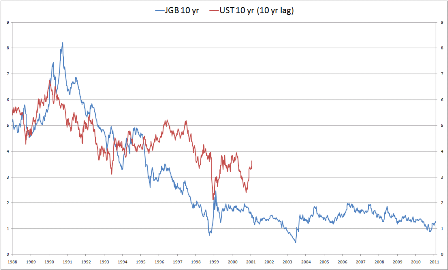

Because we believe we can be the next Greece, we continue to work to turn ourselves into the next Japan?

Japan’s surplus years were 1987-92, ours were about 10 years later from 1997 to 2001.

Both ended in stock market crashes and lower rates.

Because we believe we can be the next Greece, we continue to work to turn ourselves into the next Japan?

Japan’s surplus years were 1987-92, ours were about 10 years later from 1997 to 2001.

Both ended in stock market crashes and lower rates.