This release along with the Chicago Fed report that November housing starts were down, and anecdotal evidence from home builder reports and various mortgage originators seems to indicate the reported 22% jump in November housing starts reported last week is at best subject to downward revision.

MBA Purchase Applications

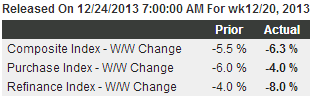

Highlights

The rise in mortgage rates, this time following the Fed’s decision to begin tapering stimulus, is increasingly reducing mortgage activity. The purchase index fell 4.0 percent in the December 20 week for a year-on-year decrease of 11.0 percent, tangible contraction that underscores the importance of all-cash buyers in the home market.

The rise in mortgage rates is also sharply reducing refinancing activity with the refinance index down 8.0 percent in the week to its lowest level of the recovery. The average rate for conforming mortgages ($417,500 or less) rose 2 basis points in the week to 4.64 percent.

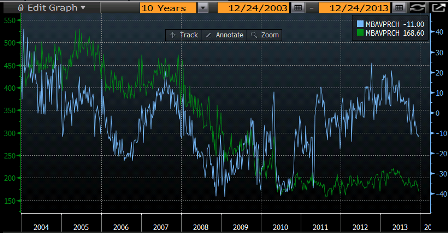

MBA Purchase Applications, Y/Y and level:

Full size image

Durables were up nicely as per yesterday’s release as well, with a boost from November’s elevated vehicle sales rate of 16.4 million units. But December car sales are currently forecast to be down to about a 15.5-16 million pace, vs month’s 16.4 million and October’s govt shutdown limited 15.2 million. This also brings the year over year growth rate down to maybe 4% as things flattened out in 2013 from higher prior growth rates. Also, as you can see from the chart, durables don’t tell you much about what might happen next. For example, we had about the same increase in Q1 2008:

Full size image

And the Capital goods non defense ex aircraft year over year chart speaks for itself as well:

Full size image

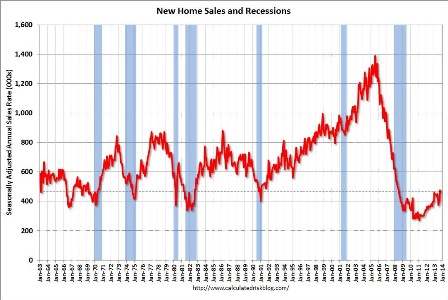

New home sales also just out, with a whopping upward 120,000 revision to last month causing today’s initial November print to be down tic. Seems it’s going to take a few more months of releases and revisions to see what’s actually been happening.

Full size image