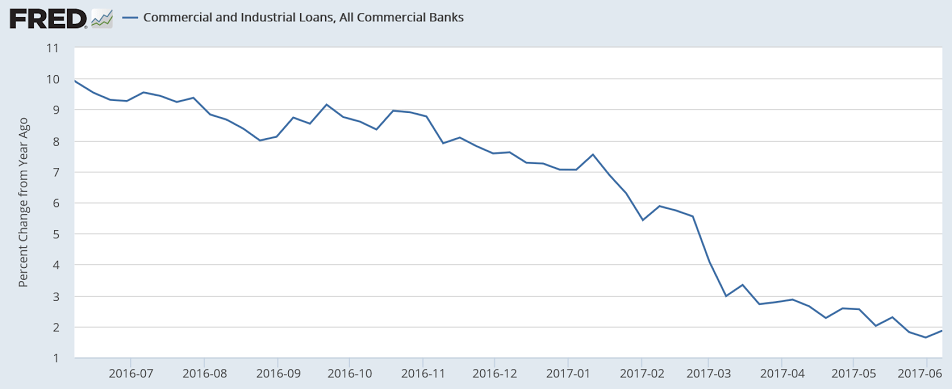

More problematic by the week. Note the absolute level of c and I loans has been flat to negative since October:

Annual rate of growth remains sub 2%:

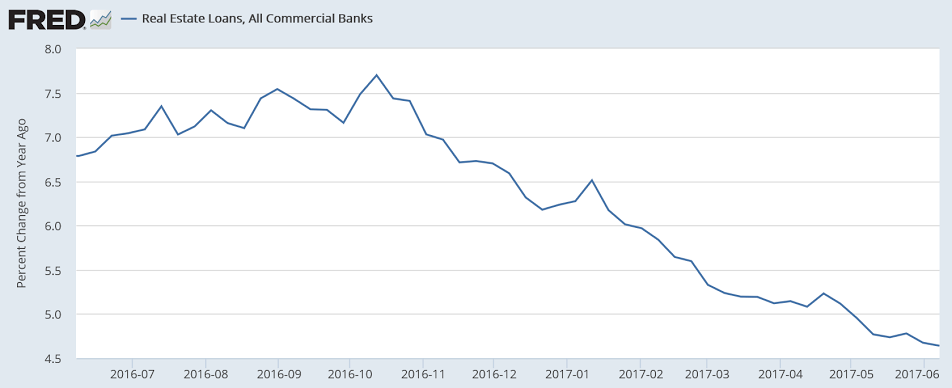

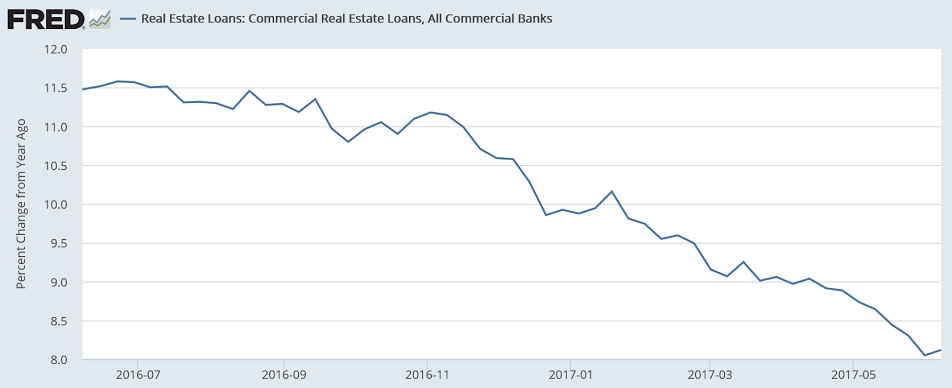

This is consistent with the weakening housing releases:

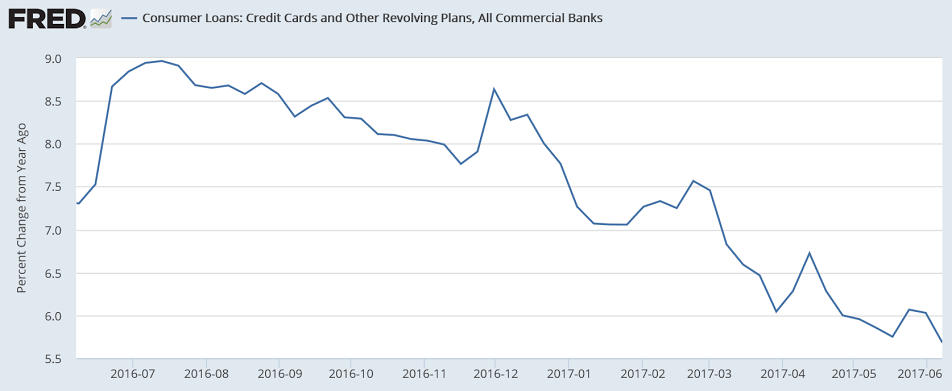

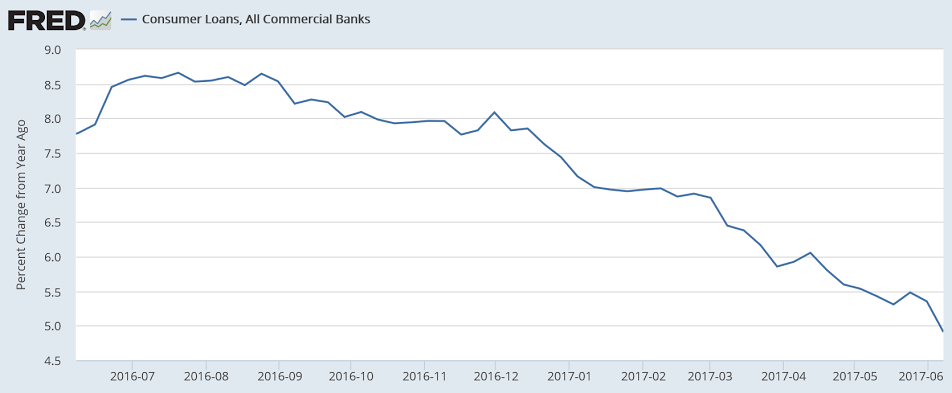

This is consistent with weakening consumer spending:

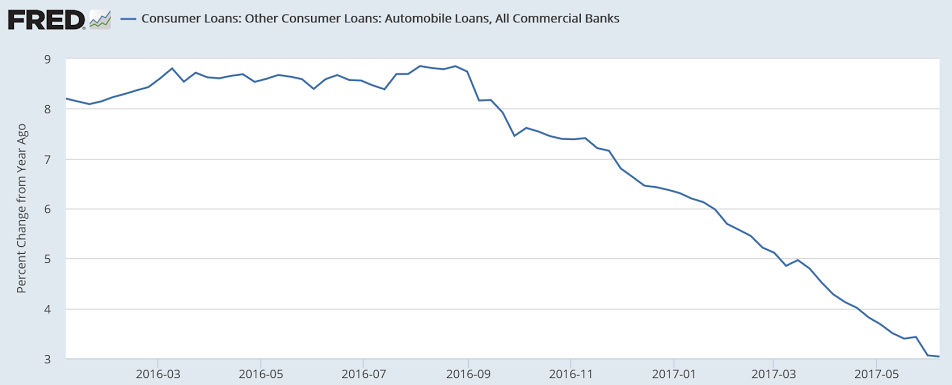

This is consistent with weakening vehicle sales:

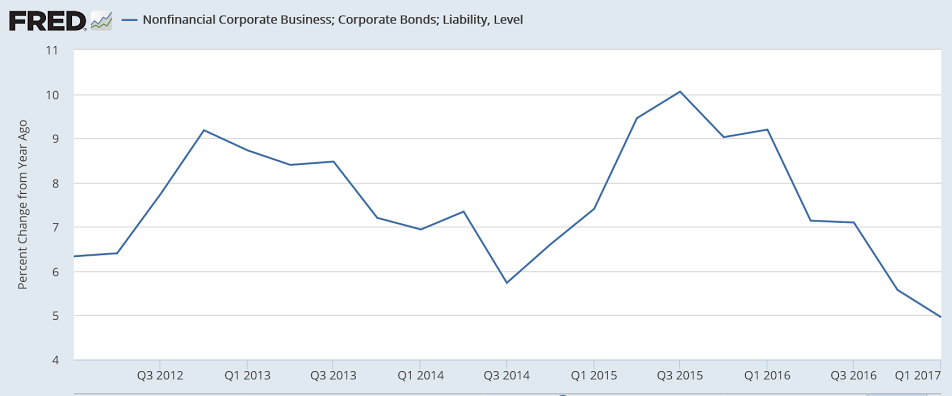

Corporate bonds are not picking up the slack- quite the opposite: