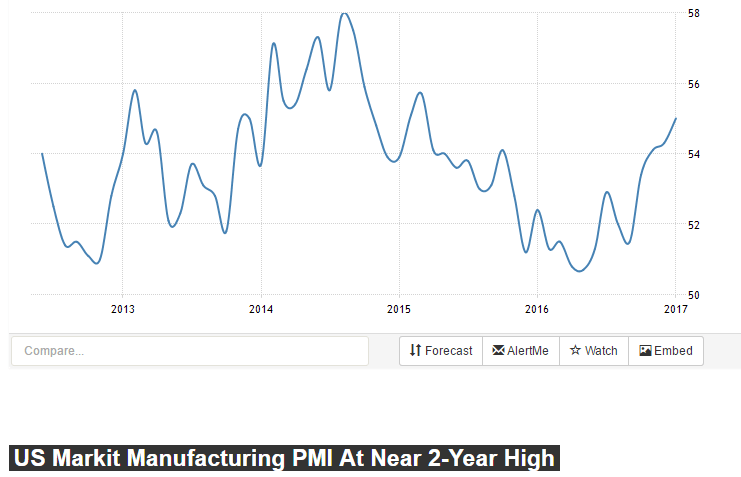

Same story- survey expectations elevated while hard data continues to soften:

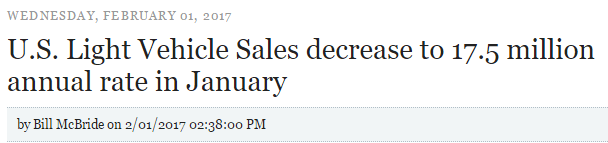

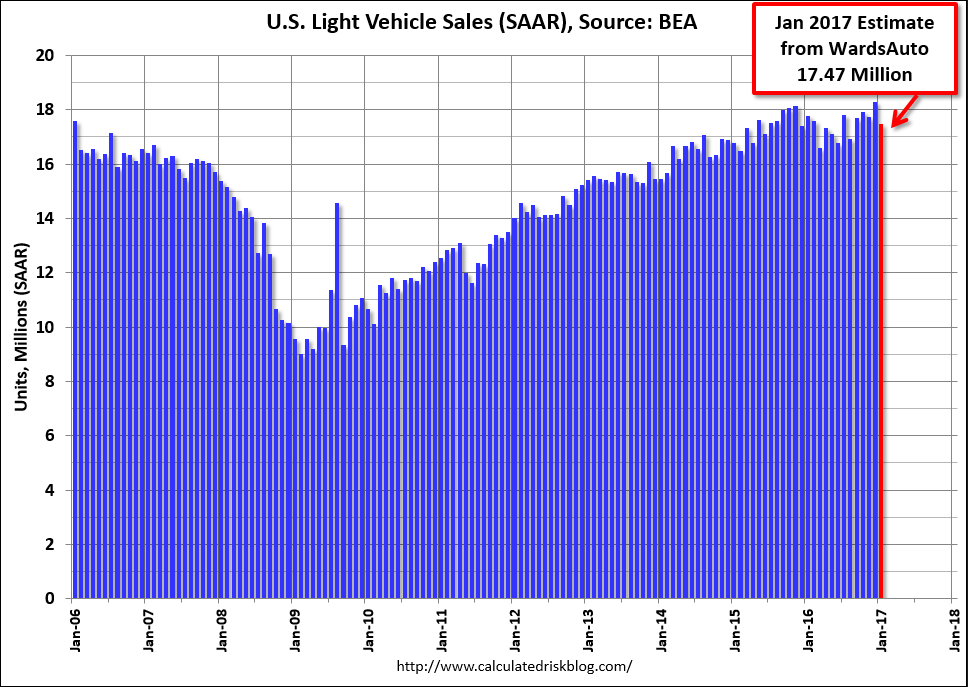

Based on a preliminary estimate from WardsAuto, light vehicle sales were at a 17.47 million SAAR in January.

That is up about 2% from January 2016, and down 4.5% from the 18.29 million annual sales rate last month.

