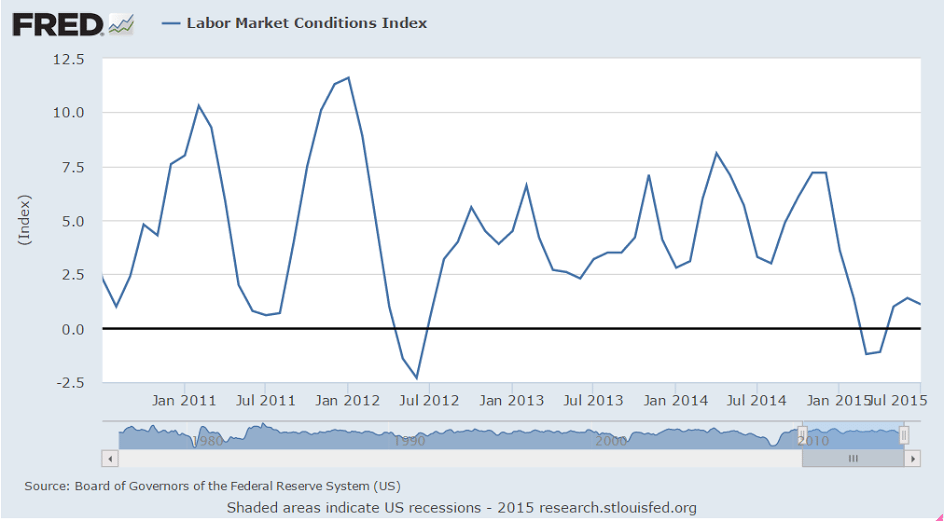

Labor Market Conditions Index

Highlights

The August employment report proved mixed but not the labor market conditions index which rose 3 tenths to 2.1. This is a soft level compared to the mid-single digit trend of 2013 and 2014 but is still the highest reading of the year, since December. Adding to the strength is a 7-tenths upward revision to July. Payroll growth in August was weak but not the unemployment rate which fell 2 tenths to a recovery best of 5.1 percent. This index is based on a broad set of 19 components and could be cited by the hawks as evidence of labor market improvement at next week’s FOMC.

This hasn’t updated yet but you can see today’s print of 2.1 doesn’t impress: