Durable Goods Orders

Highlights

Durables orders fell back in August, coming off July’s surge in aircraft orders. But the core was healthy in August. New factory orders for durables dropped a monthly 18.2 percent, following a spike of 22.5 percent in July. Market expectations were for a 17.1 percent fall. Transportation fell a monthly 42.0 percent in August, following a 73.3 percent jump the month before.

Excluding transportation, durables orders rebounded 0.7 percent, following a decline of 0.5 percent in July. Analysts projected a 0.8 percent gain for August.

Within transportation, nondefense aircraft fell a monthly 74.3 percent, following a 315.6 percent spike in July with both swings essentially reflecting Boeing aircraft orders. Defense aircraft orders slipped 0.6 percent, following a 31.7 percent drop in July. Motor vehicle orders have been moderately volatile but healthy on average, decreasing 6.4 percent after a 10.0 percent boost the prior month.

Outside of transportation, major industries seeing a gain in the latest month were fabricated metals, machinery, computers & electronics, electrical equipment, and “other.” Declines were posted for primary metals.

Orders for equipment investment made a healthy comeback in August. Nondefense capital goods orders excluding aircraft rebounded 0.6 percent in August, following a dip of 0.2 percent the month before. Shipments of this series edged up 0.1 percent but followed a strong 1.9 percent gain in July.

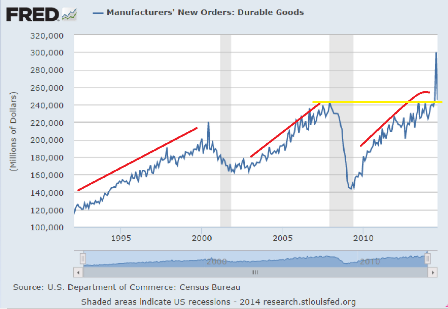

Recent durables orders have shown record volatility. On average, durables orders point to moderate upward momentum in manufacturing.

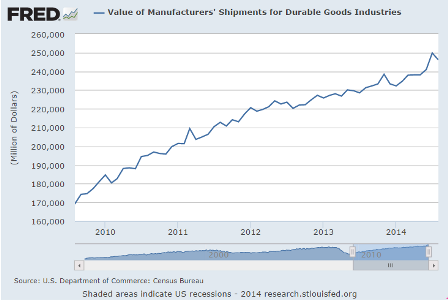

The yellow line is to show that actual orders have just gotten back to pre recession levels, and that’s not inflation adjusted, so in real terms they haven’t yet caught up.

The red lines are roughly the ‘slope’ which is a proxy for the rate of growth, but it should get ever steeper on this arithmetic chart to indicate the same rate of growth. So the growth rate in this cycle is slowing. And also seems last time around we went into recession before this indicator turned south, while the cycle before that it turned down before we went into recession.

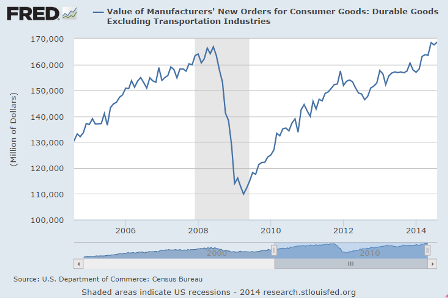

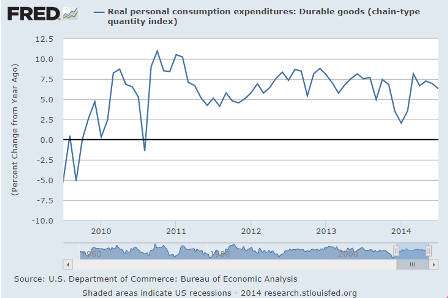

Adjusted for inflation this is still below 2008 levels as well:

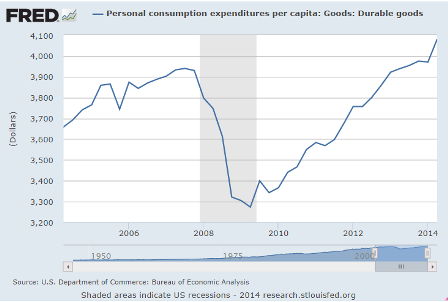

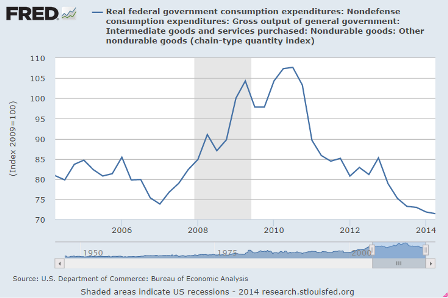

Govt cutbacks in evidence here:

Shipments are what counts for GDP. Last month’s gain increased GDP estimates, this month’s reduction reduces them:

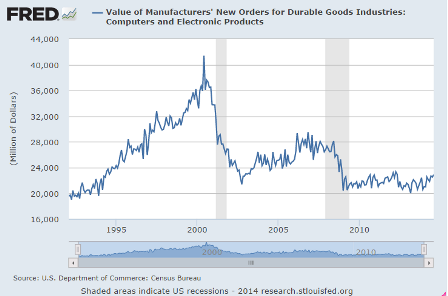

And how about that Y2K/.com mania of the late 90’s!