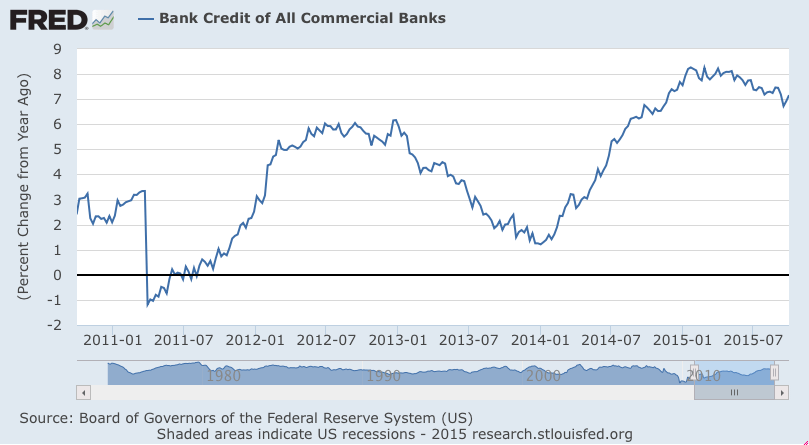

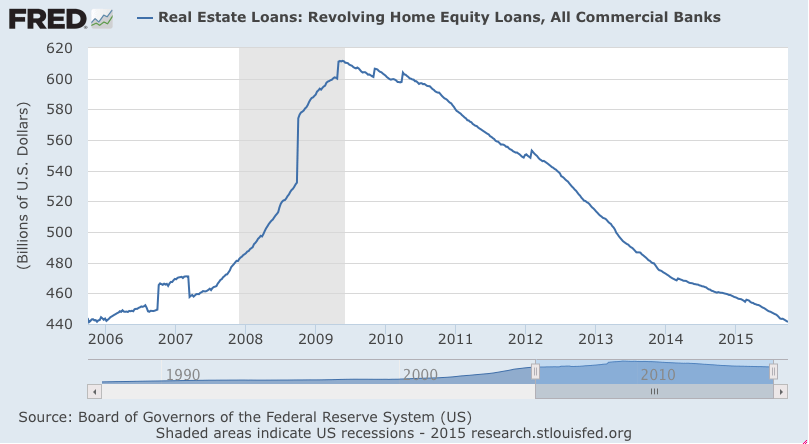

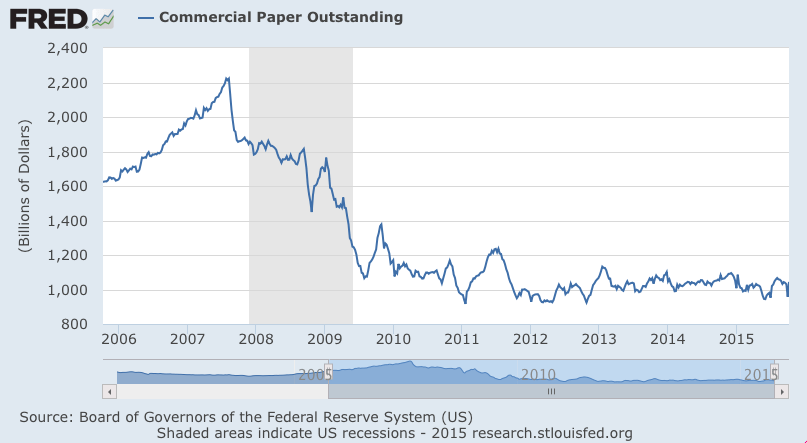

Growth rates still trending lower:

