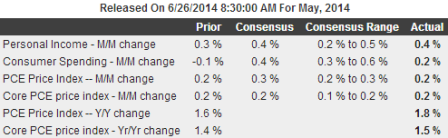

The Commerce Department said consumer spending increased 0.2 percent after being flat in April. Spending, which accounts for more than two-thirds of U.S. economic activity, had been forecast rising 0.4 percent after a previously reported 0.1 percent dip in April.

When adjusted for inflation, consumer spending fell for a second straight month, suggesting spending this quarter could struggle to regain momentum after growing at its slowest pace in nearly five years in the first quarter.

Spending in May was probably constrained by weak healthcare spending as outlays on services barely rose for a second month.

While reports ranging from employment to manufacturing and the services industries suggest the economy has rebounded after sinking in the January-March period, the consumer spending data indicated that growth would probably fall short of the 4.0 percent annual pace that some economists are expecting in the second quarter.

Personal Income and Outlays

From Calculated Risk

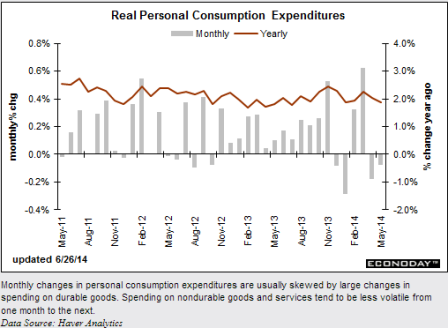

Real PCE — PCE adjusted to remove price changes — decreased 0.1 percent in May, compared with a decrease of 0.2 percent in April. … The price index for PCE increased 0.2 percent in May, the same increase as in April. The PCE price index, excluding food and energy, increased 0.2 percent in May, the same increase as in April. … The May price index for PCE increased 1.8 percent from May a year ago. The May PCE price index, excluding food and energy, increased 1.5 percent from May a year ago.

Note: Usually the two-month and mid-month methods can be used to estimate PCE growth for the quarter (using the first two months and mid-month of the quarter). However this isn’t very effective if there was an “event”, and in Q1 PCE was especially weak in January and February – and then surged in March.

Still, using the two-month method to estimate Q2 PCE growth, PCE was increasing at a 2.3% annual rate in Q2 2014 (using the mid-month method, PCE was increasing less than 1.5%). Since the comparison to March will be difficult, it appears PCE growth will be below 2% in Q2 (another weak quarter).

Note the now familiar down into winter, up some, and then settling down again pattern: