Up 1.24 M/M.

Whoop de do :(

Full size image

I see no public purpose served by allowing banks to be in the wealth management business?

This is the current thinking, but the pieces don’t add up?

Hoping I’m being too negative here…

Comments below:

US consumers keep spending despite reduced pay

By Christopher S. Rugaber

April 29 (AP) — This year got off to a sour start for U.S. workers: Their pay, already gasping to keep pace with inflation, was suddenly shrunk by a Social Security tax increase.

Which raised a worrisome question: Would consumers stop spending and further slow the economy? Nope. Not yet, anyway.

On Friday, the government said consumers spent 3.2 percent more on an annual basis in the January-March quarter than in the previous quarter the biggest jump in two years. It highlighted a broader improvement in Americans’ financial health that is blunting the impact of the tax increase and raising hopes for more sustainable growth.

Yes, but the ‘slope’ has been negative, with March way down.

Consumers have shed debt. Gasoline has gotten cheaper. Rising home values and record stock prices have restored household wealth to its pre-recession high. And employers are steadily adding jobs, which means more people have money to spend.

Sort of. There have been new jobs, but often at lower pay, and the participation rate has continued to fall. Rising home values are from very low, foreclosure depressed levels, and reports show substantial negative equity remains. And it seems that while total household wealth may be back to the highs, the ‘1%’ has benefited disproportionately.

“No one should write off the consumer simply because of the 2 percentage-point increase in payroll taxes,” says Bernard Baumohl, chief economist at the Economic Outlook Group. “Overall household finances are in the best shape in more than five years.”

Yes, better than 08 after the crash, but still marginal. Debt is down, but take home pay vs the cost of living isn’t doing all that well.

Certainly, spending weakened toward the end of the January-March quarter. Spending at retailers fell in March by 0.4 percent, the worst showing in nine months. And more spending on utilities accounted for up to one-fourth of the increase in consumer spending in the January-March quarter, according to JPMorgan Chase economist Michael Feroli, because of colder weather.

Higher spending on utilities isn’t a barometer of consumer confidence the way spending on household goods, such as new appliances or furniture, would be.

Right. Not good and the slope is negative.

Americans also saved less in the first quarter, lowering the savings rate to 2.6 percent from 3.9 percent in 2012. Economists say that was likely a temporary response to the higher Social Security tax, and most expect the savings rate to rise back to last year’s level. That could limit spending.

‘Saving less’ generally takes the form of ‘borrowing more’, in this case to pay utility bills and make up for the income lost to the tax hike, which is not sustainable.

But several longer-term trends are likely to push in the other direction, economists say, and help sustain consumer spending. Among those trends:

Wealth is up

Home prices rose more than 10 percent in the 12 months that ended in February. And both the Dow Jones industrial average and Standard & Poor’s 500 stock indexes reached record highs in the first quarter. As a result, Americans have recovered the $16 trillion in wealth that was wiped out by the Great Recession.

Again, skewed to the higher income groups who’s ‘consumer spending’ wasn’t all that sensitive to income in any case.

Economists estimate that each dollar of additional wealth adds roughly 3 cents to spending.

Or is it every 3 cents in spending adds a dollar of additional wealth?

That means last year’s $5.5 trillion run-up in wealth could spur about $165 billion in additional consumer spending this year. That’s much more than the $120 billion cost of the higher Social Security taxes.

Or the 120 billion tax hike will reduce wealth by $5.5 trillion from where it would have been otherwise?

‘The wealth’ has to ‘come from’ somewhere. In this case, so sustain spending, non govt debt would have to climb that much more just to make up for the tax hike. It’s possible, but working against that happening is the lower after tax income makes it harder to qualify for new debt, even if you wanted to.

Debt is down

Household debt now equals 102 percent of after-tax income, down from a peak of 126 percent in 2007. That’s almost back to its long-term trend, according to economists at Deutsche Bank.

And so why should it grow faster than the long term trend? The burst last time around was from the sub prime fraud. Before that the .com nonsense and the Y2K scare. Before that the expansion phase of the S&L fraud. And it won’t happen this time if we’re careful to not allow a credit expansion we’ll later regret…

And households are paying less interest on their debts, largely because of the Federal Reserve’s efforts to keep borrowing rates at record lows.

And earning less on their savings. Households are net savers.

The percentage of after-tax income that Americans spent on interest and debt payments dropped to 10.4 percent in the October-December quarter last year. That’s the lowest such figure in the 32 years that the Federal Reserve has tracked the data.

And personal income from interest has likewise dropped, and probably more so.

Jobs are up

Employers have added an average of 188,000 jobs a month in the past six months, up from 130,000 in the previous six. Job gains slowed in March to only 88,000.

Yes, negative slope again. And not even beginning to close the output gap.

But most economists expect at least a modest rebound in coming months. And layoffs sank to a record low in January. Fewer layoffs tend to make people feel more secure in their jobs and more willing to spend.

Gas prices are down

Gasoline prices have fallen in the past year and are likely to stay low. Nationwide, the average price of a gallon of gas has dropped 28 cents since this year’s peak of $3.79 on Feb. 27. Analysts expect gas to drop an additional 20 cents over the next two months. Each 10 cent drop over a full year translates into roughly $13 billion in savings for consumers.

Yes, that helps, except gas prices have been going back up most recently.

Loan costs are down

Lower interest rates have enabled millions of Americans to save money by refinancing their mortgages. Mortgage giant Freddie Mac estimates that in the fourth quarter of 2012, homeowners who refinanced cut their interest rate by one-third, the biggest reduction in 27 years the agency has tracked the data. On a $200,000 loan, that means $3,600 in savings over the next 12 months.

And savers are losing that much.

Some economists note that the Social Security tax cut didn’t spur much more spending when it first took effect at the start of 2011. The tax cut gave someone earning $50,000 about $1,000 more to spend each year. A household with two high-paid workers had up to $4,500 more.

Despite the tax cut, Baumohl notes that consumer spending rose only 2.5 percent in 2011 and 1.9 percent in 2012. In the 10 years before the recession began in December 2007, the average annual spending increase was 3.4 percent.

And a study by the Federal Reserve Bank of New York found that consumers spent only 36 percent of the increased income that resulted from the tax cut. The rest went to paying down debt or to savings.

Ok, so the question is whether with the tax hike they will cut spending or consume from borrowing and dipping into savings. Initially that’s what happened, but seems by March the increasing consumption had started to fade?

And the sequesters hadn’t even begun.

Since the tax cut didn’t boost spending that much, its expiration may not drag it down much, either. Economists say temporary tax cuts are often ineffective because many consumers assume that the tax breaks will eventually disappear. So they don’t ramp up spending in response.

As just discussed. It’s not necessarily symmetrical.

Scott Loehrke, 25, hasn’t cut back spending this year. Loehrke went ahead in March with some car repairs that could have been delayed. And he still plans to vacation in May in Mexico with his wife, Jackie.

The couple, who live just outside Cleveland, feel secure in their jobs. Loehrke is a salesman for a company that makes T-shirts, cups, key chains and other promotional products. Business has picked up in the past year as the economy has improved. His wife is a pharmacist.

“Everything that we’ve planned to do we’re still doing,” Loehrke says.

That proves their case!!!

:(

The Loehrkes both have heavy student debt and so are focused on keeping their expenses in check. They both drive used cars. That’s enabled them to build up some savings and made it easier to absorb the tax increase.

New threats have emerged. Across-the-board government spending cuts kicked in March 1. The spending cuts have triggered government furloughs and could lead private companies that do business with the government to cut staff. And the cuts are expected to shave a half-point from economic growth this year.

And that’s just the first order effect.

Even so, most economists are relieved that consumers have proved so resilient so far.

“It’s very encouraging that consumers and thus the broader economy have been able to weather that storm as well as they have,” says Mark Zandi, an economist at Moody’s Analytics.

‘The beatings will continue until morale improves’

This is my overall view of the economy.

The US was on the move by Q4 last year. A housing and cars (and student loans) driven expansion was happening, with slowing transfer payments and rising tax revenues bringing the deficit down as the automatic stabilizers were doing their countercyclical thing that would eventually reverse the growth. But that could take years. Look at it this way. Someone making 50,000 per year borrowed 150,000 to buy a house. The loan created the deposit that paid for the house. The seller of the house got that much new income, with a bit going to pay taxes and the rest there to be spent. Maybe a bit of furniture etc. was bought on credit as well, again adding income and (gross) financial assets to the recipients of the borrowers spending. And increasing sales added employment as well as output, albeit not enough to keep up with population growth etc.

I was very hopeful. Back in November, after the ‘Obama is a socialist’ sell off, I wrote that it was time to buy stocks and go play golf for three years, as, left alone, the credit accelerator in progress could go on for a long time.

But it wasn’t left along. Only a few weeks later the cliff drama began to intensify, with lots of fear of going over the ‘full cliff’. While that didn’t happen, we did go over about 1/3 cliff when both sides let the FICA reduction expire, thus removing some $170 billion from 2013, along with strong prospects of an $85 billion (annualized) sequester at quarter end. This moved me ‘to the sidelines’. Seemed to me taking that many dollars out of the economy was a serious enough negative for me to get out of the way.

But the Jan and then Feb numbers showed I was wrong, and that the consumer had continued to grow his spending as before via housing and cars, etc. Even the cliff constrained -.1 GDP of Q4 was soon revised up to .4. Stocks kept moving up and bonds moved higher in yield, even as the sequester kicked in, with the market view being the FICA hike fears were bogus and same for the sequester fears. Balancing the budget and getting the govt out of the way does indeed work to support the private sector. The UK, Eurozone, and Japan were exceptions. Austerity inherently does work. And markets were discounting all that, as it’s what market participants believed and the data supported.

Then, it all changed. April releases of March numbers showed not only suddenly weak March numbers, but Jan and Feb numbers revised lower as well. The slope of things post FICA hike went from positive to negative all at once. The FICA hike did seem to have an effect after all. And with the sequesters kicking in April 1, the prospects for Q2 were/are looking worse by the day.

My fear is that the FICA hikes and sequesters didn’t just take 1.5% of GDP ‘off the top’ as forecasters suggest, leaving future gains from the domestic credit expansion there to add to GDP as they had been. That is, the mainstream forecasts are saying when someone’s paycheck goes down by $100 per month from the FICA hike, or loses his job from the sequester, he slows his spending, but he still borrows to buy a car and/or a house as if nothing bad had happened, and so GDP is reduced by approximately the amount of the tax hikes and spending cuts, with a bit of adjustment for the ‘savings multipliers’. I say he may not borrow to buy the house or the car. Which both removes general spending and also slows the credit accelerator, shifting the always pro cyclical private sector from forward to reverse. And the ‘new’ negative data slopes have me concerned it’s already happening. Before the sequesters kicked in.

Looking at Japan, theory and evidence tells me the lesson is that lower interest rates require higher govt deficits for the same level of output and employment. More specifically, it looks to me like 0 rates may require 7-8% or even higher deficits for desired levels of output and employment vs maybe 3-4% deficits when the central bank sets rates at maybe 5% or so, etc. And US history could now be telling much the same.

And another lesson from Japan we should have learned long ago is that QE is a tax that does nothing good for output or employment and is, if anything, ‘deflationary’ via the same interest income channels we have here. Note that the $90 billion of profits the Fed turned over to the tsy would have been earned in the economy if the Fed hadn’t purchased any securities. So, as always in the past, watch for Japan’s QE to again ‘fail’ to add to output, employment, or inflation. However, their increased deficit spending, if and when it materialize, will support output, employment, and prices as it’s done in the past.

Oil and gasoline prices are down some, which is dollar friendly and consumer friendly, but only back to sort of ‘neutral’ levels from elevated ‘problematic’ levels And there is risk that the Saudis decide to cut price for long enough to put the kibosh on the likes of North Dakota’s and other higher priced crude, wiping out the value of that investment and ending the output and employment and currency support from those sources. No way to tell what they may be up to.

So my overall view is negative, with serious deflationary risks looming.

And the solution is still fiscal- a tax cut and/or spending increase.

However, that seems further away then ever, as the President is now moving towards an additional 1.8 trillion of deficit reduction.

:(

Seems like this ‘quasi’ govt type of thing is often later shown to be behind ‘difficult to explain’ ‘liquidity driven’ equity moves.

Norway oil fund makes big move from bonds to stocks

By Richard Milne in Oslo

April 29 (FT) — Norway’s oil fund has reduced its bond holdings to their lowest ever level as the worlds largest sovereign wealth fund signals its discomfort with the effects of western central banks money printing.

The fund held just 36.7 per cent of its $726bn assets in bonds at the end of the first quarter, the lowest proportion since it first received money in 1996. Its equity holdings were close to a record high, accounting for 62.4 per cent of the total.

Yngve Slyngstad, the funds chief executive, told the Financial Times there had been a significant change in rhetoric away from its previous comments that it was comfortable with a high level of equity holdings.

Now it is that we are not so comfortable with the low returns in the bond portfolio. It is not enthusiasm for the equity market but a lack of enthusiasm for the bond market, he said.

The worlds biggest sovereign wealth fund by some distance, Norways oil fund has for some time been concerned about the low level of government bond yields and what that will mean for fixed income return.

But Norges Bank Investment Management, as it is also known, is reluctant to comment about money printing, known as quantitative easing, by the US Federal Reserve, Bank of England or Bank of Japan as the fund is part of the Norwegian central bank.

Still, Mr Slyngstad said unconventional actions were riskier than normal measures, signalling his unease. Unconventional in this context means untried. Things that are untried have a different risk profile than things that have been tried, he added.

The fund has been shifting both its bond and equity holdings away from dollar, yen, euro and sterling assets to those of emerging markets . But the fund is noticeably more positive on US Treasuries than other western government bonds with Mr Slyngstad saying they serve [a] double purpose of being a haven and highly liquid.

Mr Slyngstad said the fund could take several courses of action to reduce the risk of a sharp fall in bond prices, including buying real assets such as property and diversifying into new currencies. It has also reduced the average duration of its bond holdings from about six to five years.

His comments came as the fund delivered its biggest ever quarterly increase in its market value of NKr366bn. It posted a 5.4 per cent overall return with equities gaining 8.3 per cent and fixed income just 1.1 per cent. Apple, Santander and BHP Billiton were its worst-performing investments while BlackRock, Nestl and Novartis were the best. The oil fund also formally unveiled its plans to become a more active investor , as first revealed by the Financial Times. Mr Slyngstad has joined the nomination committee of Swedish truckmaker Volvo , the first time the fund has formally participated in the selection of board directors.

This plays to investors who think a drop in govt spending is good for the private sector as it ‘gets govt out of the way’ and ‘opens the door’ for that much more private sector growth in short order.

While this could be sort of but not necessarily true at full employment, it is of course not true in any case with with today’s excess capacity.

Seems they forget that today, cuts in govt spending immediately translate into cuts in private sector sales, which are the driver of private sector output and employment.

Yes, private sector credit expansion has (had?) begun to ‘kick in’, somewhat more than replacing the decline in govt deficit spending from the ‘automatic fiscal stabilizers’ of slowing transfer payments and rising revenues from higher incomes. The causation was from more ‘borrowing to spend’ in the economy to less deficit spending.

And that all can accelerate and continue for many years before, left alone, the deficit gets too small (and shrinking) to support the growing private sector credit expansion, as it all becomes unsustainable and implodes.

But at any point during that credit expansion, a pro active dose of govt deficit reduction can remove sufficient income to restrict the private sector’s credit expansion. People who may have borrowed to buy a house or a car, for example, suddenly losing their jobs and those purchases not happening, etc.

So the idea that 3% GDP is a ‘given’ due to private sector credit expansion and therefore a proactive tax hike and spending cut of maybe 1.25% of GDP will lower that to 1.75% growth misses that dynamic, as it presumes the proactive fiscal adjustments don’t throw a monkey wrench into the credit expansion dynamics. Like what’s been happening in the euro zone.

—– Original Message —–

At: Apr 26 2013 07:39:34

The miss was mostly a result of government declining, again. This is really the surprise. Trade was also a drag, but from a surprise perspective government is the winner. In all, gov subtracted a chunky 0.8ppts from the topline – meaning if you add it back Q1 would have printed 3.3%.

Having said that, this a rearview mirror report and what we already know about the handoff to Q2 is that it was weak. Indeed, we are looking for a rather paltry 1% outcome here in Q2.

Finally, in terms of today’s report, no underlying detail is inconsistent with our thinking about the handoff to Q2.

Rolling over from ever lower cyclical levels???

Higher than first reported, but still not looking at all good. Particularly compared to previous cycles.

The intellectual dishonesty continues.

As before, it’s the lie of omission.

R and R are familiar with my book ‘The 7 Deadly Innocent Frauds of Economic Policy’ and, when pressed, agree with the dynamics.

They know there is a more than material difference between floating and fixed exchange rate regimes that they continue to exclude from their analysis.

They know that one agents ‘deficit’ is another’s ‘surplus’ to the penny, a critical understanding they continue to exclude.

