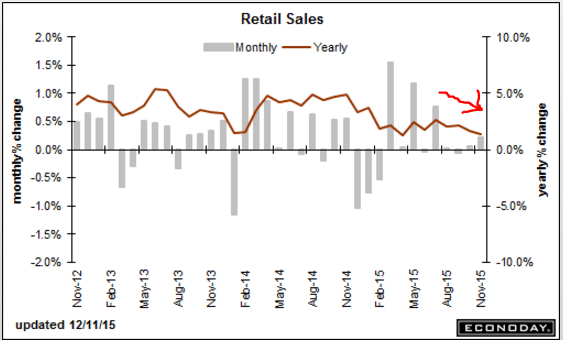

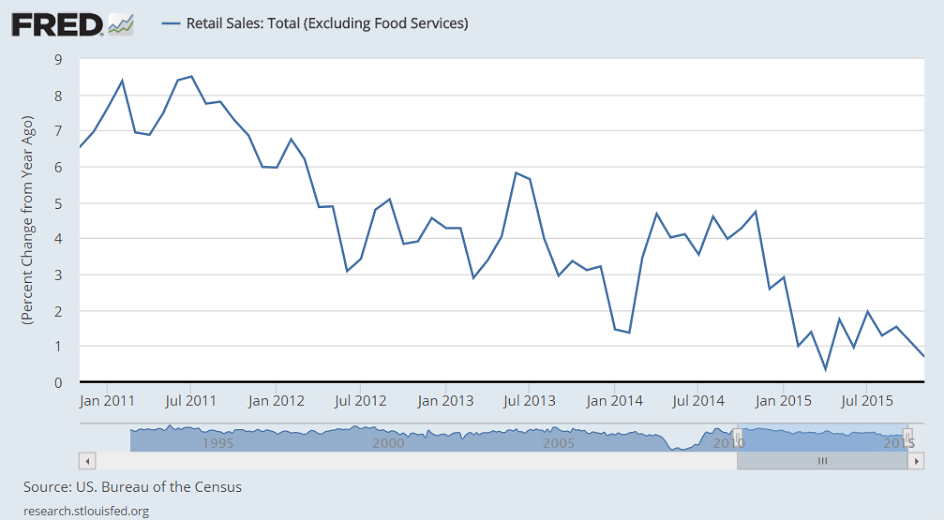

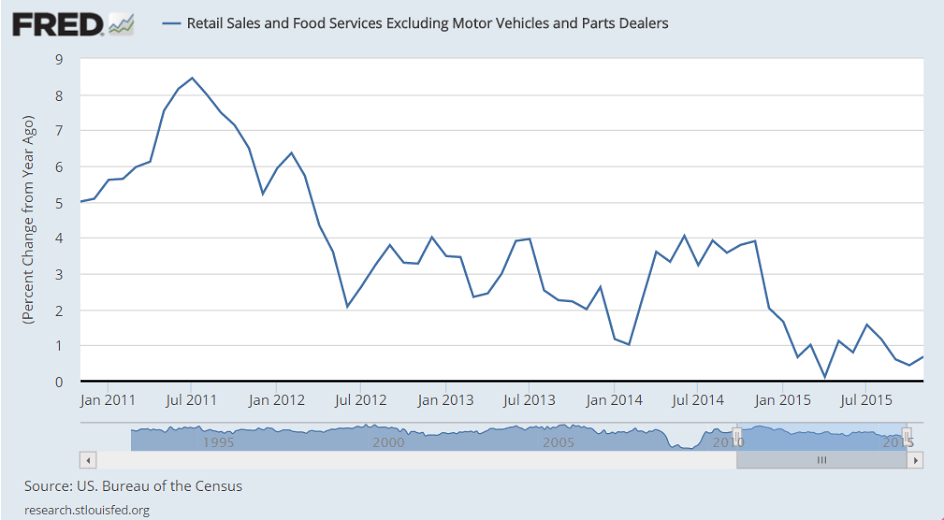

Retail sales = retail (gross) income and growth is still way down year over year, as per the charts.

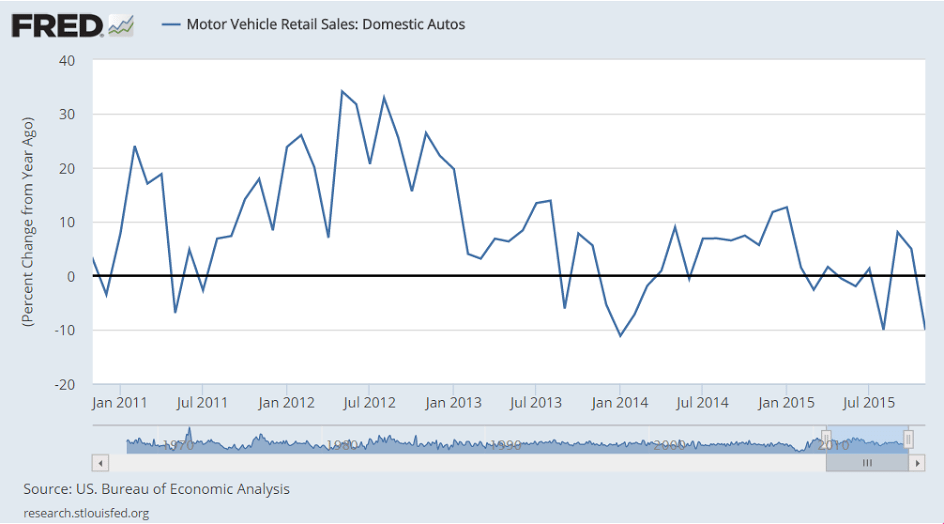

Also declining vehicle sales are highly problematic, as they were what was keeping a bad story from being that much worse. And not to forget when looking at year over year change oil and gas prices were already down quite a bit by this time last year:

Retail Sales

Highlights

Once again the headline for the retail sales report understates underlying strength. Total retail sales rose only 0.2 percent in November which is just under the Econoday consensus. But weakness here came from vehicles of all places which otherwise have been one of this year’s standout component for this report. Excluding vehicles, sales rose 0.4 percent which is 1 tenth above expectations. Excluding both vehicles and gasoline, core sales rose a very solid 0.5 percent which is 2 tenths above expectations. A key discretionary category, restaurants, shows yet another very strong gain, this at 0.7 percent in the month. Also showing sizable gains are electronics & appliances, clothing & accessories, non-store retailers (once again), and the general merchandise category where, despite a deflationary pull from falling import prices, sales jumped 0.7 percent in the month.

Vehicle sales fell 0.4 percent in the month on top of October’s 0.3 percent decline. These declines are a bit of a surprise given steady readings in unit sales of vehicles which have been holding firmly at 12-year highs. Whether there’s a rebound ahead for vehicle sales, which had been so strong through the year, will be key to consumer spending going into the new year. Sales at gasoline stations continue to contract, at minus 0.8 percent in the month. Furniture sales, which have been strong, fell back as did sales of building materials & garden supplies, which have been soft.

Year-on-year rates show nonstore retailers out in front, at plus 7.3 percent to confirm acceleration for online sales. Restaurants are right behind at plus 6.5 percent year-on-year followed by furniture and by sporting goods, both at plus 5.4 percent. All together, core retail sales are up a moderate 3.6 percent year-on-year held down by contraction in electronics & appliances and soft readings for grocery stores and general merchandise. Outside the core, motor vehicles are still in the thick of things, at plus 4.0 percent year-on-year, with gasoline stations down 19.9 percent. Total retail sales are up only 1.4 percent but the gain goes up to 3.6 percent (the same as the core) when excluding just gas.

Taken together, rates of growth are no more than moderate but certain areas are posting eye-catching results, results that point to what must have been a successful Black Friday sales push. The consumer, boosted by a solid labor market and having more money to spend because of low gas prices, is definitely alive and spending going into the final weeks of the holiday season. In a methodology note, the November data reflect a new sample and prior levels have been revised (mostly lower).

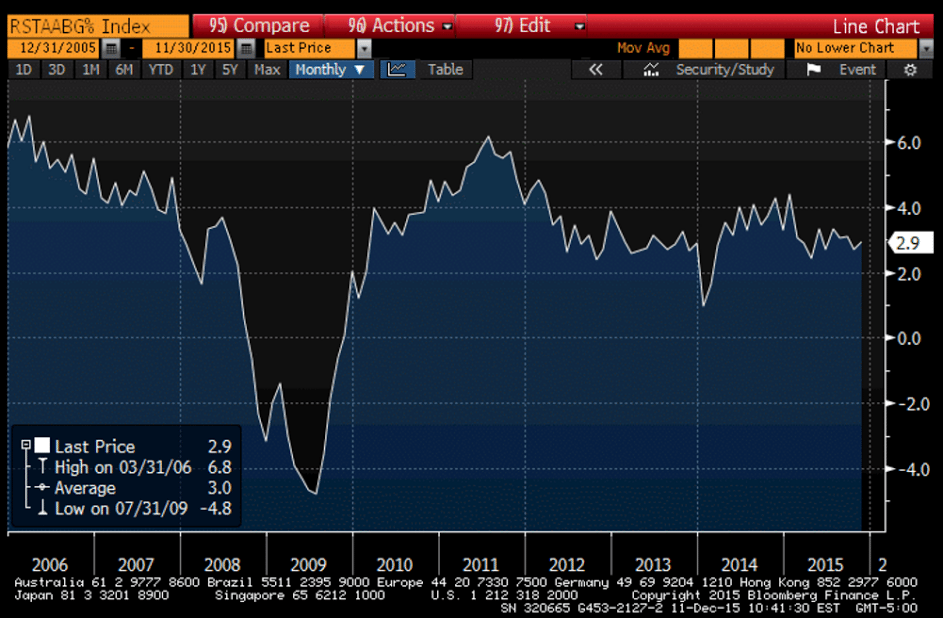

This one’s call the ‘control group’ (excludes auto dealers, gas stations, food services, building materials) and sure doesn’t look to me like it’s part of a rate hike story:

These came out Dec 3:

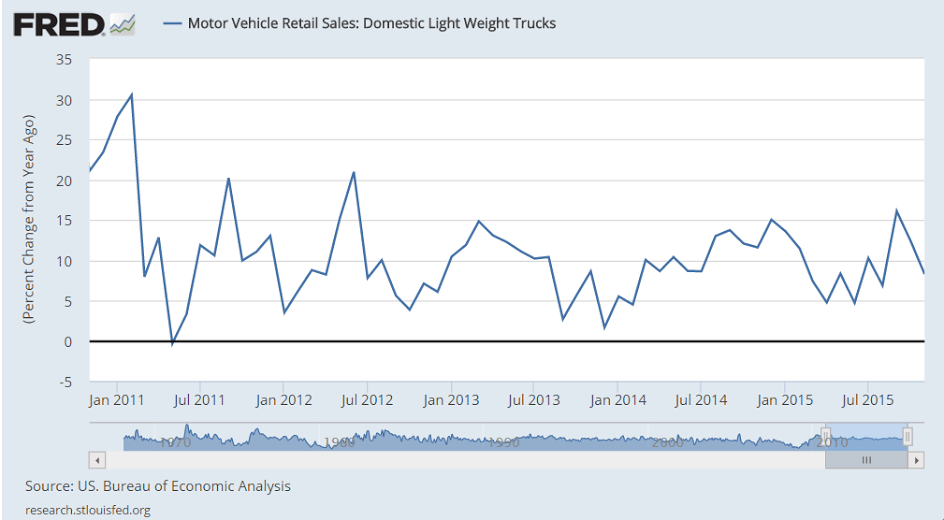

Trucks doing better:

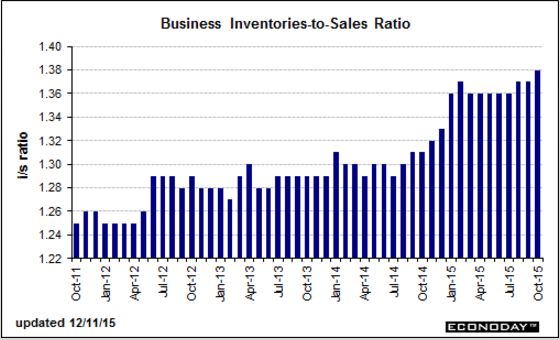

Inventory building stops but slow sales hike the inventory/sales ratio:

Business Inventories

Highlights

Businesses appear to be putting the brakes on inventories which however are still rising a bit relative to sales. Business inventories were unchanged in October with September revised down 2 tenths to plus 0.3 percent in readings that will pull down the GDP outlook slightly. Sales came in unchanged which is just enough to drive up the stock-to-sales ratio to 1.38 from 1.37. This time last year, this reading was at 1.31.

All three components show only the most minimal change in inventories, up 0.1 percent for retailers and down 0.1 percent for both manufacturers and for wholesalers. And sales tell the story, unchanged in October for both retailers and wholesalers and down 5 tenths for manufacturers.

The lack of punch in the economy, the result of weak foreign demand, continues to put upward pressure on inventories. But businesses are successfully keeping their stocks as low as possible, thereby limiting future corrections in production and employment.