Read more at http://www.calculatedriskblog.com/#qWEO2cMQ2CSiDhiS.99

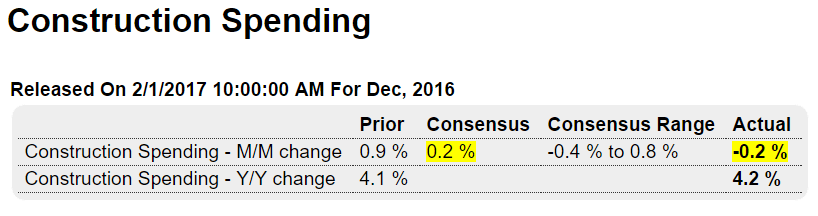

Highlights

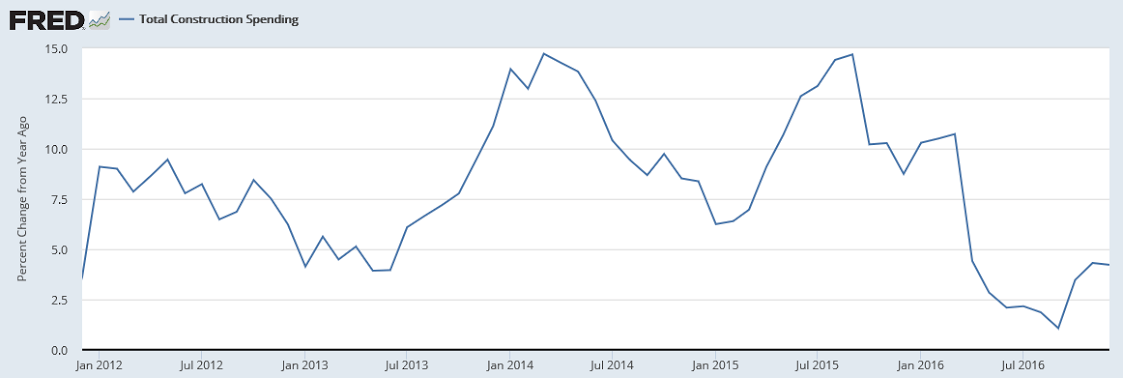

Construction spending fell 0.2 percent in December but details show welcome gains for housing. Spending on new single-family homes rose 0.5 percent in the month with multi-family spending up 2.8 percent. A negative on the residential side, however, is a 0.6 percent dip in home improvements.

More negative pull comes from public construction spending which fell a sharp 1.7 percent in the month. Educational spending fell 2.2 percent with highways & streets down 0.6 percent. Private nonresidential categories are mixed with total spending for this component unchanged in the month.

Spending on new home construction will have to improve further to ease the very tight supply in the new home market. Watch for construction payrolls, one possible highlight of Friday’s employment report.

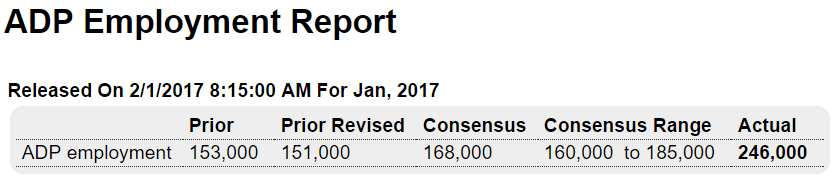

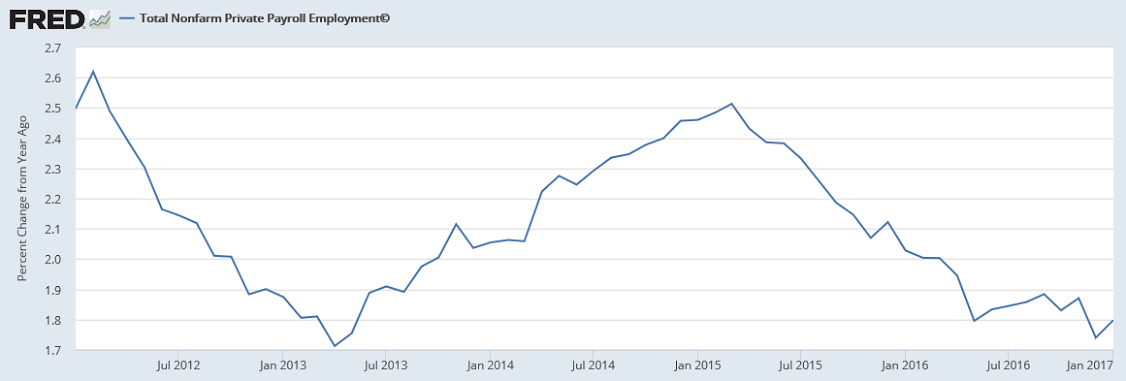

This is a forecast of Friday’s payroll report:

Highlights

ADP is calling for substantial strength in Friday’s employment report, at 246,000 for private payrolls. This is far beyond expectations and would compare with December private payroll growth in the government’s report of 144,000 (ADP’s count for December is revised slightly lower to 151,000). Today’s data follow positive employment indications in yesterday’s consumer confidence report and may very well pull expectations higher, at least to a degree, for January’s employment report.

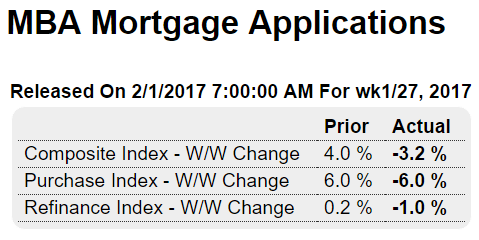

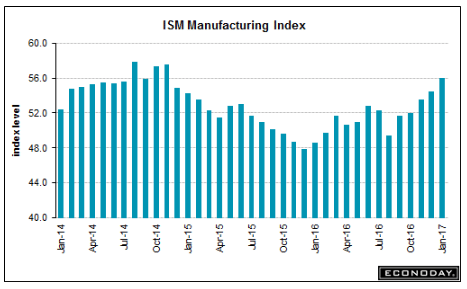

This is a survey:

So is this: