Post war deceleration seems to be on track.

Debt/GDP falling fast as Federal Covid spending winds down.

Post war deceleration seems to be on track.

Debt/GDP falling fast as Federal Covid spending winds down.

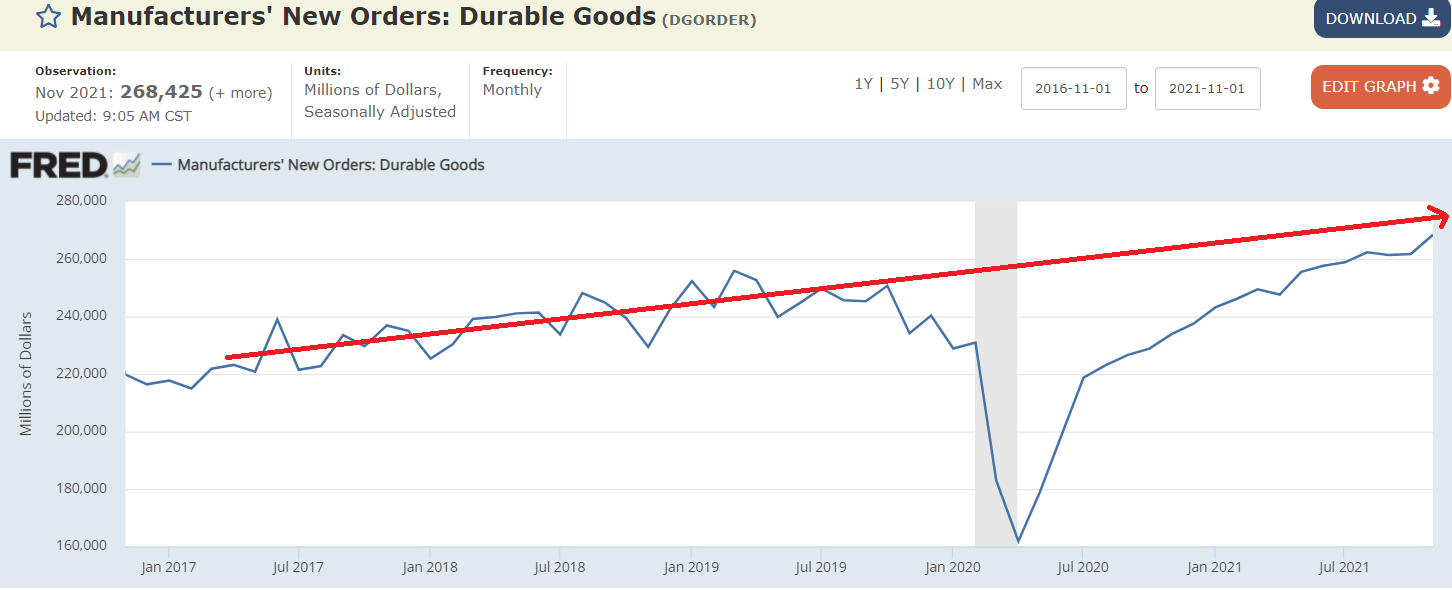

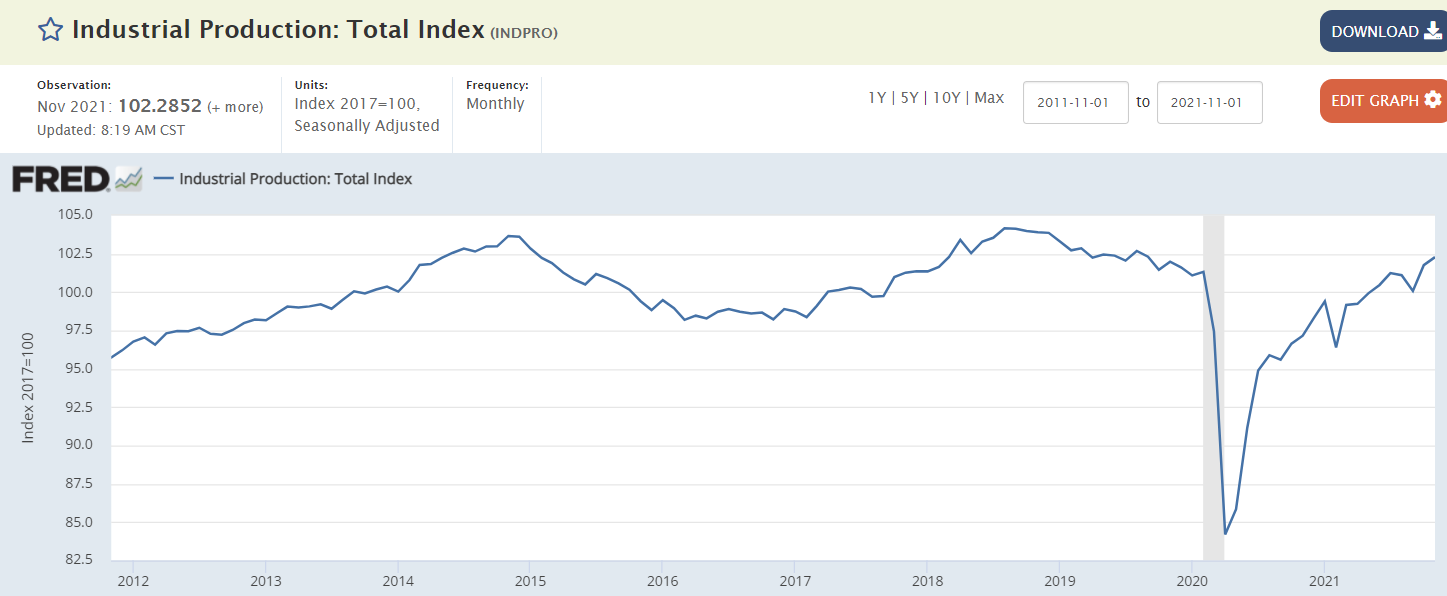

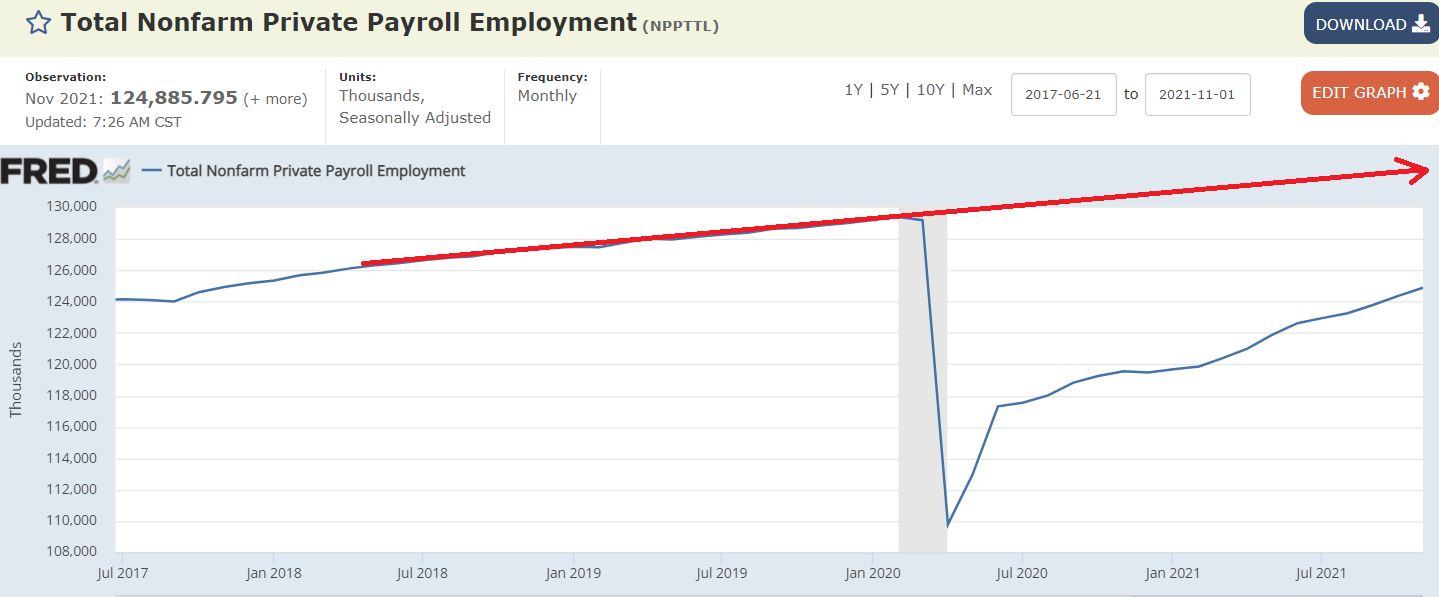

Continues to level off well below the pre covid trend:

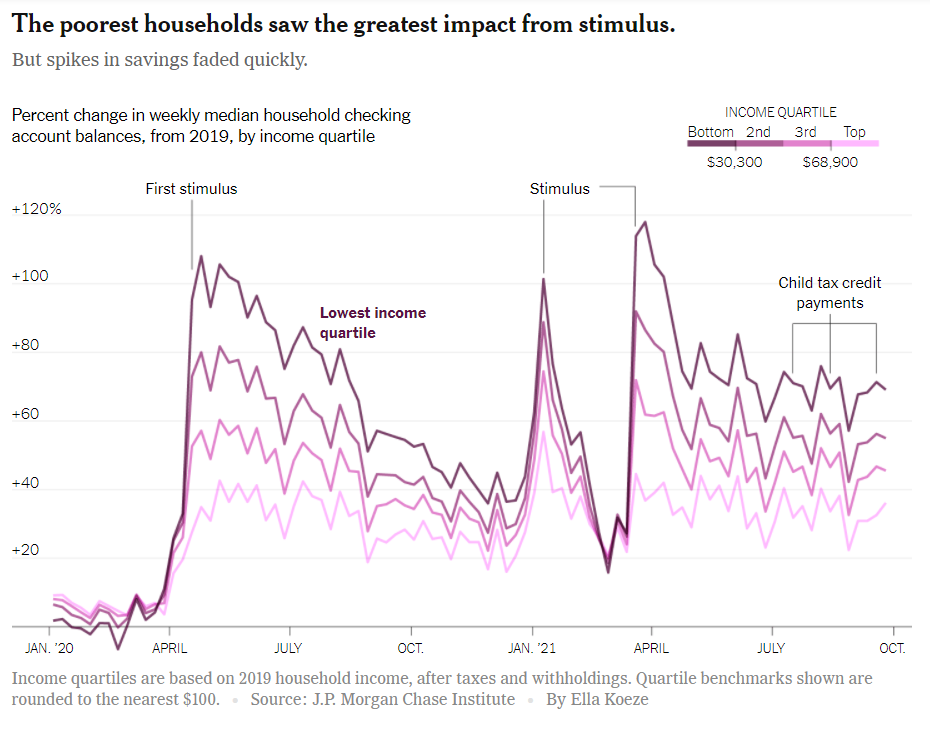

Picking up as Federal transfer payments diminish:

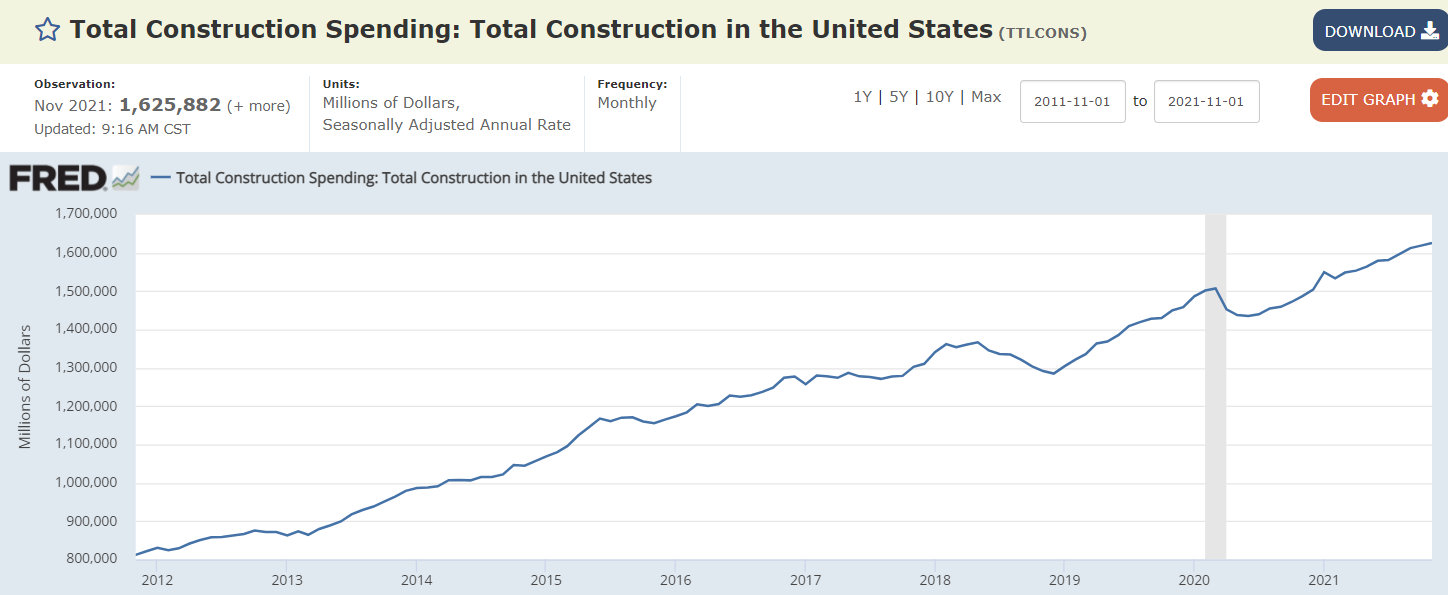

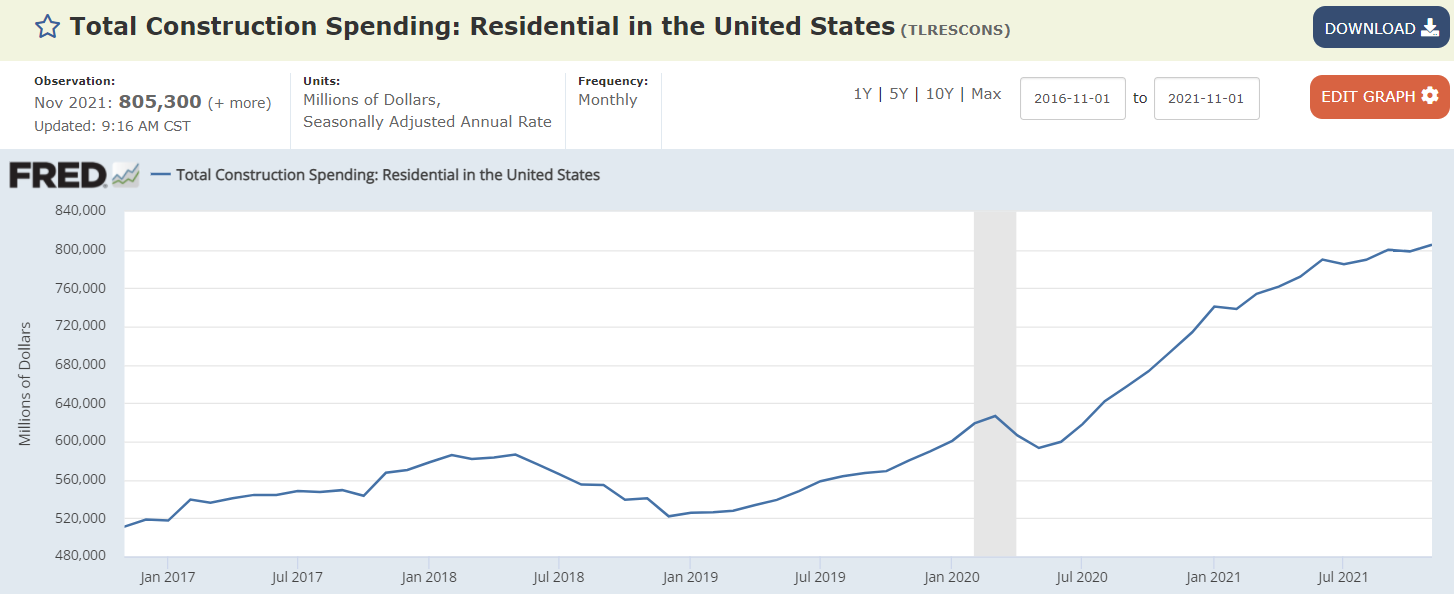

Starting to fade, and this is not adjusted for inflation:

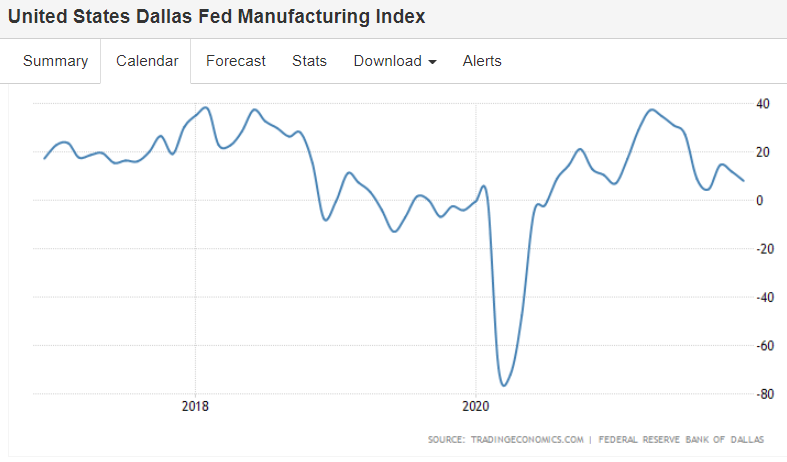

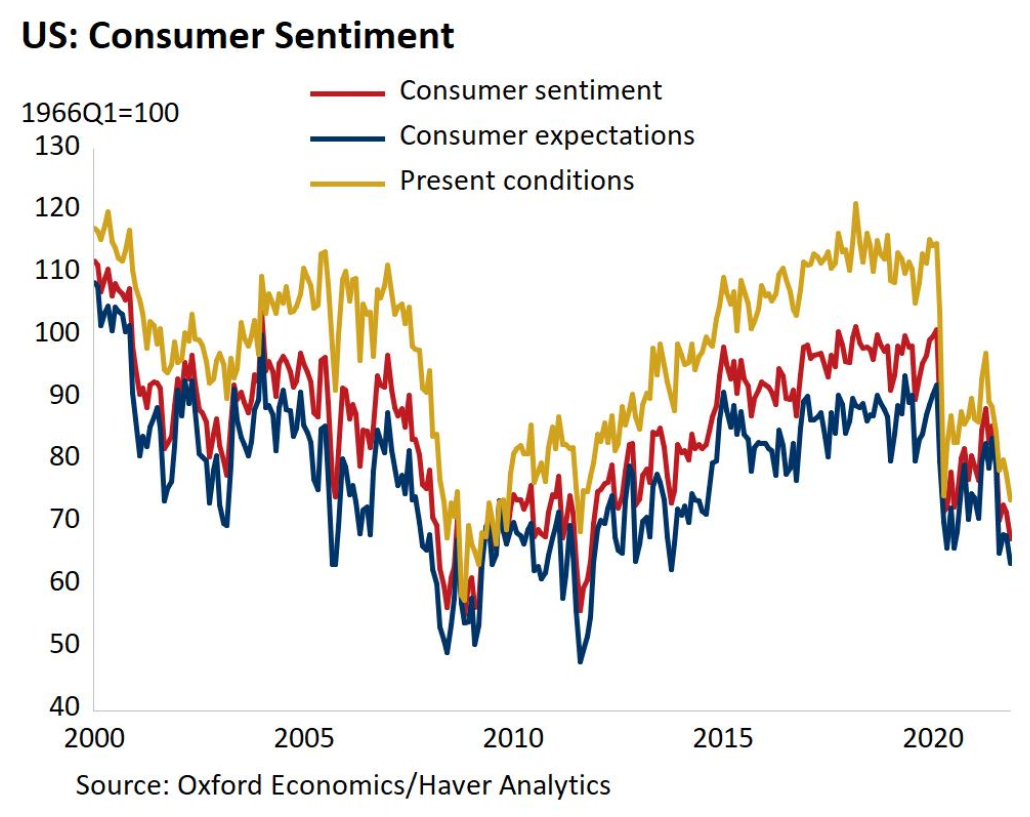

Not sure what to make of this except the post covid bounce seems to be leveling off?

