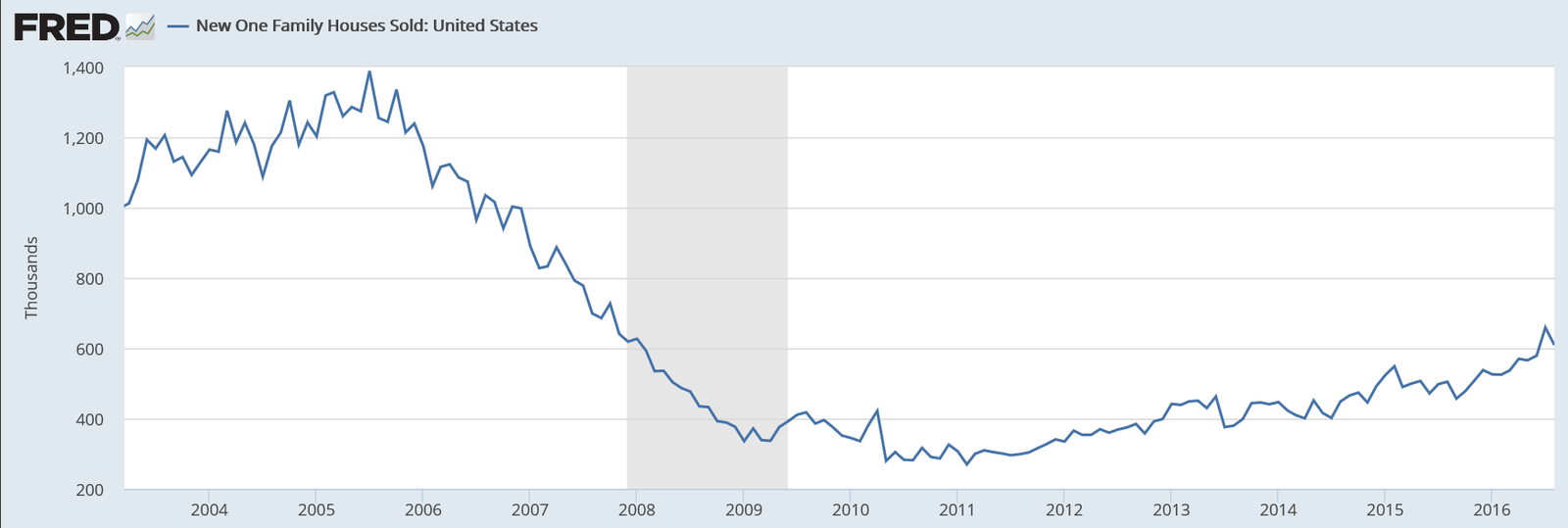

Settling back down. Without permit growth this isn’t going anywhere;

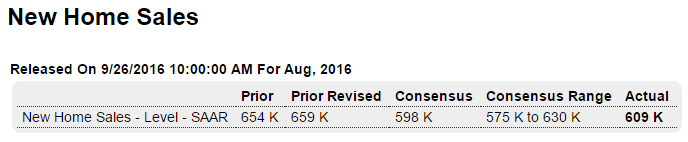

Highlights

New home sales may have fallen back by a monthly 7.6 percent in August, but the 609,000 annualized rate is still above Econoday’s consensus for 598,000. And a major plus in the report is a surprise 5,000 upward revision to July which now stands at a cycle high of 659,000 and a monthly gain from June of 13.8 percent. The volatility of this series had made a downward revision to July a major risk in today’s report.

Prices are coming down which points to builder discounting. The median, at $284,000, is down 3.1 percent on the month and down 5.4 percent on the year. Prices aren’t getting much lift from stubbornly low supply which is at 4.6 months. Total new homes for sale, at 235,000, did rise in the month but only slightly. Year-on-year, supply is up 8.3 percent which, however, is far under the 20.6 percent gain in year-on-year sales.

Sales strength is coming out of the West, a focused region for builders where the 162,000 annualized rate is up 8.0 percent on the month and a whopping 35.0 percent on the year. All other regions show monthly declines including the largest region which is the South where the 343,000 rate is down 12.3 on the month but still up 15.9 percent on the year.

This is a very positive report which underscores the accelerating strength of the new home market, strength that is making up for less far momentum on the resale side.

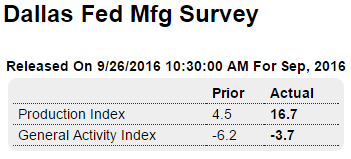

Highlights

The Dallas production index, at 16.7 in today’s September report, continues to remain positive despite weakness in underlying demand. The general activity index remains in the negative column, at minus 3.7 to extend its long uninterrupted negative streak that started with the 2014 collapse in oil prices. New orders are at minus 2.9 this month with backlog orders at minus 1.1. Hiring is flat and the Dallas sample continues to draw down inventories, in part reflecting the month’s strength in production but also tight management given what are only modestly positive expectations in future business strength. Price data show weakness in selling prices but gains for wages & benefits. This report isn’t uniformly negative and joins what have been similarly weak but still mixed reports from other regional Feds this month.