They know that ‘demand leakages’ mean some other agent must spend more than its income to sustain output and employment.

They know federal spending is via the Fed crediting a member bank reserve account, a process that is not operationally constrained by revenues. That is, there is no dollar solvency issue for the US government.

They know that ‘debt management’, operationally, is a matter of the Fed simply debiting and crediting securities accounts and reserve accounts, both at the Fed.

They know that if there is no problem of excess demand, there is no ‘deficit problem’ regardless of the magnitudes, short term or long term.

They know unemployment is the evidence deficit spending is too low and a tax cut and/or spending increase is in order, and that a fiscal adjustment will restore output and employment, regardless of the magnitude of deficits or debt.

Carmen’s husband Vince was the head of monetary affairs at the Fed for many years, serving both Alan Greenspan and Ben Bernanke. He knows implicitly how the accounts clear and how the accounting works, to the penny. He knows the currency itself is a case of monopoly. He knows the Fed, not ‘the market’ necessarily sets rates. He knows that, operationally, US Treasury securities function as interest rate support, and not to fund expenditures. He knows it all!

Carmen, Vince, please come home! I hereby offer my personal amnesty- come clean NOW and all is forgiven! As you well know, coming clean NOW will profoundly change the world. As you well know, coming clean NOW will profoundly alter the course of our civilization!

Carmen, Vince, either you believe in an informed electorate or you don’t!?

(feel free to distribute)

Debt, Growth and the Austerity Debate

By: Carmen Reinhart and Kenneth Rogoff

Congrats!!!

FW from President Gregory Warden:

It is with great pleasure and tremendous pride that I am able to announce that the Swiss University Conference [SUK/CUS], the governing body for higher education in Switzerland, has granted Franklin College Switzerland full university institution accreditation, stating in its recent notification:

We are pleased to inform you of the positive decision made by the SUK [CUS] on April 18, 2013 regarding the accreditation of Franklin College Switzerland as a university institution.

The notice of accreditation went on to state:

The expert team is convinced that Franklin College Switzerland has gone through a major development since the last accreditation. This is largely the result of the realization of the recommendations by the 2005 OAQ expert team. Franklin College Switzerland now is better integrated within the Swiss landscape, as well as being connected within Europe. According to the expert team, it has above all strengthened its research activities. The qualifications and in particular the research activities of the faculty have significantly increased since the last accreditation.

In 2005 the Swiss University Conference granted Swiss university accreditation to all major programs of study leading to the Franklin College Bachelor of Arts degreemaking Franklin the first and only university to receive such recognition. With our new institutional accreditation, it is with even greater pride that Franklin is now the first and only university to have institutional university accreditation in both the United States and Switzerlanda distinction that will serve Franklin and its past and future graduates well.

In the Swiss Center of Accreditation and Quality Assurance in Higher Educations expert team recommendation to the Swiss University Conference they stated that Franklin College fulfills all accreditation standards, making the following statement and recommendation:

Franklin College is an American and private institution of higher education in Europe, and thus it represents a kind of hybrid organization. It has introduced new educational principles into the European setting, it is very international by its course offerings and by its student body, and in its teaching it puts heavy emphasis on the general skills and human values, that are especially appropriate for the 21st century world. Its programs are well linked to meet the current challenges in higher education, also on a global scale. Its teaching methods are innovative and appropriate. The students also have a strong feeling of belonging to the Franklin community. The network of its alumni appears to be very active, spread all over the world. The Franklin graduates appear to be well placed especially in international companies. Its strategic goals appear very appropriate to meet the needs and challenges higher education at large is currently facing at least in Europe, but also globally. The experts group recommends accreditation of Franklin College Switzerland, without conditions.

Everyone associated with Franklin should be very proud of all that has been achieved since it was founded in 1969. This recognition is an affirmation of the quality of the institution as a whole and the hard work and contributions of so many peoplefaculty, staff, students, alumni, parents and trustees. Franklin would not be the special place it is today if it were not for each and everyones efforts on its behalf.

Thank you and best regards,

P. Gregory Warden

President

So some was gross, not net, and some unspent:

Nomura: Asia Insights: China: Why GDP growth has weakened despite strong credit growth

- Economic growth in China has weakened surprisingly despite rapid credit growth in H2 2012 and Q1 2013.

- We believe a large part of the new credit supply in Q1 did not go into the real economy. For example, at least 20% of urban construction bond issuance was used to pay off expiring bank loans.

- Recent policy signals suggest credit growth will slow in Q2. We reiterate our view that economic growth will slow in Q2, while the market consensus expects a rebound.

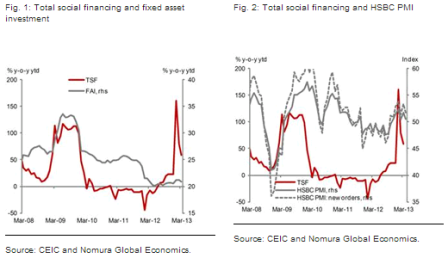

We had expected economic growth in China to rise in Q1 because of very strong credit growth, but GDP growth surprisingly slowed to 7.7% from 7.9% in Q4 2012, and economic activity in Q2 has started on a weak note. This is very different to what happened in 2009, when growth in total social financing picked up from 26.6% y-o-y in Q4 2008 to 114% in Q1 2009 and 121% in Q2 2009, growth in fixed asset investment moved up from 26.8% y-o-y in Q4 2008 to 28.6% in Q1 2009, the HSBC PMI rose to 44.8 from 40.9, and the new orders component in the HSBC PMI jumped to 43.6 from 36.1 (Figures 1, 2 and 3).

But in 2013 it is a very different story. Total social financing rose to an historical high and jumped by 160.6% y-o-y in January and by 58.2% y-o-y in Q1, but fixed asset investment (FAI) growth only picked up slightly to 21.2% y-o-y in January and February, and then slowed to 20.9% in March. GDP growth slowed to 7.7% y-o-y in Q1. The flash HSBC PMI weakened in April despite favorable seasonal factors it has only dropped once in April once during the past seven years. The new orders component of the flash HSBC PMI has dropped as well.

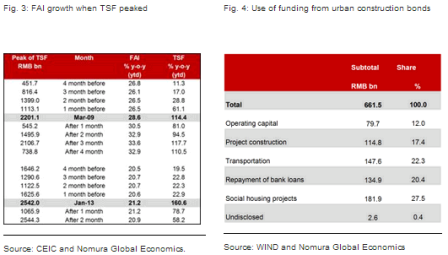

Many investors ask us the same question: where has all the money gone? We believe a large part of the new credit supply in Q1 did not go into the real economy. We do not have comprehensive information, but we provide the following two pieces of evidence. First, we collected public information on the 370 largest issues of urban construction debt that took place in 2012, and found that at least 20% of the money raised was used to repay debt (Figure 4). It is not surprising to us as many infrastructure investments projects are not yet profitable. Therefore, local government financing vehicles need to continue borrowing new funds for debt financing.

Another piece of evidence comes from a recent government policy announcement. According to a Chinese newspaper, First Financial Daily, the National Development and Reform Commission (NDRC) issued a policy notice at the end of March to ensure the funds raised for public housing construction in the bond market are not used for other purposes. We believe this policy may be triggered by cases where some funds were misused. Indeed, risks of such events have been mentioned repeatedly in government documents.

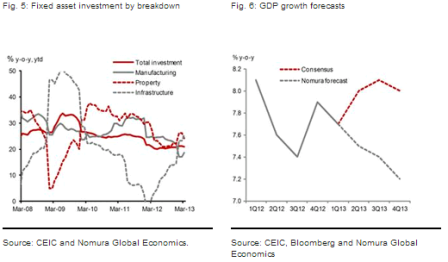

Why didnt money flow into the real economy? We think it is partly because the underlying demand for investment is weak. FAI growth for the manufacturing industry has been on a downward trend since 2011 and dropped sharply in Q1 2013 despite strong infrastructure FAI growth, which should have generated some positive spillover effects for manufacturers (Figure 5). The over-capacity problem in the manufacturing industry has been exacerbated by aggressive policy easing in 2009 and 2012.

We reiterate our view that economic growth will slow to 7.5% in Q2 as credit growth weakens (Figure 6). The consensus expects growth to recover to 8% in Q2, but recent policy signals suggest policy tightening has started and will adversely affect growth. In particular, the government has investigated several high profile corruption cases in the bond market in the past few days, and the Peoples Bank of China held a meeting on 24 April with commercial banks to clean up irregular activities in the bond market, according to a Chinese newspaper Economic Information. This initiative will likely lead to a slowdown in bond issuance and growth in total social financing in the coming months.

Full size image

Full size image

Full size image