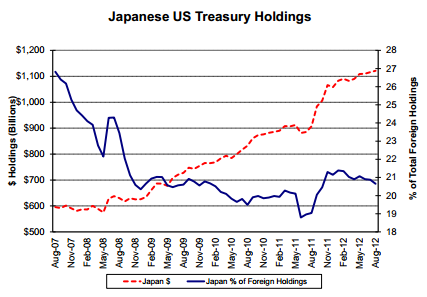

Seems this is what these charts would look like if Japan was selling yen to buy dollars and euro to support their exporters?

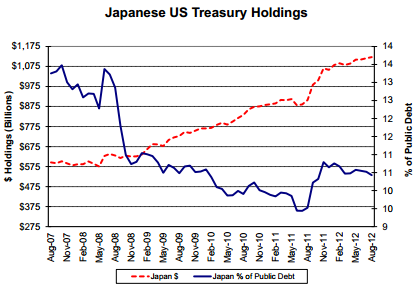

Seems this is what these charts would look like if Japan was selling yen to buy dollars and euro to support their exporters?