Andea Terzi is a former student of Paul Davidson, now a professor of economics at Franklin College, Lugano, Switzerland.

The institutional structure in the euro zone has been it’s own undoing since inception, very much like we all described at that time.

Current policy responses continue to support the same repressive fiscal policies that again look to be driving the otherwise prosperous euro zone into negative GDP growth.

The glimmer of hope may be that they have discovered the sector balance approach.

The next step in the right direction would be a recognition of the actual causations.

From Professor Tezi:

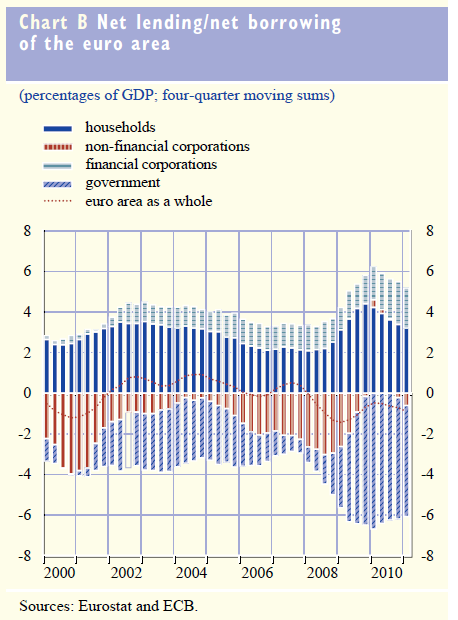

Does the ECB understand sector financial balances?The August 2011 Monthly Bulletin of the European Central Bank has an interesting chart of financial balances of different sectors in the euro area. The chart is reproduced below.

The figure shows how rising deficits in Europe in 2008 and 2009 have produced higher net financial savings in the private sector.

This is evidence that automatic (anti-cyclical) stabilizers worked as usual: as growth declines, or goes negative, tax revenues fall, government deficits increase, and this stops the economy from falling further. This can only work, however, until market-constrained governments in the euro area begin acting pro-cyclically. Governments acting pro-cyclically during recessions means that deficit reductions will reduce private savings below the desired level, and this means a further fall of demand and incomes.

Looking at 2010, and considering that the euro area’s current account balance is marginally negative, there is evidence of this pro-cyclical effect, as government deficits declined, and net private lending inevitably declined.

What is remarkable is how the ECB interprets the chart:

With euro area total investment growing faster than saving, the net borrowing of the euro area increased (to 0.9% of GDP, expressed as a four-quarter sum). From a sectoral point of view, this masked further rebalancing between sectors, with another reduction in government net borrowing (the government de?cit falling to 5.5% of GDP on a four-quarter moving-sum basis, from a peak of 6.7% in the ?rst quarter of 2010) and a further decline in households net lending, while the net borrowing of NFCs increased sharply. (ECB, Monthly Bulletin, August, 2011, pp. 37-8)

The ECB is assuming that savings are needed to finance investment and sector rebalancing is always a good thing. And it makes no reference to the connection between financial balances and nominal GDP growth.

In plain language, this is what the ECB is telling us:In 2010, Euro area’s savings were insufficient to finance investment. Business needed to borrow to finance their investments and households savings were not enough to fill the gap. This is why the euro area runs a current account deficit, and is a net borrower. European governments, however, are doing their part by reducing their own net borrowing, thus contributing to a progressive rebalancing in financial deficits/surpluses across sectors.

For the ECB, the government net borrowing bar getting shorter (in the chart above) is a reason for optimism. In our reading, this optimism is unwarranted, and what the ECB calls “rebalancing between sectors” is a most worrying financial development of the euro area.