Perspective

by Steve Hanke

US Mercantilist Machismo, China replaces Japan

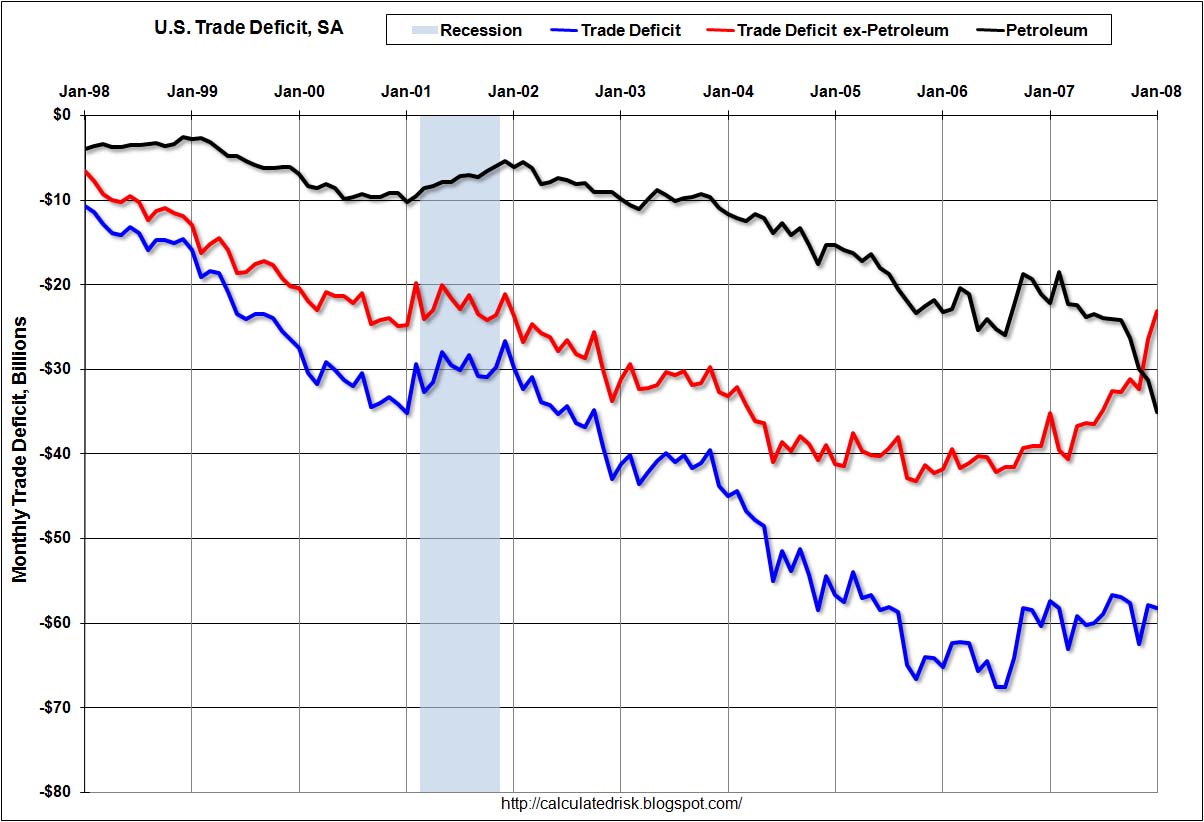

The United States has recorded a trade deficit in each year since 1975.

That is a good thing – exports are real costs, imports benefits.

This is not surprising because savings in the US have been less than investment.

This is a tautology from the above misconceived notion and of no casual consequence.

The trade deficit can be reduced by some combination of lower government consumption, lower private consumption

Yes, if we get less net goods and services from non residents, our trade deficit goes down, as does our real terms of trade and our standard of living.

Real terms of trade are the real goods and services you export versus the real goods and services you import.

In economics, it is better to receive (real goods and services) than to give.

or lower private domestic investment.

We could (and would if ‘profitable’) ‘borrow to invest’ domestically (loans ‘create’ deposits, not applicable/no such thing as ‘borrowing from abroad’ etc.)

But said, domestic borrowing decreases ‘savings’ equal to the increased domestic investment (accounting identity). So, the trade gap would remain the same if we invested more or less via domestic funding.

So, his above statement is a tautology of no casual interest.

But you wouldn’t know it from listening to the rhetoric of Washington’s politicians and special interest groups. Many of them are intent on displaying their mercantilist machismo. This is unfortunate. A reduction of the trade deficit should not even be a primary objective of federal policy. Never mind. Washington seems to thrive on counter-productive trade “wars” that damage both the US and its trading partners.

Almost sounds like he gets it! But don’t get your hopes up..

From the early 1970s until 1995, Japan was an enemy. The mercantilists in Washington asserted that unfair Japanese trading practices caused the US trade deficit and that the US bilateral trade deficit with Japan could be reduced if the yen appreciated against the dollar.

Washington even tried to convince Tokyo that an ever-appreciating yen would be good for Japan. Unfortunately, the Japanese

complied and the yen appreciated, moving from 360 to the greenback in 1971 to 80 in 1995. In April 1995, Secretary of the Treasury Robert Rubin belatedly realized that the yen’s great appreciation was causing the Japanese economy to sink into a deflationary quagmire.

Actually, it was the fiscal surplus they allowed from 1987-1992 that drained net yen income and financial assets that removed support for the yen credit structure and ended the expansion.

In consequence, the US stopped arm-twisting the Japanese government about the value of the yen and Secretary Rubin began to evoke his now-famous strong-dollar mantra. But while this policy switch was welcomed, it was too late. Even today, Japan continues to suffer from the mess created by the yen’s appreciation.

The mess was created by the surplus and repeated attempts to reduce the following countercyclical deficits. Only when the deficit was left alone and grew to 7% of GDP a few years ago did the economy finally get the net income and financial assets it needed to recover. Only to be undermined recently by a political blunder regarding building codes. Japan should do better in 2008, as that obstacle is overcome.

As Japan’s economy stagnated, its contribution to the increasing US trade deficit declined, falling from its 1991 peak of almost 60% to about 11%.

Sad to see that happens. Now Americans have to build the cars here as their new factories are now in the US.

While Japan’s contribution declined, China’s surged from slightly more than 9% in 1990 to almost 28% last year.

Yes, they have workers willing to consume fewer calories than those in Japan.

With these trends, the Chinese yuan replaced the Japanese yen as the mercantilists’ whipping boy. Interestingly, the combined Japanese–Chinese contribution has actually declined from its 1991 peak of over 70% to only 39% last year. This hasn’t stopped the mercantilists from claiming that the Chinese yuan is grossly undervalued, and that this creates unfair Chinese competition and a US bilateral trade deficit with China.

The unfair part is their workers are willing to work for a lot less real consumption and become the world’s slaves via net exports.

And we don’t know how to sustain our own domestic demand via internal policy; so, our politicians blame the foreigners.

I was introduced to the Chinese currency controversy five years ago when I appeared as a witness before the US Senate Banking Committee on May 1, 2002. The purpose of those hearings was to determine, among other things, whether China was manipulating its exchange rate.

All state currencies are public monopolies, and value is a function of various fiscal/monetary policies. So in that sense, all currencies are necessarily ‘manipulated’ as all monopolists are inherently ‘price setters’.

So, this entire point is moot, though far from mute.

United States law requires the US Treasury Department, in consultation with the International Monetary Fund, to report biyearly as to whether countries – like China – are gaining an “unfair” competitive advantage in international trade by

manipulating their currencies.

Clearly no understanding that exports are real costs, and imports are real benefits. The entire worlds seems backwards on this.

The US Treasury failed to name China a currency manipulator back in May 2002, and it hasn’t done so since then. This isn’t too surprising since the term “currency manipulation” is hard to define and, therefore, is not an operational concept that can be used for economic analysis. The US Treasury acknowledged this fact in reports to the US Congress in 2005. But this fact has not stopped politicians and special interest groups in the United States, and elsewhere, from asserting that China manipulates the yuan.

Yes, to keep their wages low so they can produce, and we can consume.

Protectionists from both political parties in the US have threatened to impose tariffs on imported Chinese goods if Beijing does not dramatically appreciate the yuan. These protectionists even claim that China would be much better off if it allowed the yuan to become stronger vis-à-vis the US dollar.

They would – it would lower their net exports, a real benefit at the macro level.

Percenta

This is not the first time US special interests have made assertions in the name of helping China. During his first term, Franklin D. Roosevelt delivered on a promise to do something to help silver producers. Using the authority granted by the Thomas Amendment of 1933 and the Silver Purchase Act of 1934, the Roosevelt Administration bought silver.

Can’t think of a better way to help a producer!

This, in addition to bullish rumors about US silver policies, helped push the price of silver up by 128% (calculated as

an annual average) in the 1932-35 period.

(It has gone up more here in the last three years without the government buying any.)

Bizarre arguments contributed mightily to the agitation for high silver prices. One centered on China and the fact that it was on the silver standard. Silver interests asserted that higher silver pricesâ€â€Âwhich would bring with them an appreciation in the yuanâ€â€Âwould benefit the Chinese by increasing their purchasing power.

Yes – whoever is long silver wins when the price goes up.

As a special committee of the US Senate reported in 1932, “silver is the measure of their wealth and purchasing power; it serves as a reserve, their bank account. This is wealth that enables such peoples to purchase our exports.”

Things didn’t work according to Washington’s scenario. As the dollar price of silver and of the yuan shot up, China was thrown into the jaws of depression and deflation. In the 1932-34 period, gross domestic product fell by 26% and wholesale prices in the capital city, Nanjing, fell by 20%.

In an attempt to secure relief from the economic hardships imposed by US silver policies, China sought modifications in the US

Treasury’s silver purchase program.

They didn’t know how to sustain domestic demand. They needed to float the currency, offer a public service job at a non disruptive wage to anyone willing and able to work, and leave the overnight risk free rate at 0%. (See ‘Full Employment and Price Stability‘.)

But its pleas fell on deaf ears.

Maybe ears with different special interests?

After many evasive replies, the Roosevelt Administration finally indicated on October 12, 1934 that it was merely carrying out a policy mandated by the US Congress. Realizing that all hope was lost, China was forced to effectively abandon the silver standard on October 14, 1934, though an official statement was postponed until November 3, 1935.

About the same time the US abandoned the gold standard domestically for much the same reason.

This spelled the beginning of the end for Chiang Kaishek’s Nationalist government.

He let unemployment go too high out of ignorance of how to sustain domestic demand. A common story throughout history.

History doesn’t have to repeat itself. Foreign politicians should stop bashing the Chinese about the yuan’s exchange rate. This would allow the Chinese to focus on important currency and trade issues: making the yuan fully convertible, respecting intellectual property rights and meeting accepted health and safety standards for their exports.

Why do we want to encourage anything that reduces their net exports???

(rhetorical question)

Steve H. Hanke is a Professor of Applied Economics at The Johns Hopkins University in Baltimore and a Senior Fellow at the Cato Institute in Washington, D.C.

♥

{kind=link}