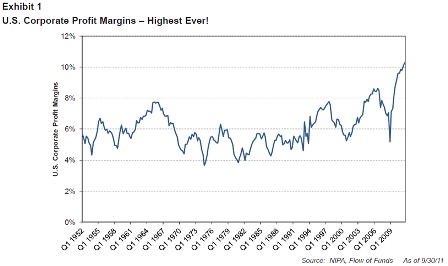

They have certainly had their ups and downs:

Click here for larger version

>

> (email exchange)

>

> Warren, what do u think stocks do here?

>

Been bearish all along from mid March and still thinking same.

Euro zone still melting down.

US coming off Q4 rebuild of Japan’s pipeline.

And now unemployment benefits expiring in 9 states with more to come?

State and local cutbacks are ‘high multiple’ and actual state and local deficit spending coming down as well?

Housing not picking up enough to add meaningfully to aggregate demand/GDP.

With ‘real productivity’/technology and management advances’ continually reducing labor needed per unit of output, recent declines in productivity in line with softer employment?

Global austerity = global slow motion train wreck?

So still looking to me like a case of

‘Because we fear becoming the next Greece, we continue to turn ourselves into the next Japan’

The only way out at this point is a private sector credit expansion, which, in the US, traditionally comes from housing, but doesn’t seem to be happening this time. Past cycles have seen it come from the sub prime expansion phase, the .com/y2k boom, the S&L expansion phase, and the emerging market lending boom.

But this time we’re being more careful of ‘bubbles’ (just like Japan has done for the last two decades). So I don’t see much hope there.

Still watching for the euro bond tax idea to surface, which I see as the immediate possibility of systemic risk, but no real sign yet.

The issues I’ve been discussing over the last year or two while now crystallizing, remain highly problematic.

The idea of Greek default transformed from being a Greek punishment to a gift, with the pending question: ‘If Greece doesn’t have to pay, why do I?’- threatening a far more disruptive outcome that is yet to be fully discounted.

That is, should Greek bonds be formally discounted, the consequences of merely the political discussion of that question will be all it takes to trigger a financial crisis rivaling anything yet seen.

And note, also as previously discussed, that there has yet to be an actual Greek default, and that all Greek bonds have continued to mature at par, as there has yet to be an acceptable alternative.

So what are the alternatives?

1. Continue to fund Greece with terms and conditions.

2. Don’t fund Greece which forces:

a. Greece is forced to limit spending to actual tax revenues

b. Greece moves back to the drachma

And what are the ‘terms and conditions’?

Austerity is always the lead demand, which slows both the Greek economy and to some extent the euro zone in general.

Additional demands currently include discounting Greek bonds to bring down their debt to GDP ratio to ‘sustainable’ levels. However, after 8 months of negotiations, this has proven highly problematic, probably for reasons yet to be fully disclosed. And, as just discussed, there may be a growing awareness that discounting opens Pandora’s box with the politically attractive question ‘if Greece doesn’t have to pay, why do we?’

So what actually happens?

My best guess, and not with a lot of conviction, is that nothing is concluded before the coming maturity dates, and the ECB winds up writing the check to support short term Greek funding to buy more time for more inconclusive discussion. So, again as previously discussed, seems like this is the solution- death by 1,000 cuts and reluctant ECB bond buying when push comes to shove to keep it all going.

And, currently, the catastrophic risk I’d highly recommend immediately hedging is the risk that Greek bonds are formally discounted, rapidly followed by a global discussion of ‘so why should we have to pay?’ Possible immediate consequences of that discussion include a sharp spike in gold, silver, and other commodities in a flight from currency, falling equity and debt valuations, a banking crisis, and a tightening of ‘financial conditions’ in general from portfolio shifting, even as it’s fundamentally highly deflationary. And while it probably won’t last all that long, it will be long enough to seriously shake things up.

Once again, management is quick to sell the shareholders down the river with a fat coupon, low strike, dilutive preferred.

This is one of the inherent risks of being a common shareholder under current law.

It keeps stocks cheaper than otherwise, which makes them more attractive as takeover candidates, as

when you own the whole thing you don’t have this risk.

BUS 08/25 13:10 Berkshire Hathaway to Invest $5 Billion in Bank of America

BN 08/25 13:12 *BERKSHIRE WARRANTS FOR 700M SHRS EXERCISE PRICE $7.142857/SHR

BN 08/25 13:10 *BOFA TO SELL 50,000 SHRS PFD, LIQUIDATION VALUE $100K/SHR

BN 08/25 13:10 *BERKSHIRE HATHAWAY TO GET WARRANTS TO BUY 700M SHRS :BAC US

BN 08/25 13:10 *BERKSHIRE HATHAWAY TO INVEST $5B IN BANK OF AMERICA :BAC US

BN 08/25 13:10 *BOFA TO SELL 50,000 SHRS PFD :BAC US

BN 08/25 13:10 *BOFA TO SELL 50,000 SHRS :BAC US

BN 08/25 13:10 *BERKSHIRE HATHAWAY TO INVEST $5B IN BANK OF AMERICA

Berkshire Hathaway to Invest $5 Billion in Bank of America

By JoAnne Norton

August 25 (Bloomberg) — Berkshire Hathaway Inc. agreed to

buy 50,000 preferred shares of Bank of America Corp. for $5

billion, the bank said today in a statement.

From Goldman:

Published August 8, 2011

* Following Friday’s downward revisions, we now expect real GDP to increase just 2%-2½% (annualized) through the end of 2012 and the unemployment rate to rise slightly to 9¼% during this period.

This is still higher than the first half, so presumably corporations will have a better second half as well, and they did just fine in the first half.

And with lower gasoline prices, consumers get a nice break there which should firm their spending on other things as well.

The tighter fiscal won’t matter for this year, and markets won’t discount what may happen in November until it’s closer to actually happening.

So still looks to me like the recent sell off in stocks was mainly technical, as the initial knee jerk sell off from the debt ceiling and downgrade uncertainties triggered further selling by those with short options positions, much like the crash of 1987.

And, like then, and unlike early 2008, the current federal deficit seems more than large to me to keep things chugging along at muddle through levels of modest growth, continued too high unemployment, and decent corporate profits and investment.

Yes, risks remain. Europe is a continuous risk, but the ECB, once again, stepped in and wrote the check. China looks to be slipping but the lower commodity prices will help US consumers maybe about as much as they hurt the earnings of some corps.

So for now, with the options related stock selling over, it looks like we’re back to calmer waters for a while.

And Congress goes back to trying to cut the deficit to put people back to work.

Someone needs to tell them they haven’t run out of dollars, they aren’t dependent on China, and they can’t become the next Greece, and so yes, the deficit is too small given the current output gap.

But until then, we keep working to become the next Japan.

Below are various commodity indices.

If China was in fact melting down in the second half of this year due to cut backs in state spending and lending, and that front loaded into the first quarter, it would look something like that before breaking further.

The Australian dollar is likewise falling, indicating shifting circumstances at China’s coal mine as well.

While good for the US consumer and US domestic demand, it’s not good for the earnings of quite a few

major corporations.

It’s also good for the dollar, which is also not good for corporate foreign earnings translations.

It also brings down headline inflation and could help moderate core CPI as well.

And if China doesn’t like US Fed style QE, ECB style QE- buying member nation debt- has to be all the more distasteful,

and could shift their reserve preference away from the euro.

Especially as the ECB check writing escalates much like it did when it supported the banking system’s liquidity. In theory the ECB’s check writing for the national govts could approach the size of the US budget deficit. Somewhat as ECB liquidity support for the euro member banks is analogous to FDIC insurance for the US banking system.