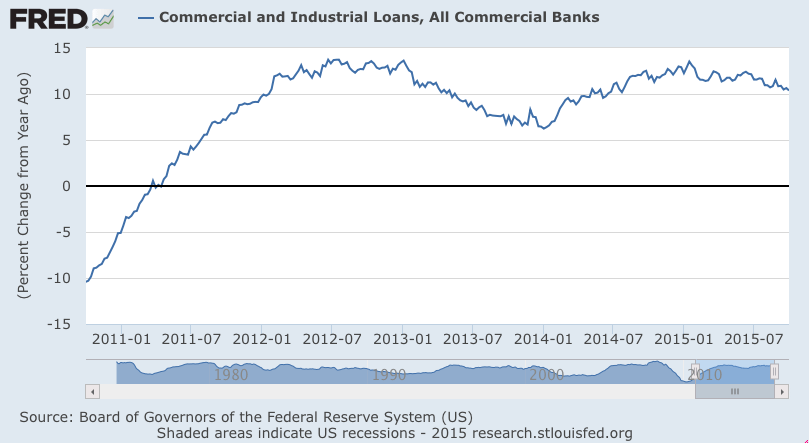

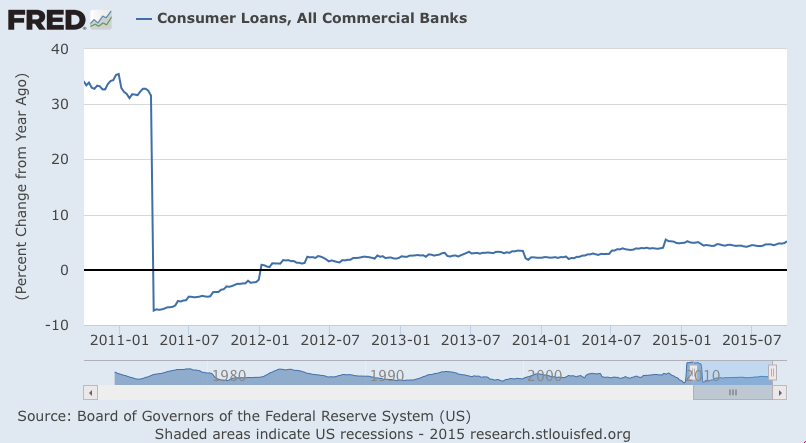

Growth rate edging higher from very low levels:

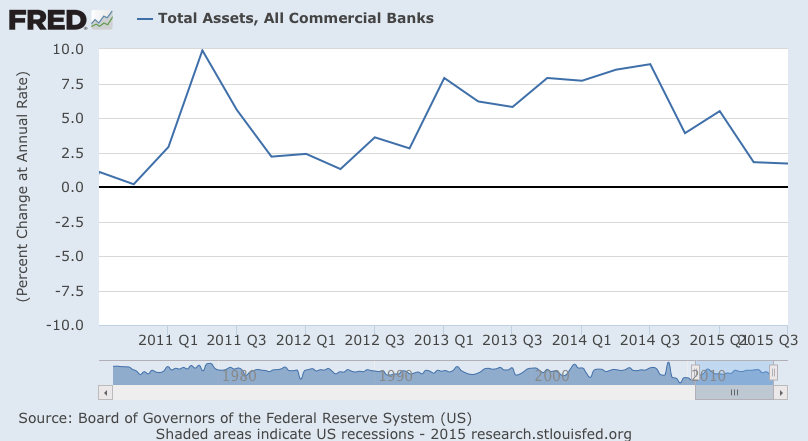

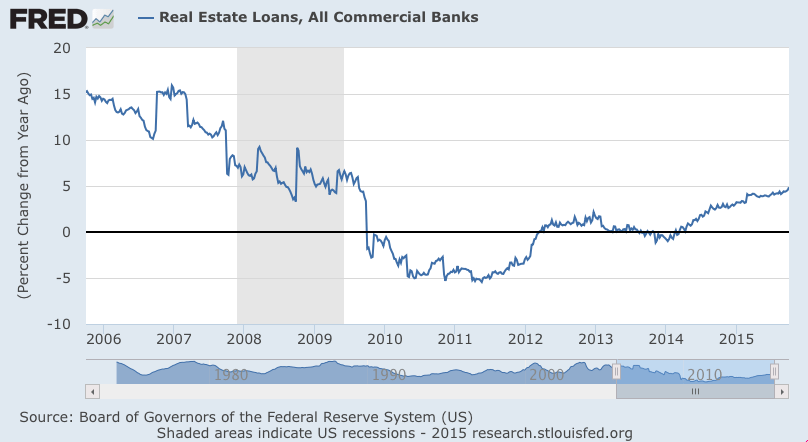

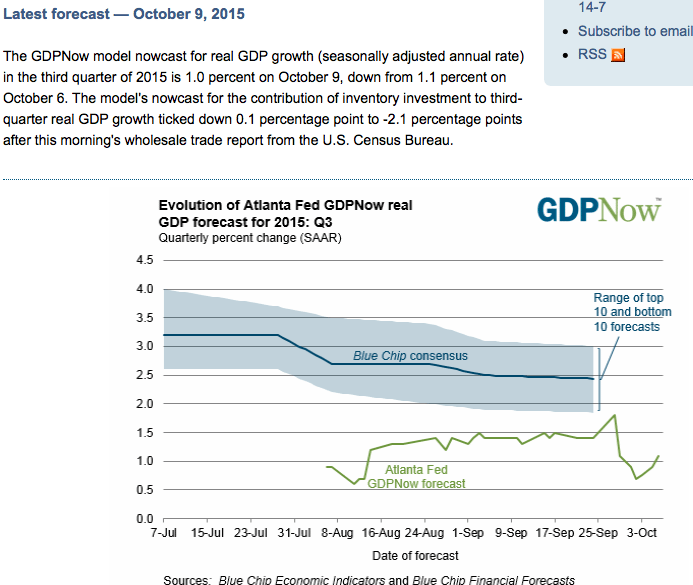

Back down to 1% for Q3:

On October 5th Saudi price cuts were announced, as they increased discounts to various benchmark prices by substantial amounts. If the reports were accurate, the discount increases create a downward price spiral dynamic as previously described.

However, since that announcement oil prices have increased approximately 10% driven by buyers reacting to various news reports ranging from reduced US output to issues surrounding the mid east conflicts. And at the same time the rising oil prices led to a lower $US, higher prices for global equities, and term structures of interest rates moving higher in yield.

The risk here is that if the Saudi discounts are in fact in place, oil prices will reverse and head lower until the Saudis alter their pricing structure. And with traders and managers having previously gone ‘the wrong way’ the sell off in oil and equities will be all the more dramatic.