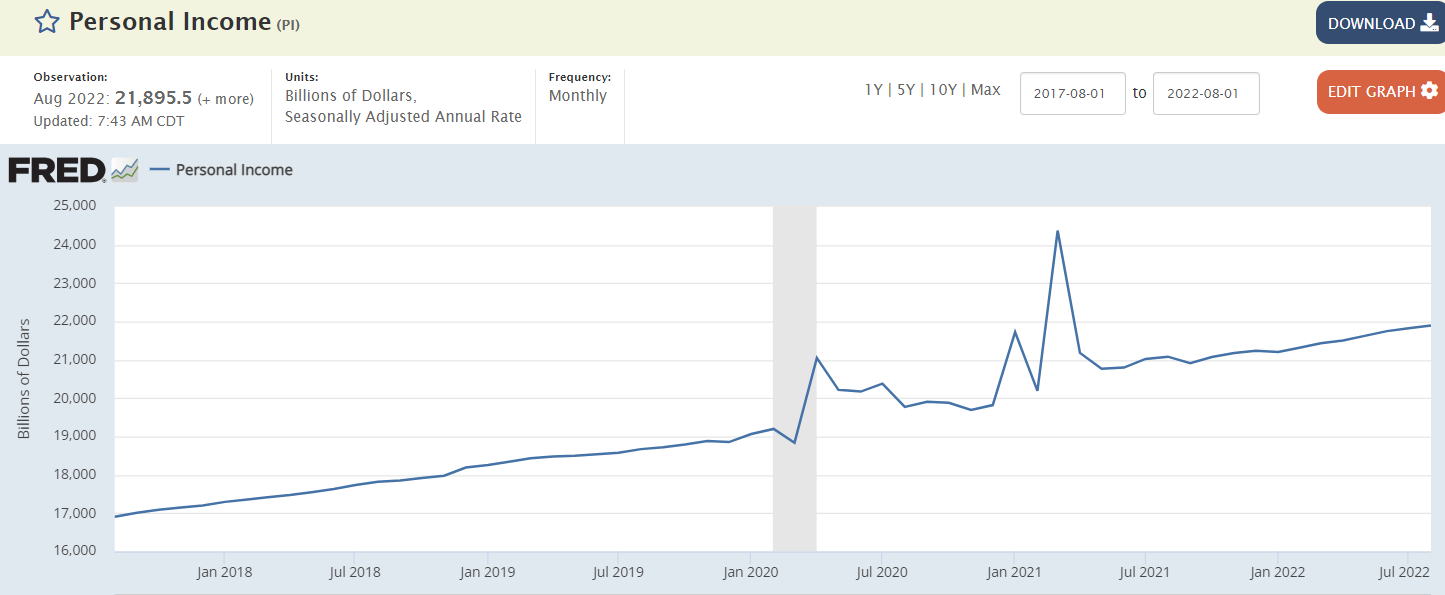

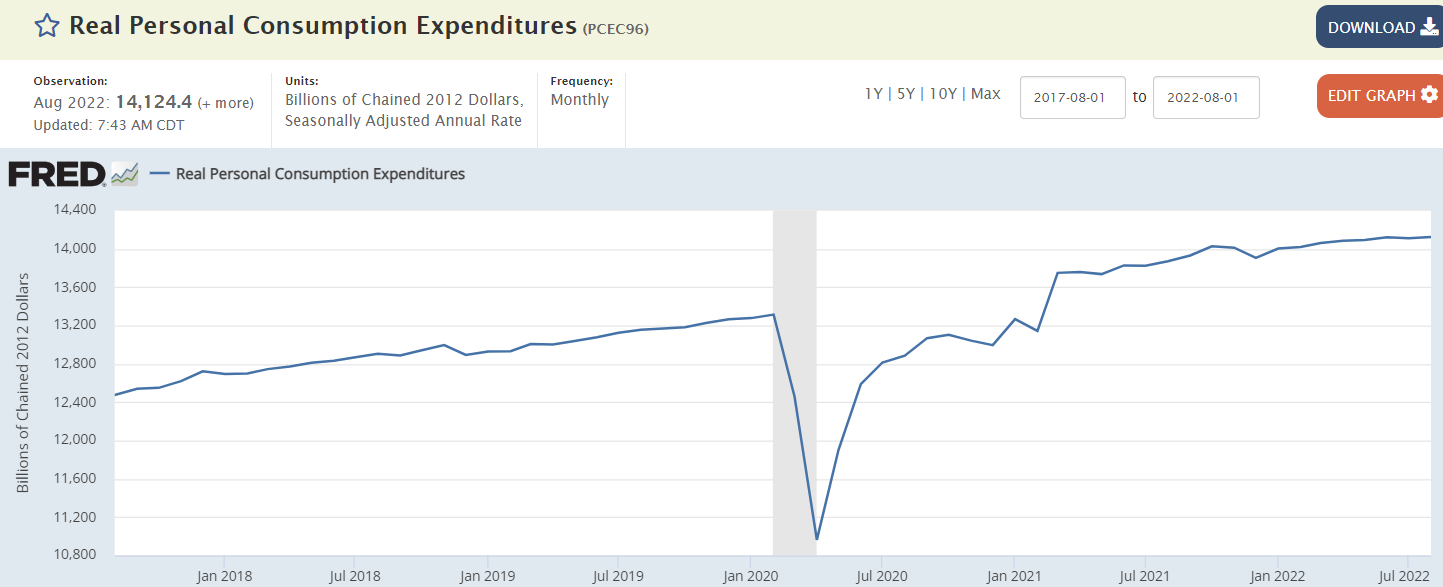

