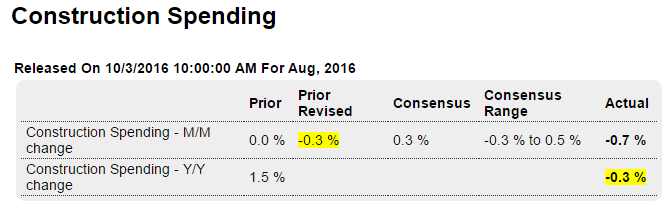

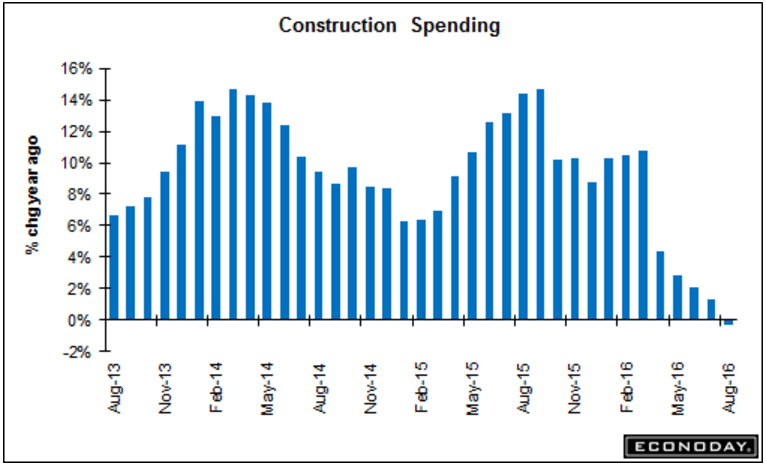

Worse than expected, prior month revised lower, and year over year now in contraction as the downtrend continues. Watch for further downward q3 GDP revisions:

Highlights

Multi-family units are just about the only strength in what is a weak construction spending report for August, down 0.7 percent on the month with July revised 3 tenths lower and into the negative column at minus 0.3 percent. Construction spending on new single-family homes fell 0.9 percent for the third monthly contraction in a row. This belies solid strength in new home sales and points to continued lack of supply in the new home market. But multi-family units are a different story, up 2.4 percent and, with July and June both revised higher, the fourth gain in a row. Strength here reflects expectations of strength for the rental market.

Nonresidential construction is weak across nearly all readings with commercial structures down 2.0 percent in the month, power down 1.5 percent, and manufacturing down 1.4 percent. These readings all reflect lack of business investment which is the economy’s stubbornly weak suit. Public spending is also weak, down 0.4 percent for educational structures and down 2.9 percent for highways and roads. Positives are hard to find but do include a 2.3 percent gain in office structures and a 4.0 percent rise in federal structures, the latter offset by a 2.5 decline at the state & local level.

Year-on-year rates confirm the weak trends with single-family homes down 1.5 percent and total construction spending down 0.3 percent. The big plus here, once again, is multi-family units where year-on-year spending is up a robust 13.9 percent. But multi-family units make up only 5 percent of total construction spending which otherwise is not having a great year.

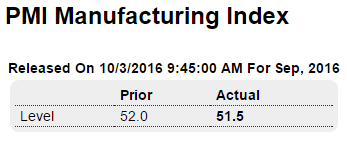

Manufacturing seems to be settling into a modestly positive stance, but not adding to GDP growth they way it had last year:

Highlights

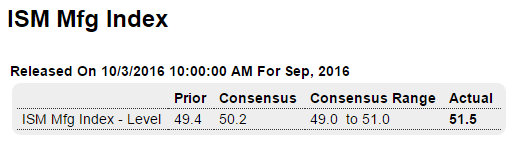

September was another slow month for Markit’s U.S. manufacturing sample with the composite index slipping 5 tenths from August to 51.5. New orders slowed to the weakest growth rate of the year while export sales contracted for the first time in four months which the report ties to strength in the dollar. Production slowed to a 3-month low, hiring during the month was soft, and the sample continues to cut inventories which indicates lack of confidence in the business outlook. One plus in the report is a slight increase in backlog orders. Otherwise, pluses are hard to find in this report. Input costs are up slightly and selling prices continue to slip. Unlike other reports, this report is citing the presidential election as a factor, specifically a negative one that it says is delaying customer decisions. Watch for the ISM manufacturing report later this morning at 10:00 a.m. ET.

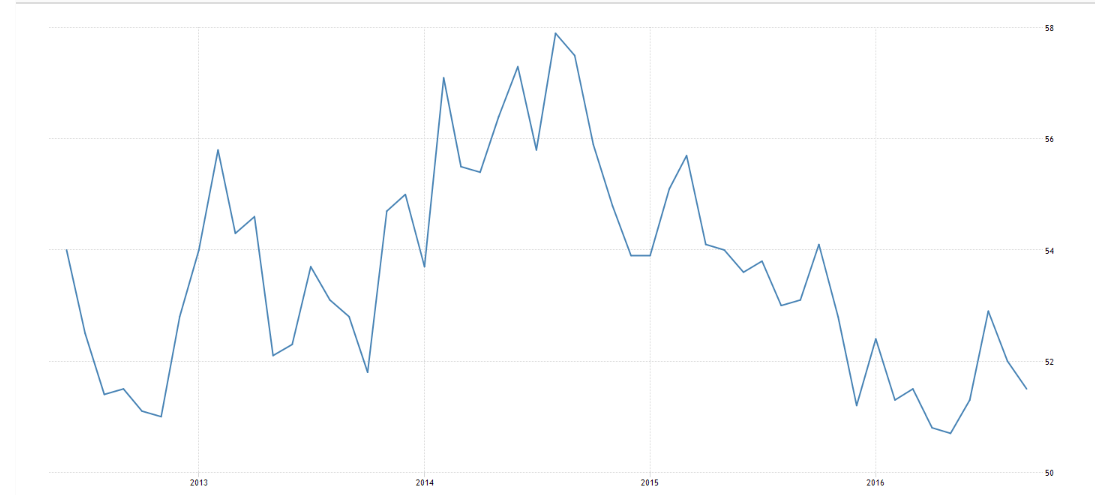

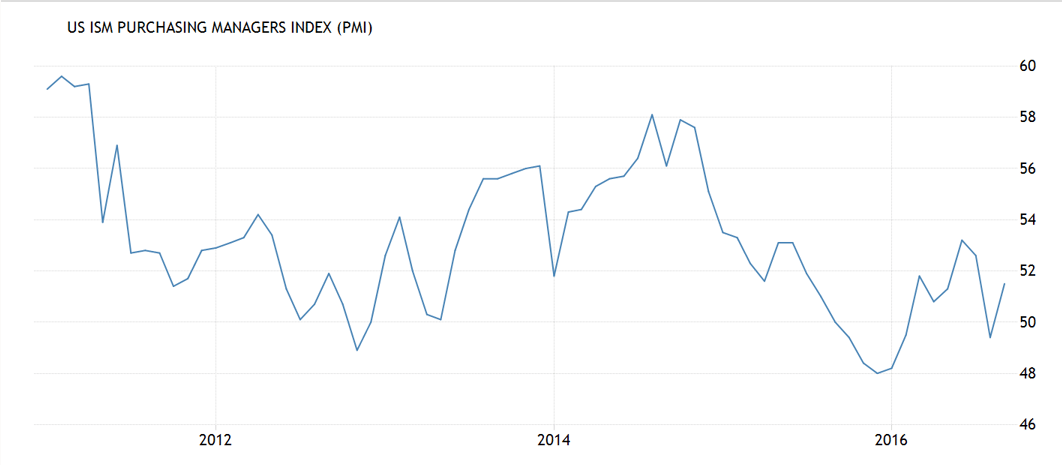

Settling in at lower levels, while employment is still in contraction:

Highlights

August proved to be a one-month letdown for ISM’s manufacturing sample as the September index bounced more than 2 points higher to a much better-than-expected 51.5. New orders are the most important of all readings and they lead the September report, rising 6 points to a very solid 55.1. Export orders are respectable and steady at 52.0 while the draw in total backlog orders slowed, with this index up 4 points and nearly hitting breakeven 50 at 49.5. Production also improved in the month, up 1.4 points to 52.8, as did employment which, at 49.7, is also nearly at 50. This is a positive report, pointing to rising though no more than moderate strength for the nation’s factory sector.

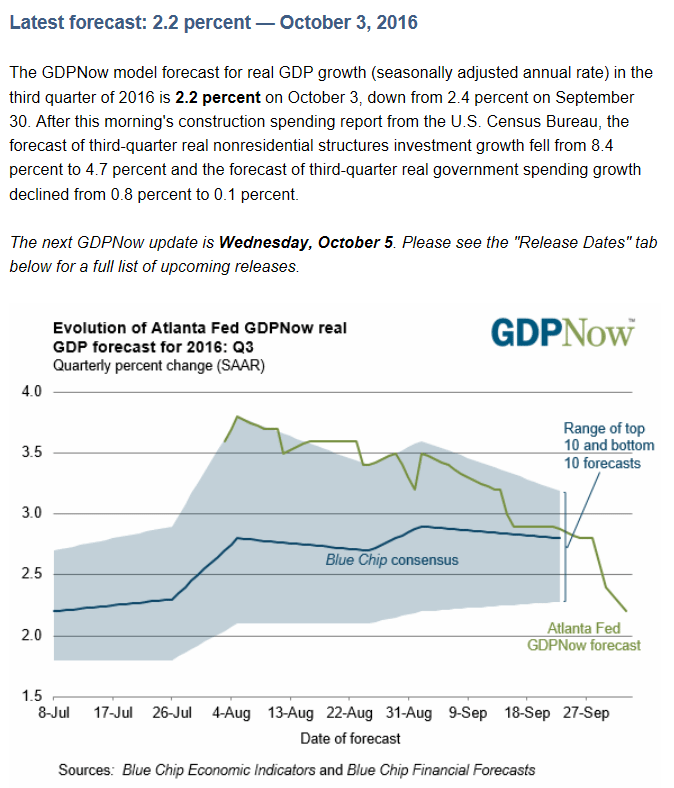

Down yet again.

Remember the cheerleading when it was at 3.8?

;)