With the US budget deficit chugging along at about 9% of GDP, domestic demand and earnings should be no worse than they were in the first half of this year, as previously discussed, which means equities should be ok in general, though with some names benefiting as others get hurt.

I tend to agree with this update from Art.

The global equity sell off seems beyond anything related to the S&P downgrade

and more likely China and commodity related. Note the recent fall in the $A for example.

There’s a new post on our site discussing the terrible performance of Asian stock markets this morning, on the first major trading day following Standard & Poor’s downgrade of the U.S. government’s credit rating. The media is widely assuming the selloff in Asia is all related to the downgrade, but I think that’s a pretty flimsy argument. Seems more likely to be related to China and/or Europe. We’ll have a better idea once European markets open. The post is linked and excerpted below. If you have any questions or concerns, let me know. Have a great week!

Asia Down Big: US Downgrade or China Cracking?

Market chatter has been focused on the impact that Standard & Poor’s downgrade of U.S. government’s credit rating on Friday afternoon would have on markets this week. If you follow our blog, you already know where we stand on S&P’s decision—it’s an utter joke. And while other markets have shown some volatility since Friday, it didn’t seem to have much of a negative impact. That’s as we expected.

However, Asian markets sold off brutally at the start of this week’s trading. The knee-jerk media interpretation is that it’s S&P-driven, but that’s not a satisfying explanation in my view. Given how the sell-offs are unfolding, it looks like it could be China-related. The Shanghai stock market is now officially in bear market territory, and smart market watchers have been predicting that China could soon experience a financial crisis, as its system is reportedly quite levered-up and fragile.

If so, this is NOT good for the global economic and risky asset outlooks. Throw one more nut on the bear claw. And China is a big nut—a lot of companies around the world depend on demand out of China, either directly or indirectly, to support current operating performance. Take that down significantly and stock market valuations suddenly look a lot richer.

Of course, it could be Europe too. And we’ve recently seen short-term interest rates go negative, an occurrence that presaged the last global financial crisis. We’re keeping a close eye on things as they unfold.

+++

In other news, Friday saw what appeared to be rather healthy payrolls and consumer credit reports. However, digging below the headlines, temporary hirings (along with measures of temp help demand from other sources) are still falling, and they tend to lead payrolls higher or lower. And underlying trends in consumer confidence indicate that the notable jump in consumer credit, though it could run for another few quarters, should be short-lived.

Work that I did with some of our strategy models over the weekend indicates that recession is going to be almost a sure thing as July and August data is fed in, and we’re currently predicting a start date between February 2012 and January 2013. Also looks, based on NYSE margin data, like the S&P 500 could fall another 10% to 30% from here, with a bear market running from May 2011 (some would date it back to 2007) through as late as mid-2013. A bear market starting roughly half a year before recession would fit historical patterns rather well, unfortunately.

One piece that is arguing emphatically against recession is the Treasury curve, which is still historically steep after last week’s flattening. However, (1) Japan’s first follow-on recession started with the term spread at around 200 basis points (unheard of up until then) and it has had two additional recessions without its yield curve ever inverting, and (2) we simply don’t expect term spreads to have much predictive power in a zero interest rate environment. Interbank funding in the U.S. is still at safe levels, but there are definitely incipient signs of stress. Everything else is on the verge of triggering a recession warning.

Depending upon what unfolds in China, Europe, and the upcoming U.S. austerity negotiations (and the ever-present unknown unknowns), recession could unfold far sooner and faster than almost anyone thinks. Forceful policy actions could do a great deal to stem the tide, but there seems to be almost no political will to do anything, probably due to the mistaken belief that governments everywhere are ‘out of bullets’.

At levels below 900 on the S&P500, we would probably start to lean heavily toward equities—unless a balanced budget amendment to the U.S. Constitution makes significant progress, in which case we’ll recommend cash and long-term Treasuries across all or most of our clients’ accounts.

Best regards,

Art

IMPORTANT DISCLOSURES: Symmetry Capital Management, LLC (“SCM”) is a Pennsylvania registered investment advisor that offers discretionary investment management to individuals and institutions. This publication is for informational, educational, and entertainment purposes only. It is not an offer to sell or a solicitation to buy securities, or to engage in any investment strategy. The firm and some of its clients hold some positions that are expected to increase in value if stock markets decline.

It doesn’t look to me like anything particularly bad has actually yet happened to the US economy.

The federal deficit is chugging along at maybe 9% of US GDP, supporting income and adding to savings by exactly that much, so a collapse in aggregate demand, while not impossible, is highly unlikely.

After recent downward revisions, that sent shock waves through the markets, so far this year GDP has grown by .4% in Q1 and 1.2% in Q2, with Q3 now revised down to maybe 2.0%. Looks to me like it’s been increasing, albeit very slowly. And today’s employment report shows much the same- modest improvement in an economy that’s growing enough to add a few jobs, but not enough to keep up with productivity growth and labor force growth, as labor participation rates fell to a new low for the cycle.

And, as previously discussed, looks to me like H1 demonstrated that corps can make decent returns with very little GDP growth, so even modestly better Q3 GDP can mean modestly better corp profits. Not to mention the high unemployment and decent productivity gains keeping unit labor costs low.

Lower crude oil and gasoline profits will hurt some corps, but should help others more than that, as consumers have more to spend on other things, and the corps with lower profits won’t cut their actual spending and so won’t reduce aggregate demand.

This is the reverse of what happened in the recent run up of gasoline prices.

Japan should be doing better as well as they recover from the shock of the earthquake.

Yes, there are risks, like the looming US govt spending cuts to be debated in November, but that’s too far in advance for today’s markets to discount.

A China hard landing will bring commodity prices down further, hurting some stocks but, again, helping consumers.

A euro zone meltdown would be an extreme negative, but, once again, the ECB has offered to write the check which, operationally, they can do without limit as needed. So markets will likely assume they will write the check and act accordingly.

A strong dollar is more a risk to valuations than to employment and output, and falling import prices are very dollar friendly, as is continuing a fiscal balance that constrains aggregate demand to the extent evidenced by the unemployment and labor force participation rates. And Japan’s dollar buying is a sign of the times. With US demand weakening, foreign nations are swayed by politically influential exporters who do not want to let their currency appreciate and risk losing market share.

The Fed’s reaction function includes unemployment and prices, but not corporate earnings per se. It’s failing on it’s unemployment mandate, and now with commodity prices coming down it’s undoubtedly reconcerned about failing on it’s price stability mandate as well, particularly with a Fed chairman who sees the risks as asymmetrical. That is, he believes they can deal with inflation, but that deflation is more problematic.

So with equity prices a function of earnings and not a function of GDP per se, as well as function of interest rates, current PE’s look a lot more attractive than they did before the sell off, and nothing bad has happened to Q3 earnings forecasts, where real GDP remains forecast higher than Q2.

So from here, seems to me both bonds and stocks could do ok, as a consequence of weak but positive GDP that’s enough to support corporate earnings growth, but not nearly enough to threaten Fed hikes.

Consumer borrowing up in June by most in 4 years

By Martin Crutsinger

May 25 (Bloomberg) — Americans borrowed more money in June than during any other month in nearly four years, relying on credit cards and loans to help get through a difficult economic stretch.

The Federal Reserve said Friday that consumers increased their borrowing by $15.5 billion in June. That’s the largest one-month gain since August 2007. And it is three times the amount that consumers borrowed in May.

The category that measures credit card use increased by $5.2 billion — the most for a single month since March 2008 and only the third gain since the financial crisis. A category that includes auto loans rose by $10.3 billion, the most since February.

Total consumer borrowing rose to a seasonally adjusted annual level of $2.45 trillion. That was 2.1 percent higher than the nearly four-year low of $2.39 trillion hit in September.