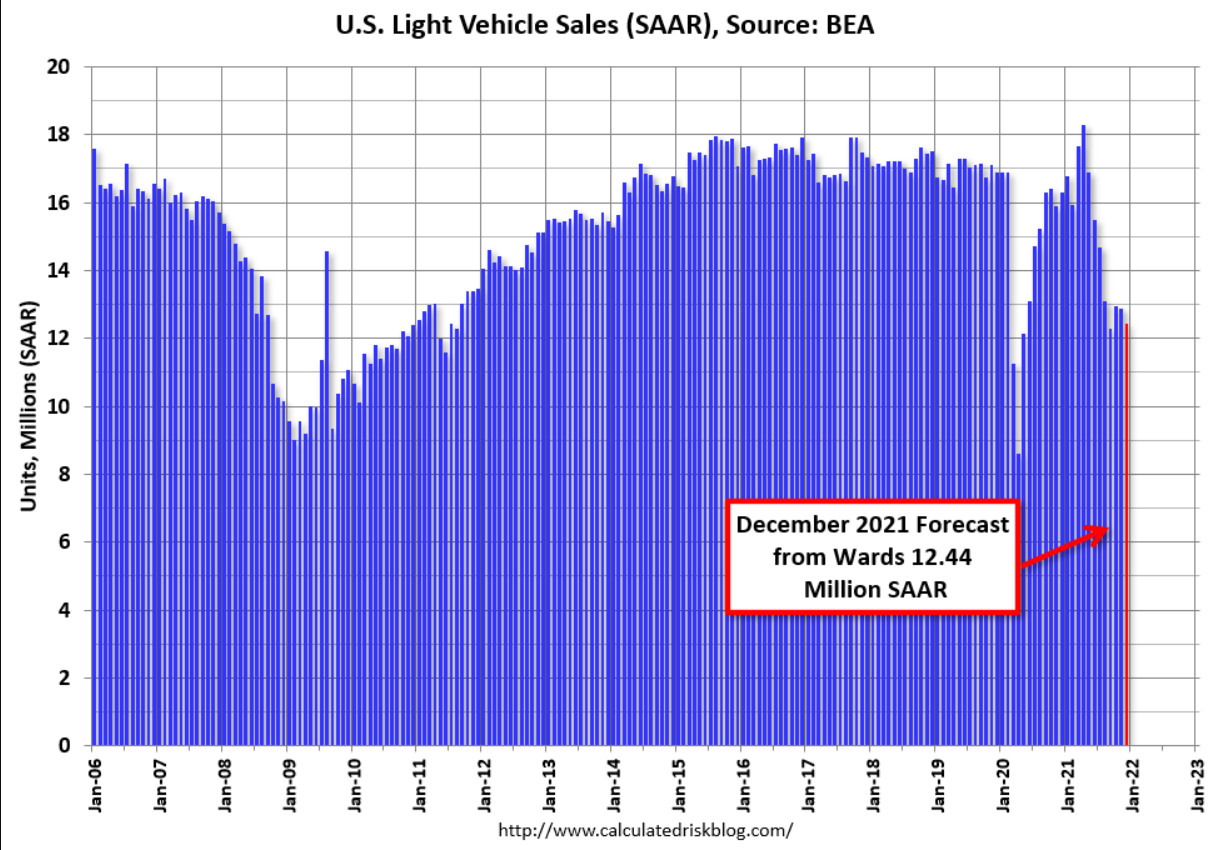

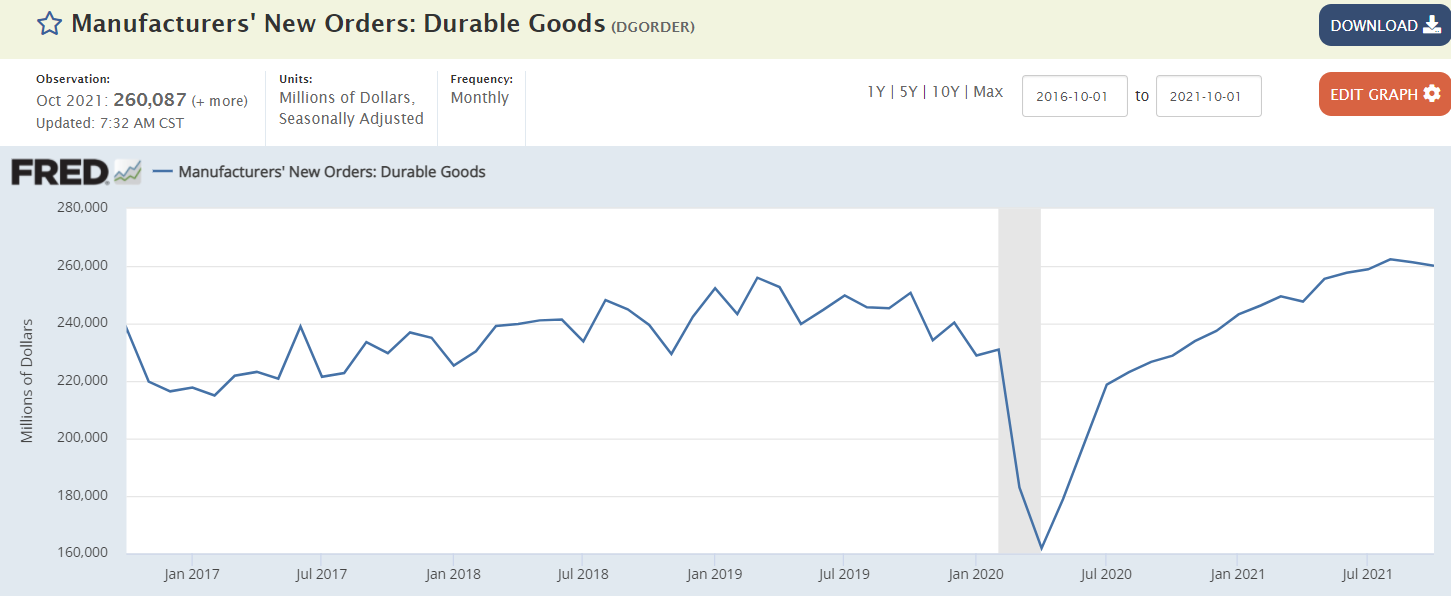

This slowdown is more than just a parts shortage:

This slowdown is more than just a parts shortage:

Working its way lower as are most of the indicators:

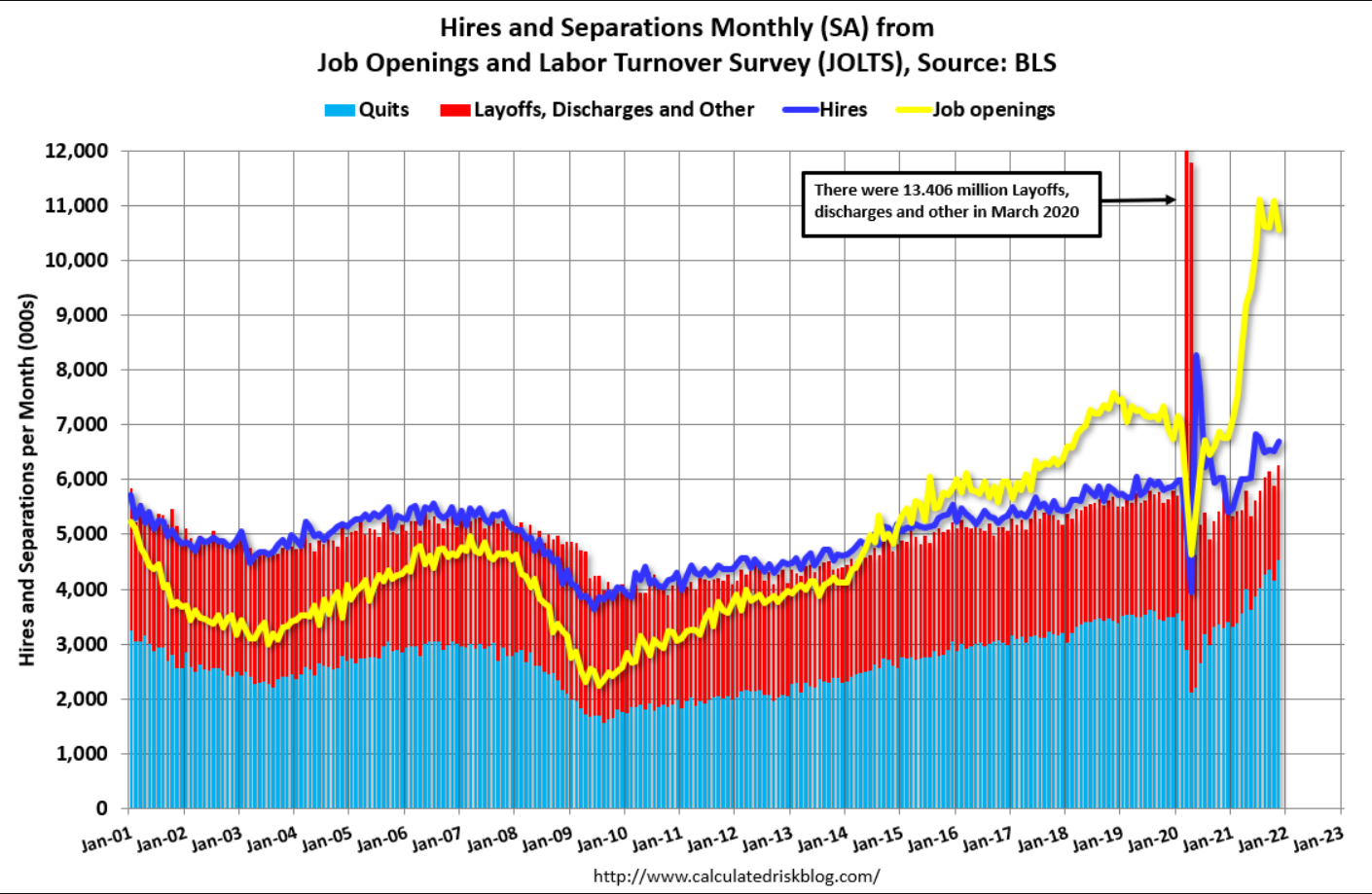

This has helped keep US demand down as fiscal transfers sustained income in the midsts of extensive supply side issues:

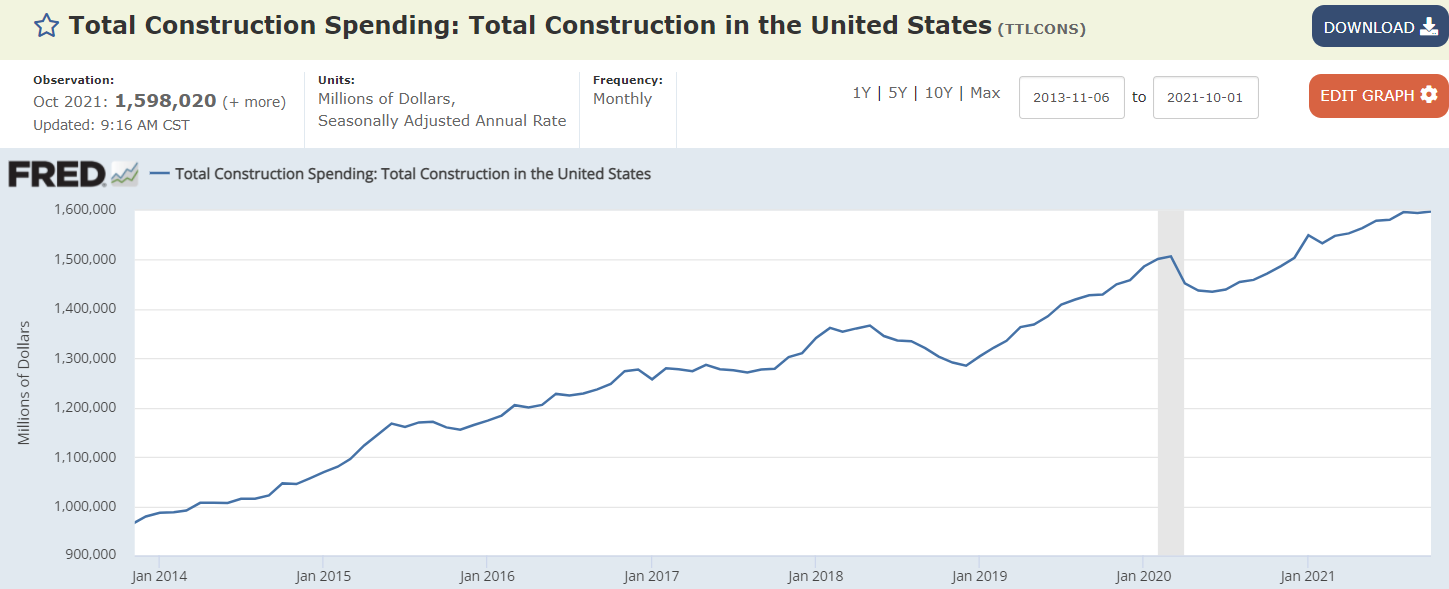

Looks to be leveling off:

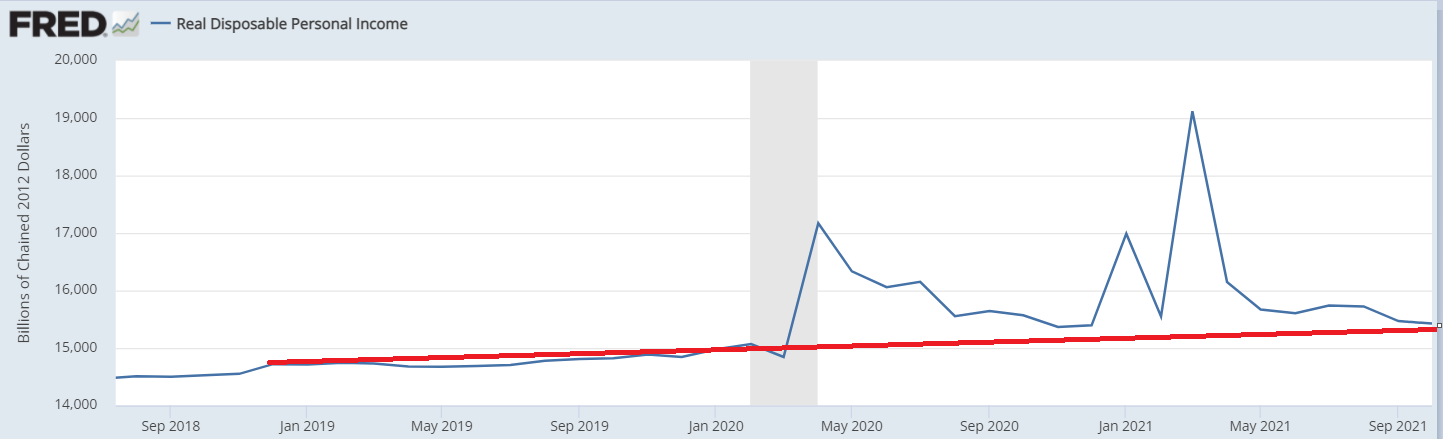

Fallen back to pre covid trend was fiscal transfers expire, with more on the way for Jan:

Back to low growth mode:

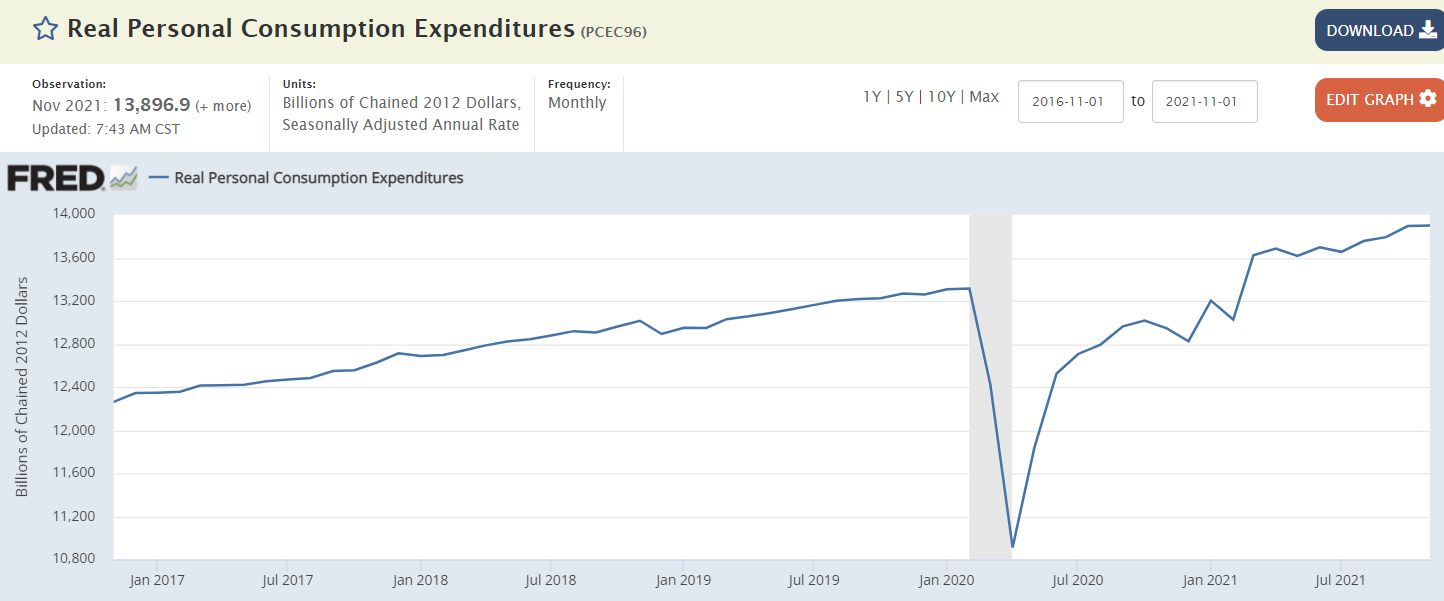

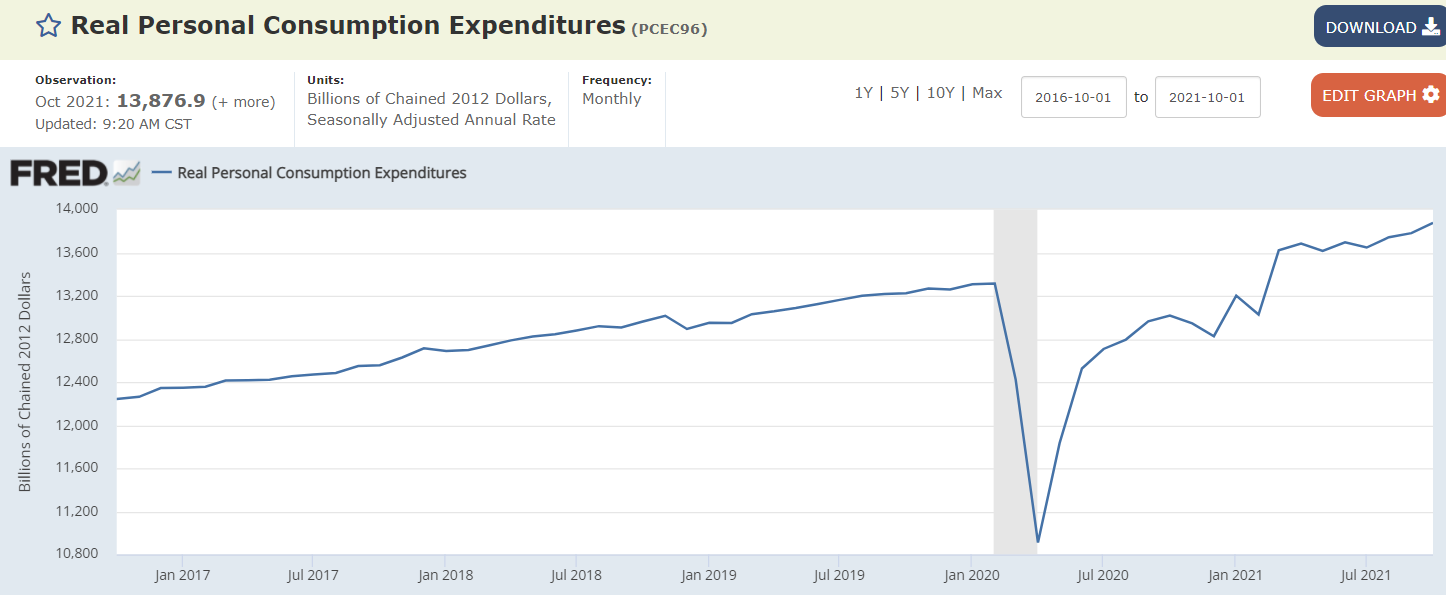

After a nice bounce from the covid dip they seem to be leveling off.

And these numbers aren’t adjusted for ‘inflation:’

Up last month but still look to be going sideways:

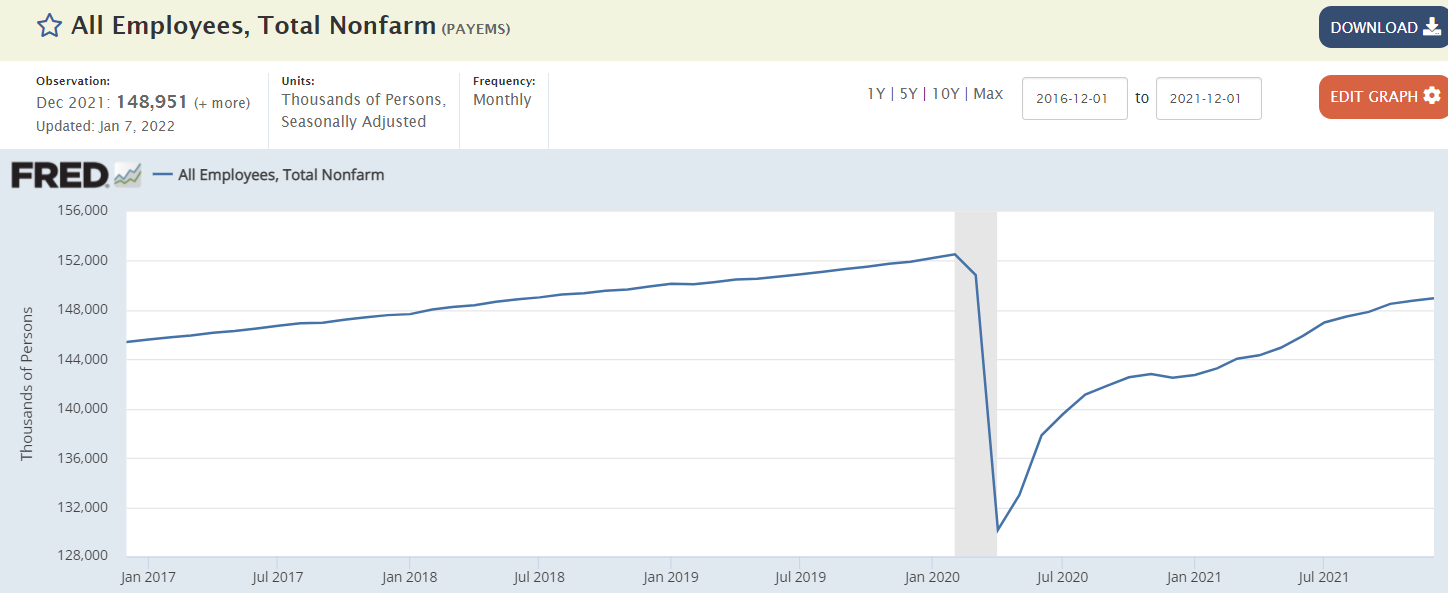

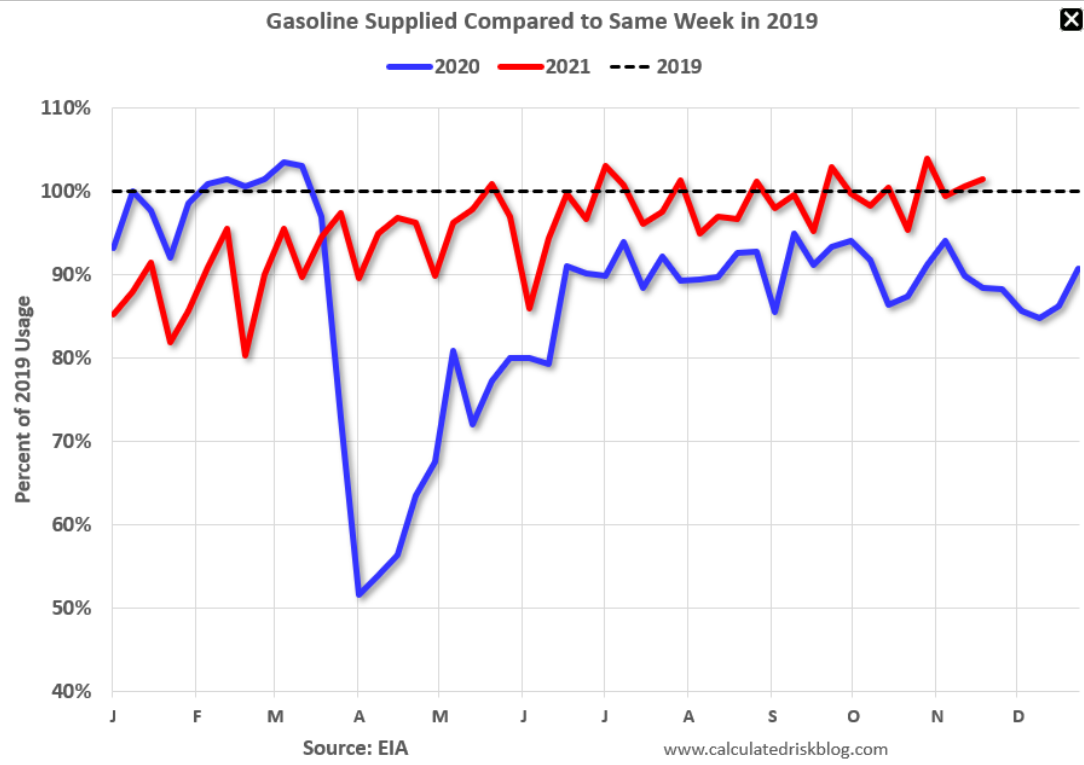

Still slowly recovering to pre covid levels:

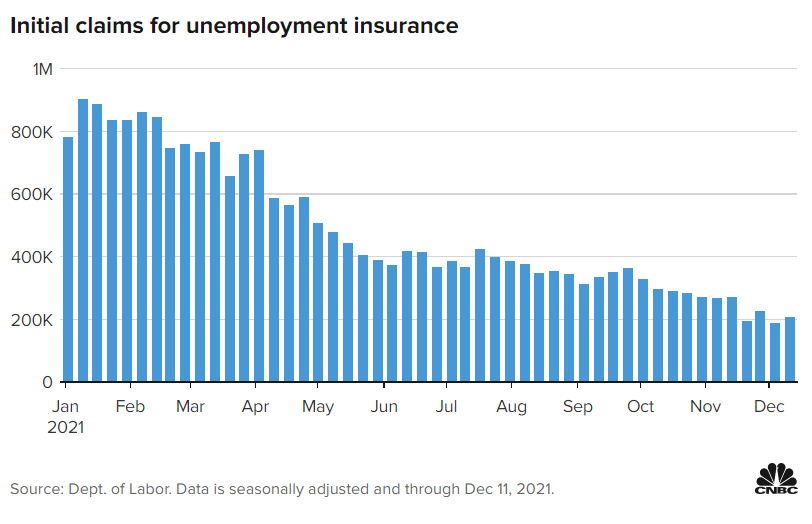

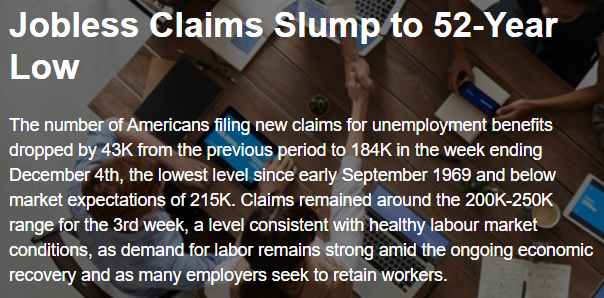

New claims for unemployment comp remain low:

Back to pre covid levels as fewer people are being let go:

Looks to me like the increases will subside if energy prices stabilize:

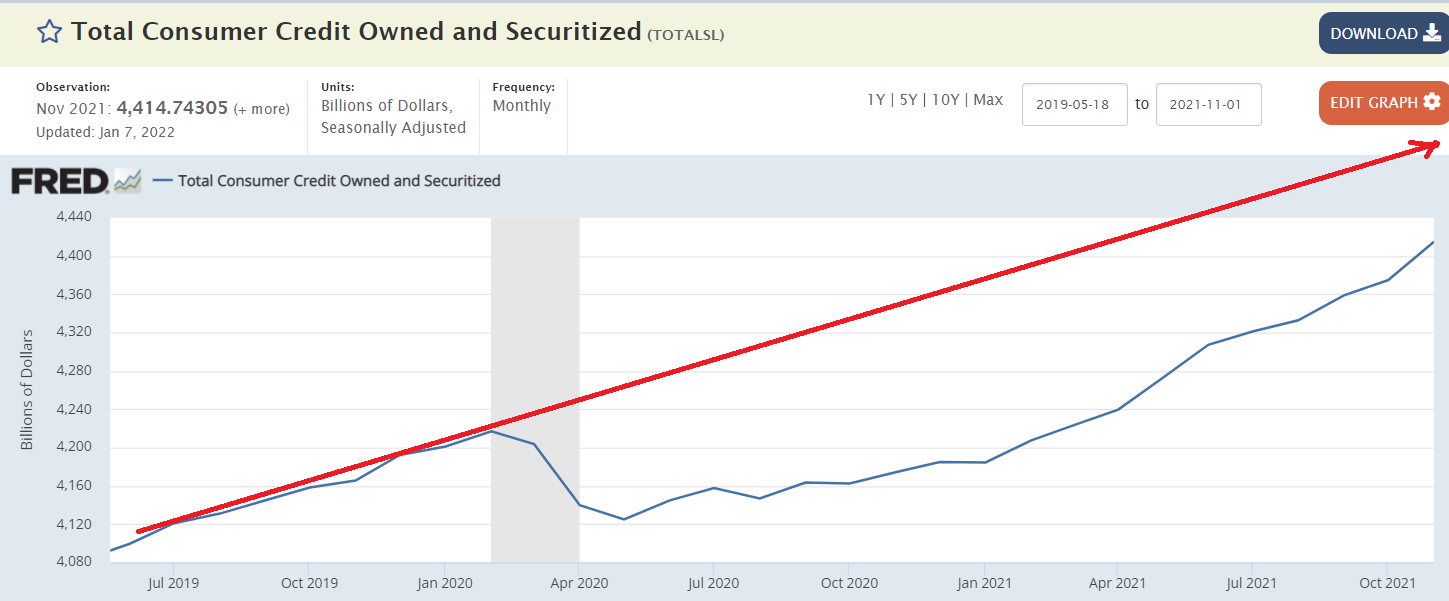

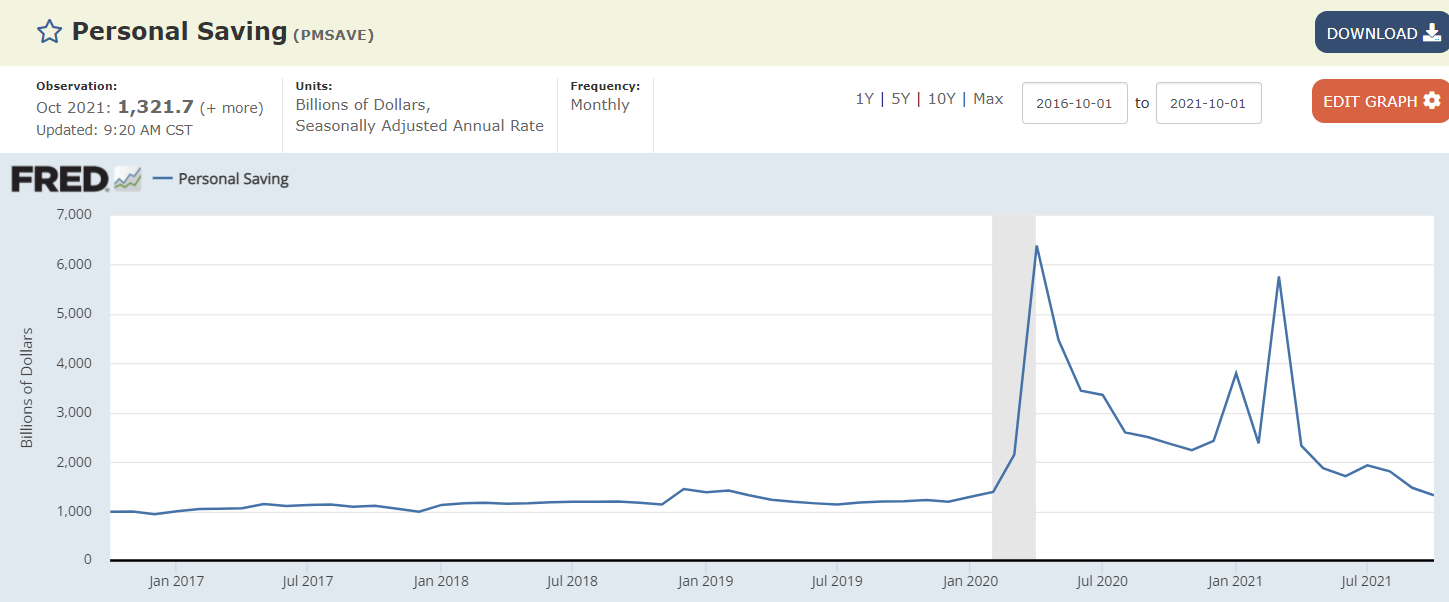

Still looks to be on the decline, as federal deficit spending is quickly fading and inflation reduces the value of savings, causing people and businesses to spend less as they try to sustain a comfortable level of savings:

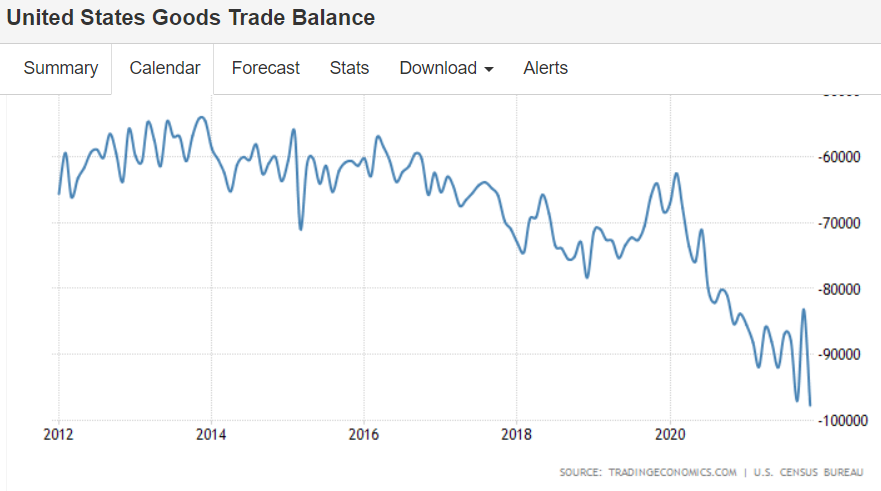

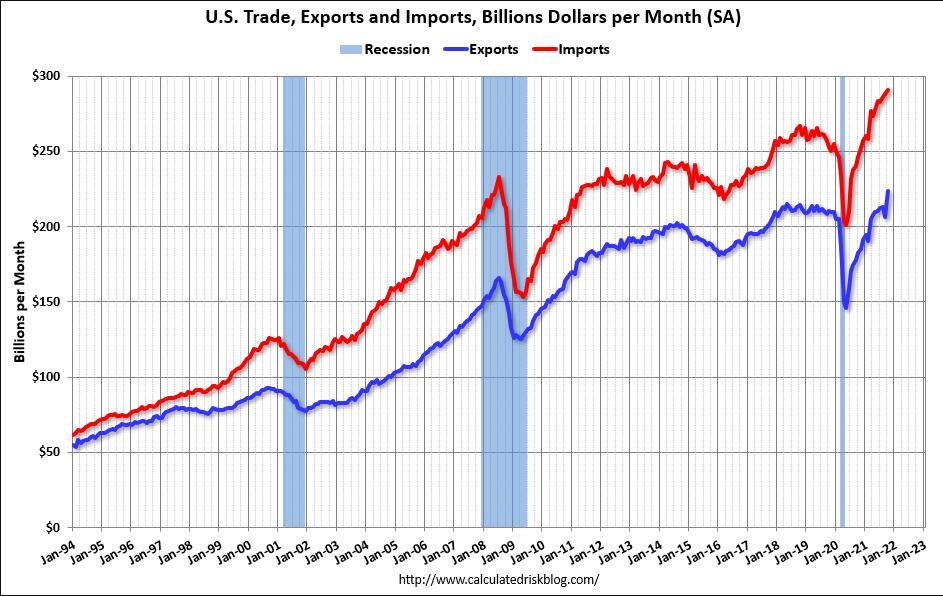

The slowdown in imports could indicate a slowing domestic economy:

Both exports and imports increased in October.

Exports are up 18% compared to October 2020; imports are up 22% compared to October 2020.

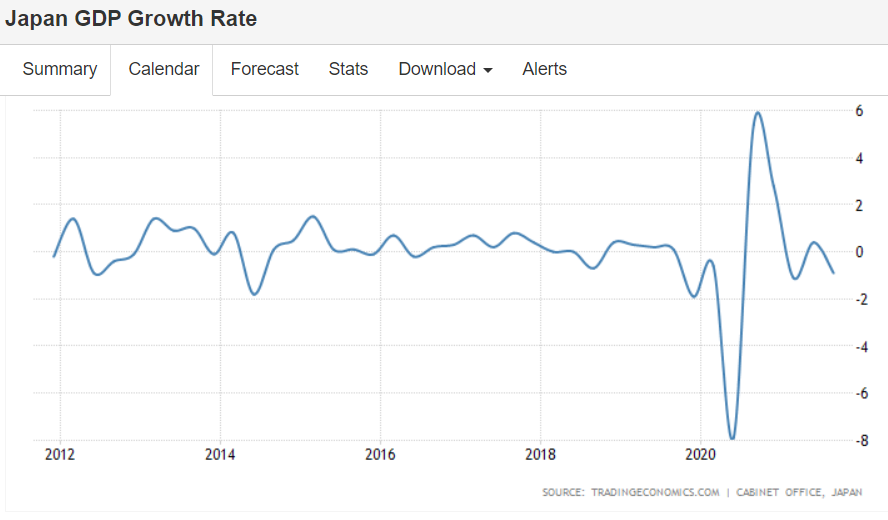

Japan not doing so well:

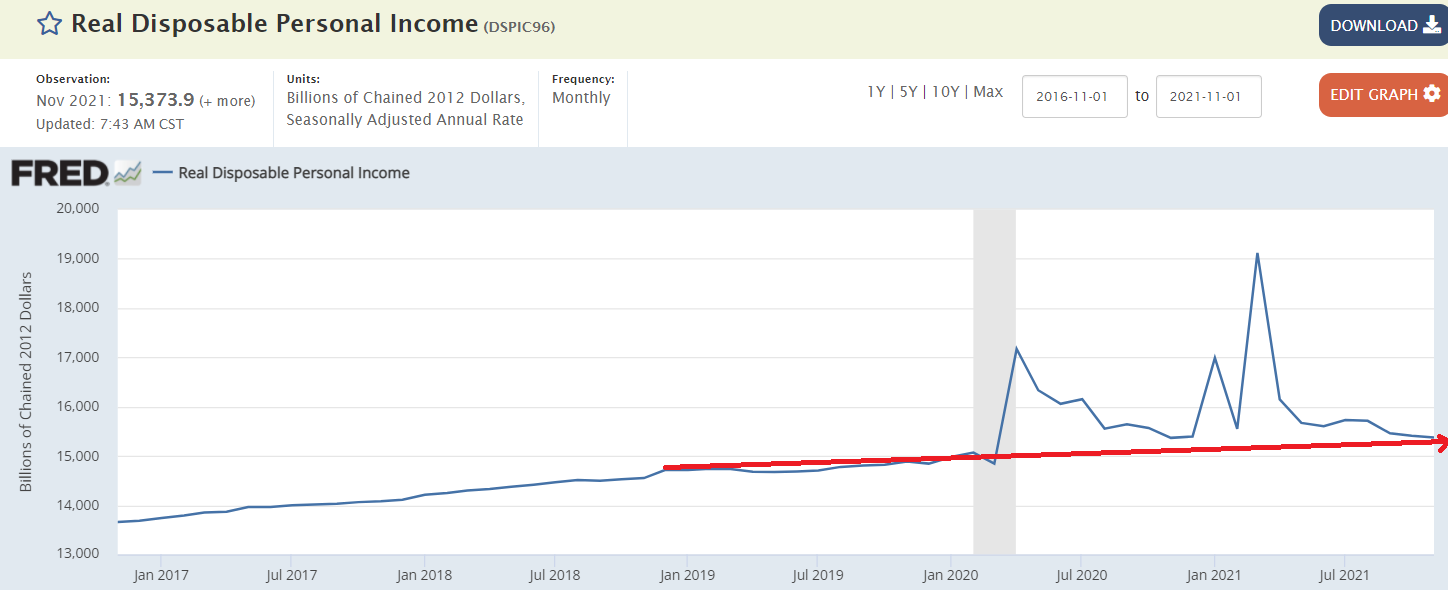

Personal income and savings went up with the fiscal transfers, and now they’re fading:

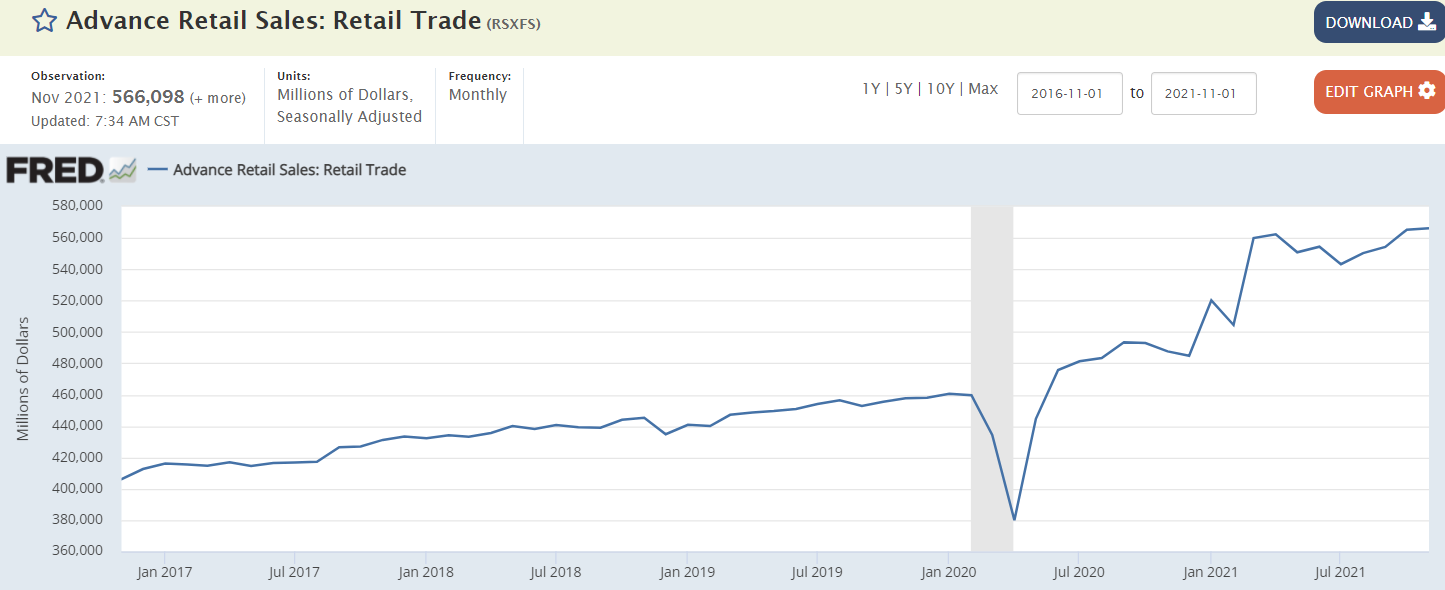

Recovered and then some:

Closing the gap but a ways to go to ketchup:

Not adding much to growth:

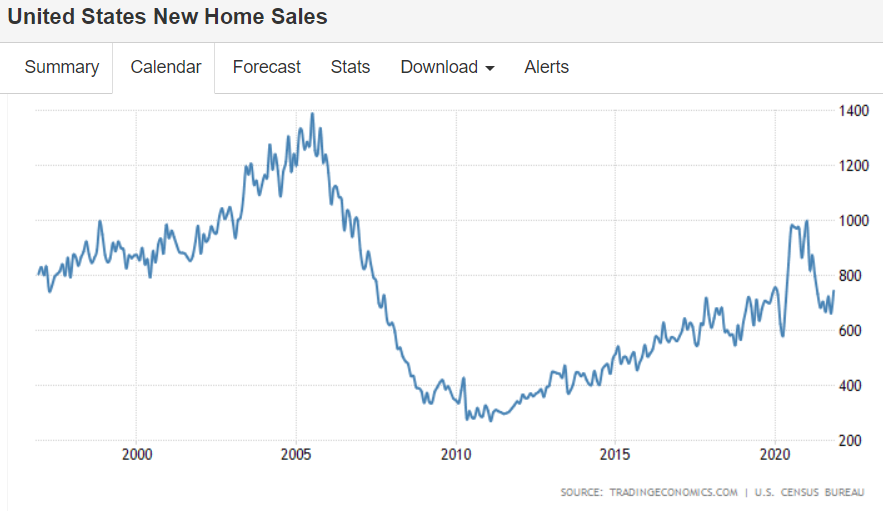

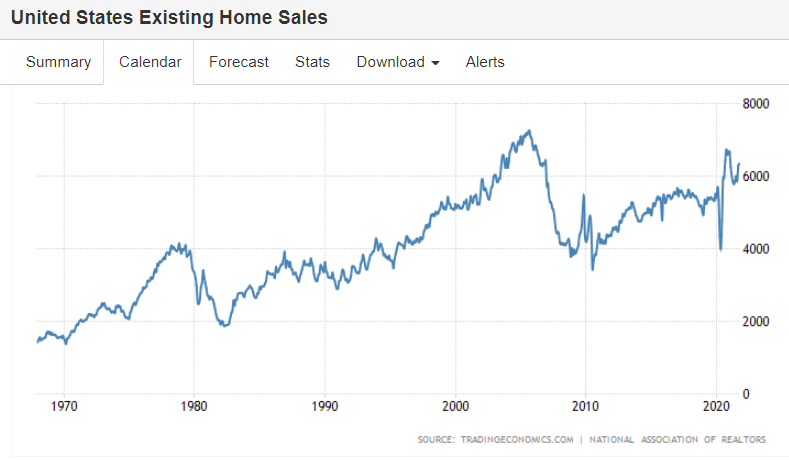

Higher prices brought out a few more sellers:

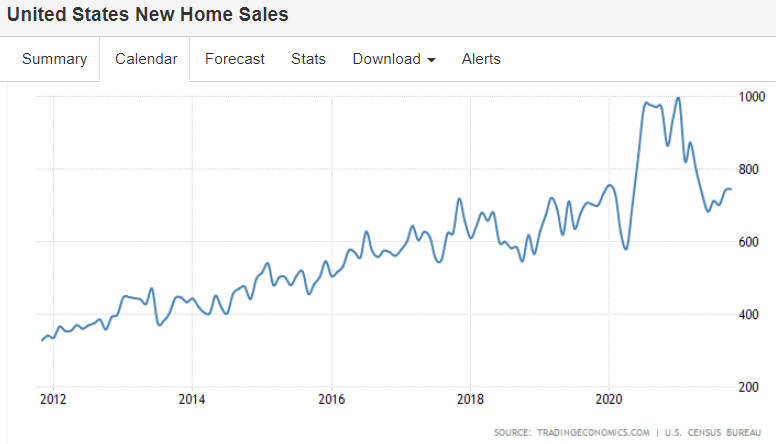

The blip up seems to have reversed:

Softening:

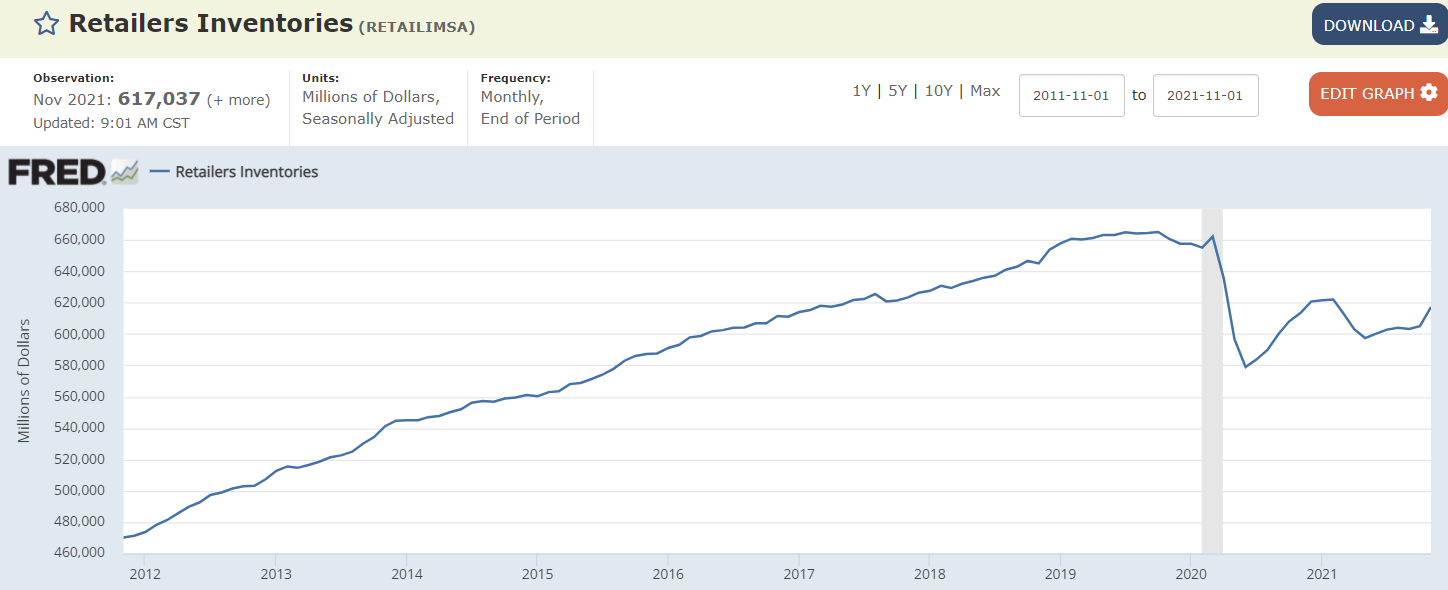

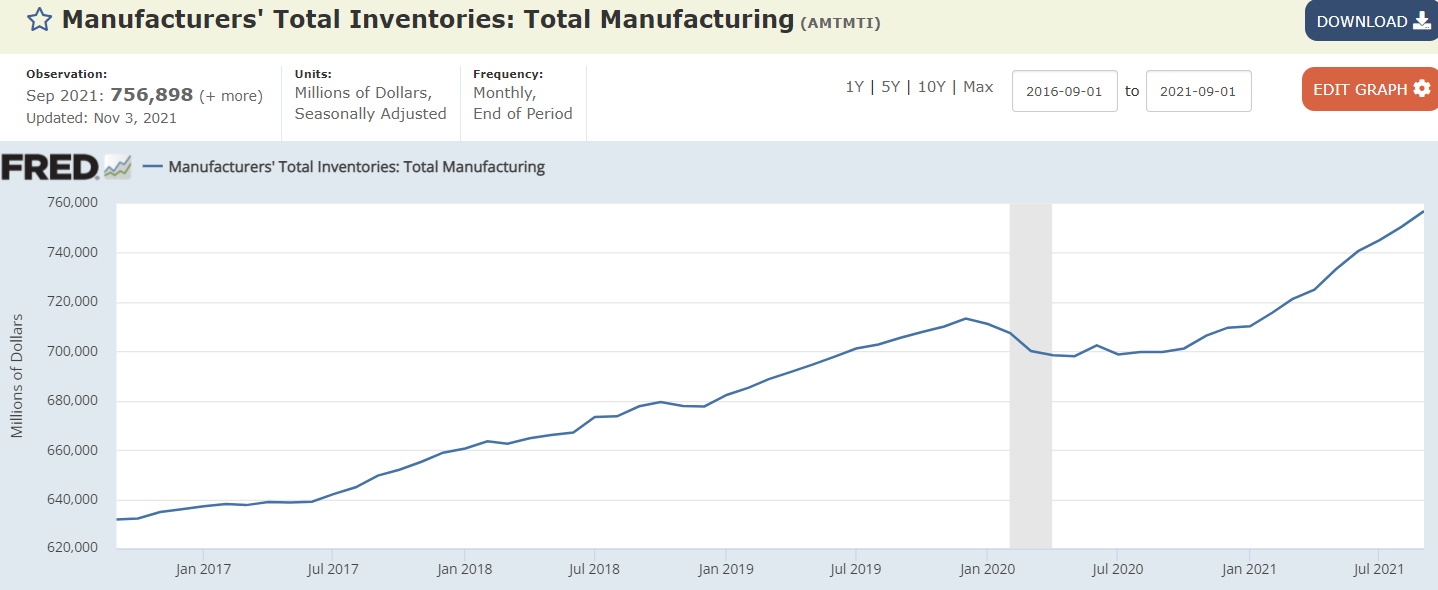

Looks like inventories have recovered:

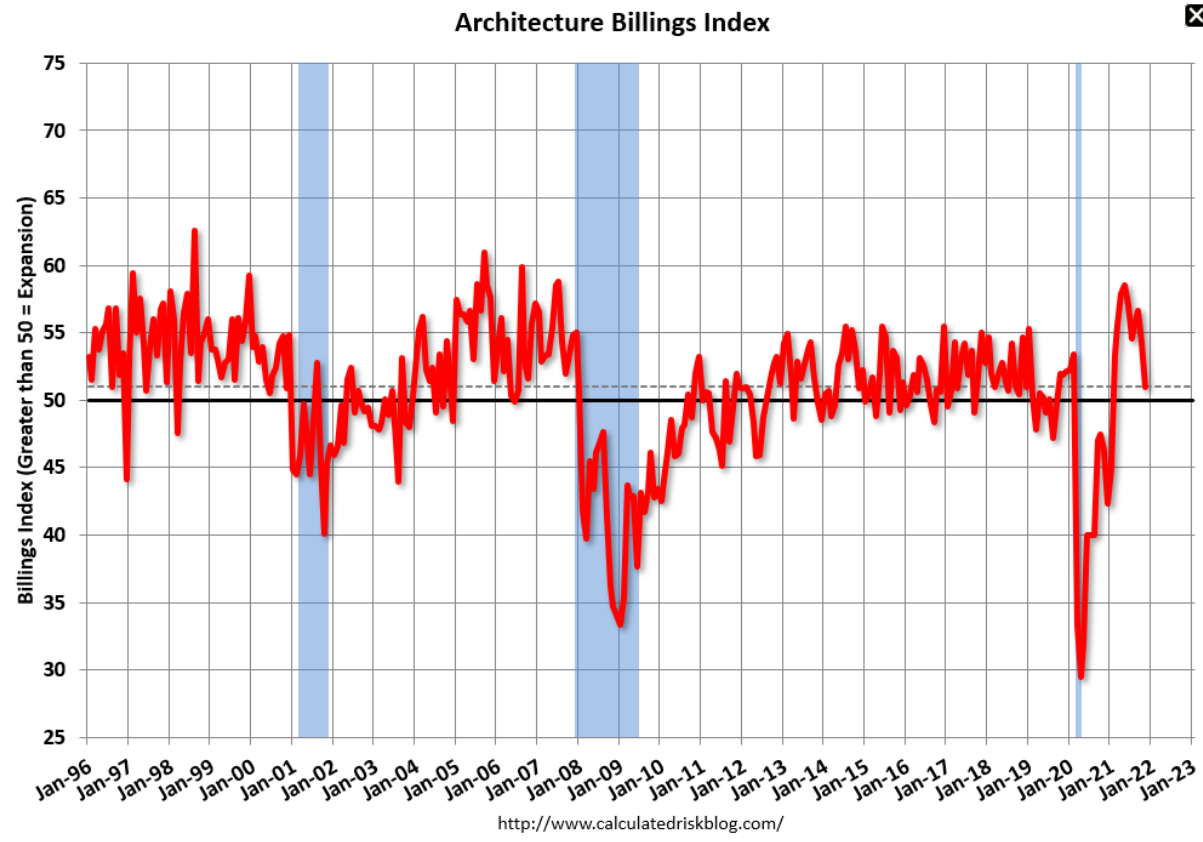

These largely involve buying intentions:

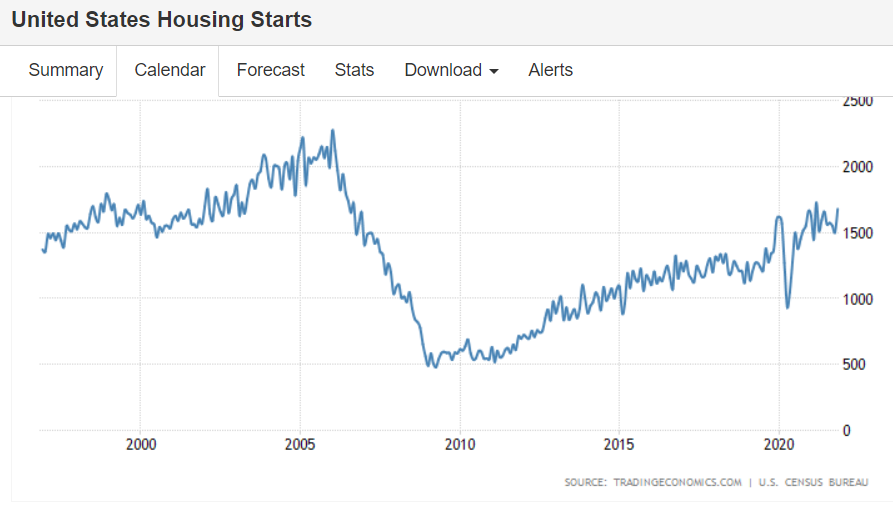

Seems to be back on trend, without have ‘made up for’ the covid dip:

The rate of growth is declining and has about settled back to the pre covid trend.

The higher personal savings from the extra income from fiscal spending is largely

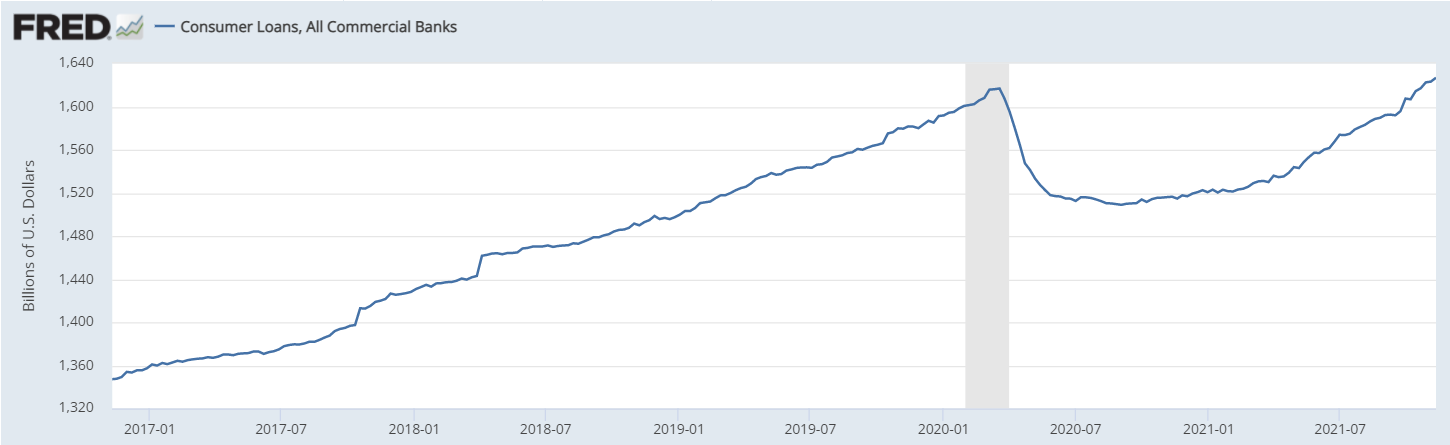

in the form of reduced personal debt:

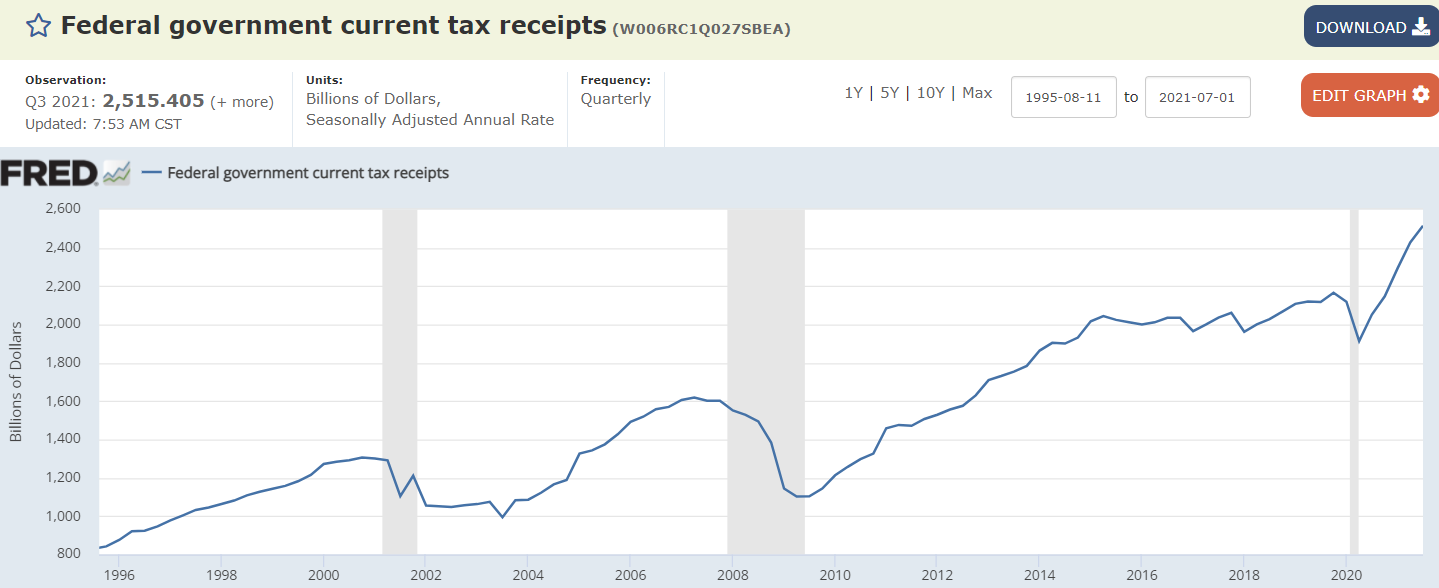

There’s a history of accelerating tax receipts causing recessions: