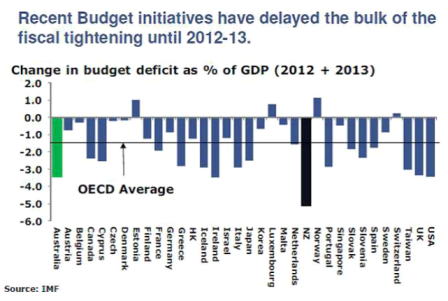

Below is a wonderful chart of fiscal initiatives and their expected impact on GDP. The chart highlights –

a) the two largest fiscal consolidations are expected to occur in NZ and Australia.

the planned consolidation in Australia is the biggest 1y fiscal consolidation on

record for Australia – this is expected to be formally introduced in their May

budget

b) number of initiatives are by the Eurozone countries (both core and peripheral) as they impose fiscal austerity to reduce debt burdens

c) significant negative impact on US GDP should tax cuts etc. that are currently in place are not extended at the end of the year.

Click here for larger version

Daily Archives: April 5, 2012 @ 8:55 am (Thursday)

Euro zone update

The joke used to be: ‘what’s the difference between bonds and bond traders?

Bonds eventually mature.

Except in the euro zone, post the Greek PSI ‘bond tax’, markets are starting to trade like maybe the don’t.

Yes, the ECB can come in and buy again, and probably will with more deterioration, but now it’s known that merely increases the risk of holding the remaining outstanding bonds, as the ECB’s bonds become ‘senior’and don’t get taxed.

So with deficits looking higher due to economic weakness due to mandatory austerity, the sustainability maths pointing to the bond tax route, and the ECB buying further adding to risk of loss, something has to give.

And it all remains potentially catastrophic for the global financial infrastructure, with aggregate demand remaining on the weak side globally and fiscal consolidation pending in most places.