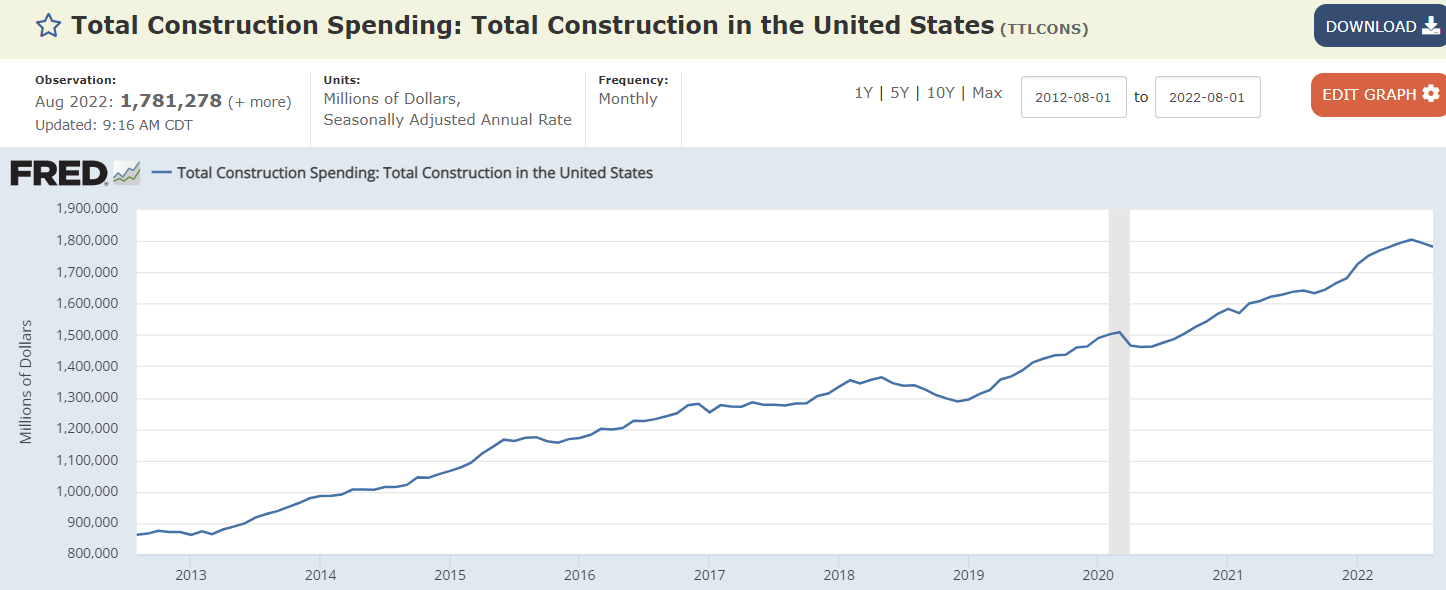

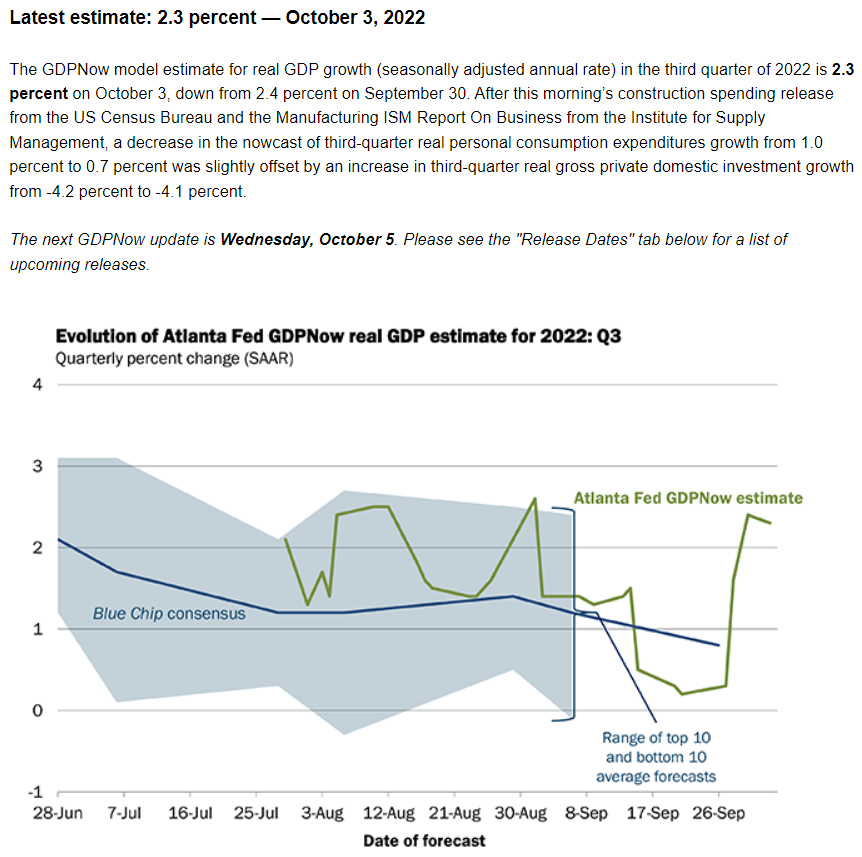

So far so good for Q3 that ended Sep 30- about in line with pre-Covid growth rates:

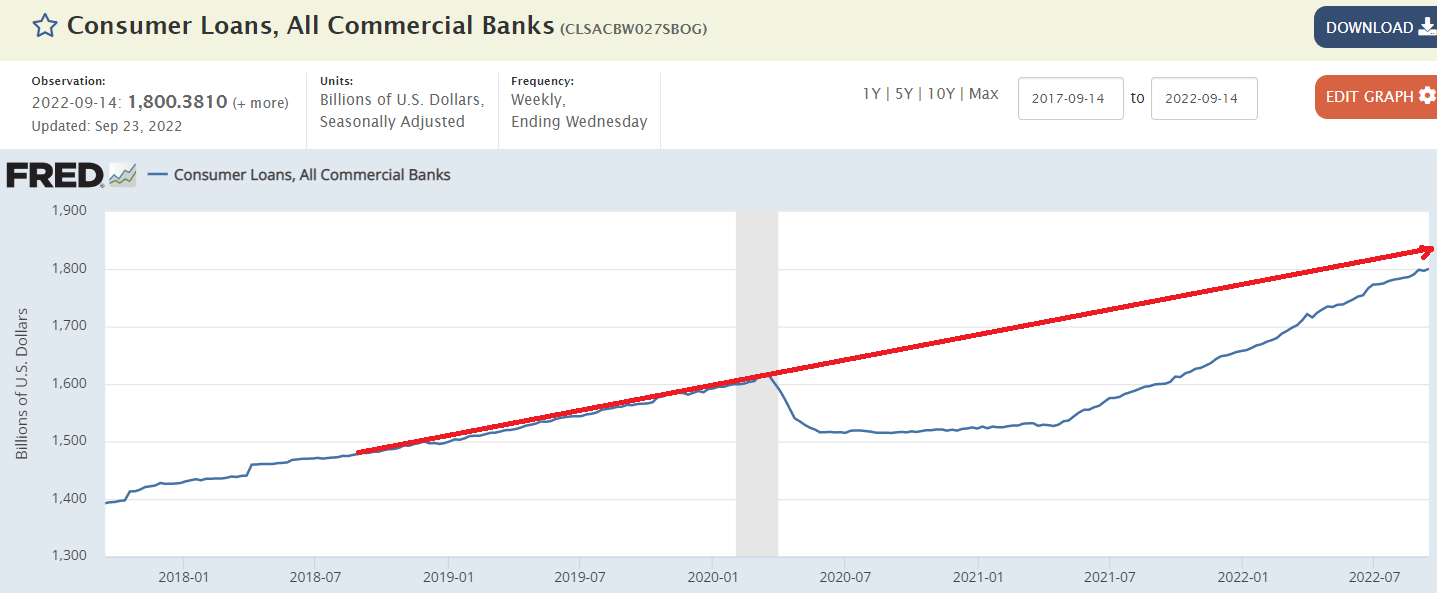

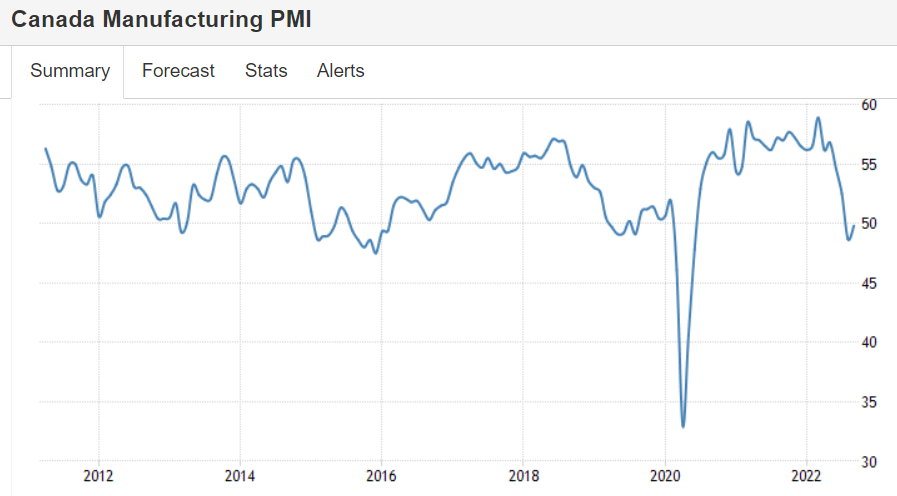

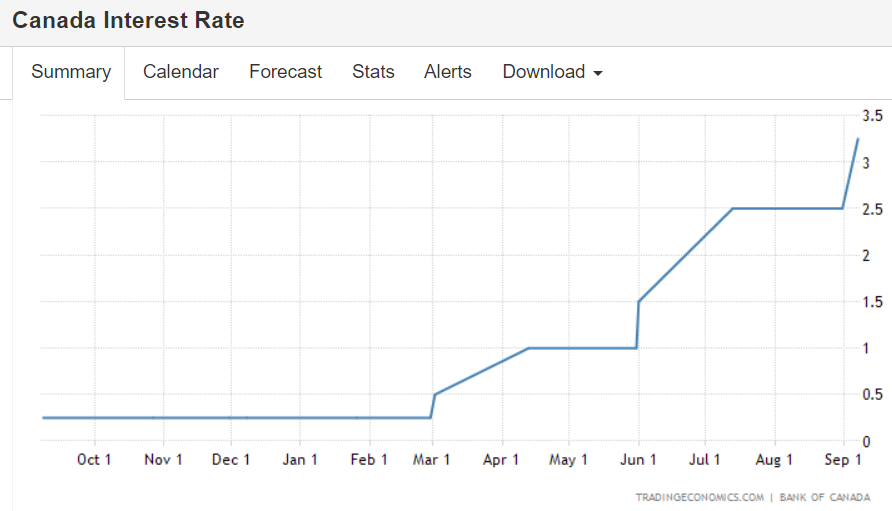

Much like the US, much of the rest of the world is hiking rates with high debt/GDP and supporting their economies that had slowed from fiscal contraction with massive government interest payments- universal basic income for those who already have money:

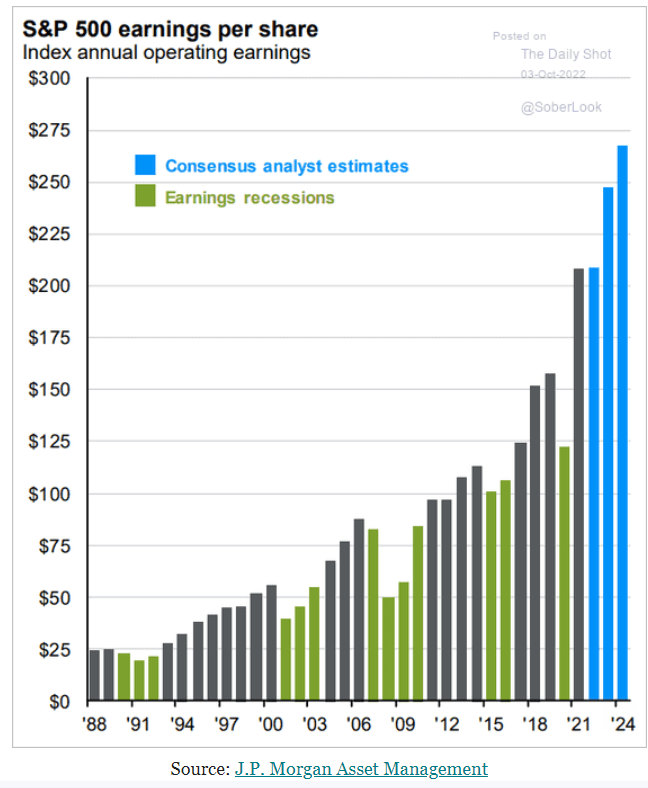

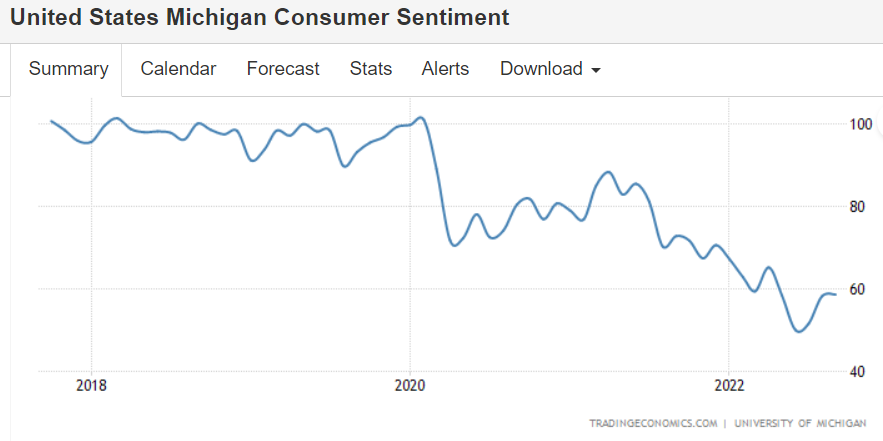

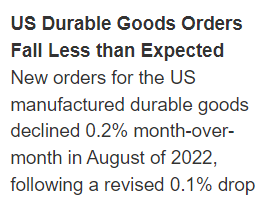

Looks like the pro forecasters see accelerating earrings ahead- yet more evidence the rate hikes aren’t working in the intended direction: