Remain towards the lows, means layoffs still tame:

This looks reasonable as well, but the Markit surveys are always suspect,

and expectations fell:

United States : PMI Services Flash

Highlights

The manufacturing sector may be sputtering but not the service sector, based on Markit’s flash PMI which is up strongly for a second straight month, to a 6-month high of 58.6 in final March vs 57.1 in final February (57.0 February flash). The final reading for January was 54.2.

Respondents are citing improvement in economic conditions, strengthening consumer confidence, and new product launches as pluses. New orders are at a 6-month high and backlogs are at a 5-month high. Employment is also up.

A negative however, and one seen in other data, is a downgrade in expectations. Those seeing a rise in business over the next 12 months is the lowest since June 2012.

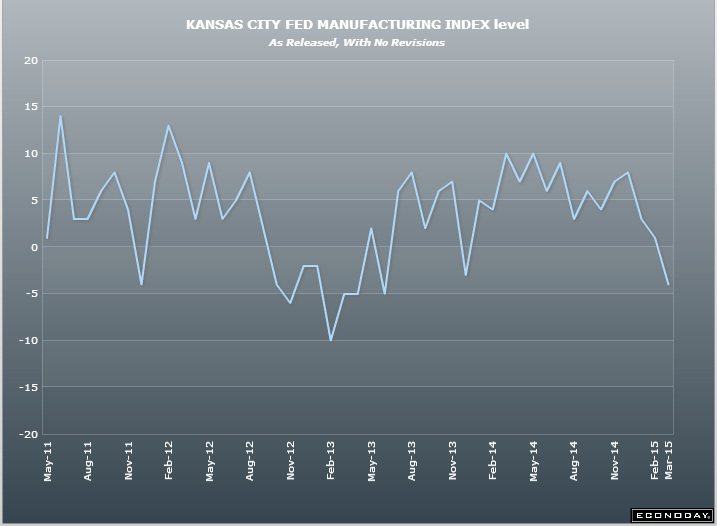

Yet another depressed Fed survey:

United States : Kansas City Fed Manufacturing Index

Highlights

Tenth District manufacturing activity declined in March, and producers’ expectations moderated somewhat but remained slightly positive. Most price indexes continued to decrease, with several reaching their lowest level since 2009. In a special question about the West Coast port disruptions, 32 percent of firms said it had affected them negatively.

The month-over-month composite index was minus 4 in March, down from plus 1 in February and 3 in January . The composite index is an average of the production, new orders, employment, supplier delivery time, and raw materials inventory indexes. The overall slower growth was mostly attributable to declines in plastics, food, and chemical production and continued weakness in metals and machinery. Looking across District states, the largest decline was in Oklahoma, with moderate slowdowns in Kansas and Nebraska.

Other month-over-month indexes decreased from the previous month. The production and shipments indexes fell after rising last month, and the new orders and order backlog indexes dropped to their lowest levels in over two years. In contrast, the employment and new orders for exports indexes inched higher but remained negative. The finished goods inventory index eased from 3 to minus 2, and the raw materials inventory index also moved into negative territory.

Year-over-year factory indexes also decreased. The composite year-over-year index declined from 9 to minus 2, and the production, shipments, new orders, and employment indexes also moved into negative territory. The capital expenditures index eased from 9 to 3, and the order backlog index decreased further. Both inventory indexes moderated somewhat.

Most future factory indexes eased slightly but remained positive. The future composite index moved down from 11 to 4, and the future production, shipments, and new orders index also decreased moderately.