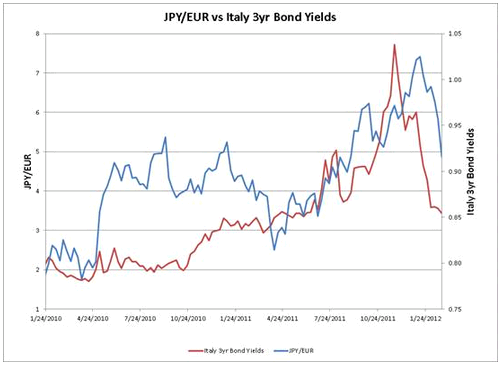

Click here for larger version

Daily Archives: February 27, 2012 @ 3:50 pm (Monday)

LTRO birdie telling me maybe the BOJ gave the nod to its banks

Just a hunch now, but Italian, Spanish, and related bond yields began falling coincident with the first ECB LTRO. The question is why, as I saw no operative channel of consequence from ECB liquidity provision of 3 year funds on a floating rate basis to the term structure of rates.

So it seemed to me that also coincident to the LTRO was some entity giving the nod to its banks to buy those bonds, or some reason sellers of those bonds backed off.

I’m now thinking it may have been the BOJ giving the nod to its member banks to buy euro member debt denominated in euro and keep the fx risk on their books, with the assurance govt policy would keep the yen weak and guarantee the banks an fx profit.

We learned after the fact that Japan had been selling yen well before they announced their new weak yen stance. And having their banks buy euro member euro denominated debt directly weakens the yen vs the euro.

The timing of the events- the LTRO/yen sell off/yen policy change- is close enough to get my attention.

So Japan managed to weaken the yen and firm euro member debt prices all under the cover of the ECB LTRO operation which they gladly allowed to take the credit.

In any case, I don’t expect any more from this next LTRO than I expected from the last, but I am keeping a close eye on the yen.

GEI article is up

Eurozone: How to Drive an Economy in Reverse

By Warren Mosler

February 27 — The situation in Greece brings me back to the conclusion that merely resolving solvency issues in the Eurozone doesn’t fix the economy. Solvency must not be an issue, but if there is negative growth, solvency math simply doesn’t work for any of the Euro members.

Without growth in the Eurozone the resolution (for now) of the Greek crisis will simply result in the focus moving on to one of the next weaker sisters. As this happens the risk remains that other countries in trouble will ask for haircuts on their debt (similar to Greece) as part of their rescue. And that could trigger a general, global, catastrophic financial meltdown.

Follow up:

Monetary and Fiscal Expansion are Needed

My first order proposal remains an ECB distribution on a per capita basis to the euro member nations of maybe 10% of euro zone GDP per year to put the solvency issue behind them. Along with relaxed budget rules, maybe allowing deficits up to 6% of GDP annually, further supported by the ECB funding a transition job at a non disruptive wage to facilitate the transition from unemployment to private sector employment. I might also recommend deficits be increased by suspending VAT as a way to increase aggregate demand and lower prices at the same time.

Alternatively, the ECB could simply guarantee all national government debt and rely on the growth and stability pact for fiscal discipline, which would probably require enhanced authorities.

And rather than trying to bring Greece’s deficit down to current target levels, they could instead relax the growth and stability pact limits to something closer to full employment levels. And, again, I’d look into suspending VAT to both increase aggregate demand and lower prices.

Strong Euro First

However, all policies seem to be ‘strong euro’ first. And the ‘success’ of the euro continues to be gauged by its ‘strength’.

The haircuts on the Greek bonds are functionally a tax that removes that many net euro financial assets. Call it an ‘austerity’ measure extending forced austerity to investors.

Other member nations will likely hold off on turning towards that same tax until after Greece is a ‘done deal’ as early noises could work to undermine the Greek arrangements, and take the ‘investor tax’ off the table.

Like most other currencies, the euro has ‘built in’ demand leakages that fall under the general category of ‘savings desires’. These include the demand to hold actual cash, contributions to tax advantaged pension contributions, contributions to individual retirement accounts, insurance and other corporate ‘reserves’, foreign central bank accumulations of euro denominated financial assets, along with all the unspent interest and earnings compounding.

Offsetting all of that unspent income (private savings) is, historically, the expansion of debt, where agents spend more than their income. This includes borrowing for business and consumer purchases, which includes borrowing to buy cars and houses. In other words, net savings of financial assets are increased by the demand leakages and decreased by credit expansion. And, in general, most of the variation is due to changes in the credit expansion component.

Austerity in the euro zone consists of public spending cuts and tax hikes, which have both directly slowed the economies and increased net savings desires, as the austerity measures have also reduced private sector desires to borrow to spend. This combination results in a decline in sales, which translates into fewer jobs and reduced private sector income. Which further translates into reduced tax collections and increased public sector transfer payments, as the austerity measures designed to reduce public sector debt instead serve to increase it.

Now adding to that is this latest tax on investors in Greek debt, and if the propensity to spend any of the lost funds of those holders was greater than zero, aggregate demand will see an additional decline, with public sector debt climbing that much higher as well.

All of this serves to make the euro ‘harder to get’ and further support the value of the euro, which serves to keep a lid on the net export channel. The ‘answer’ to the export dilemma would be to have the ECB, for example, buy dollars as Germany used to do with the mark, and as China and Japan have done to support their exporters. But ideologically this is off the table in the euro zone, as they believe in a strong euro, and in any case they don’t want to build dollar reserves and give the appearance that the dollar is ‘backing’ the euro.

Three Reverse Thrusters in Use

This works to move all the euro member nation deficits higher as the ‘sustainability math’ of all deteriorate as well, increasing the odds of the ‘investor tax’ expanding to the other member nations – and that continues the negative feedback loop.

Given the demand leakages of the institutional structure, as a point of logic, prosperity can only come from some combination of increased net exports, a private sector credit expansion, or a public sector credit expansion.

And right now it looks like they are still going backwards on all three. And with the transmission in reverse, pressing the accelerator harder only makes you go backwards that much faster.

Someone is still worried about the US becoming the next Greece

Sorry to see this happen.

Whatever.

First, it’s not a debt burden.

Debt management is just shifting $ between Fed reserve accounts to Fed securities accounts.

Second, the trick is for a given size govt to keep taxes at the right level.

Yes, some day circumstances could possibly warrant much higher taxes, though in my 40 years of experience I’ve never seen excess demand. But yes, anything is possible. And a bit of forecasting of demand leakages along with deficits might be at least somewhat enlightening, and if history is any guide, probably show future deficits still aren’t large enough for full employment.

But even if you know you have to make a turn 20 miles down the road- that is, even if you do know that 20 years from now aggregate demand could be too high- you don’t turn the wheel now.

Can America Become the Next Greece?

By John Carney

February 27 (CNBC) — When conservatives worry about the size of the federal government’s budget deficits and the national debt, liberals tend to point out that “America is not Greece.”

This is certainly true. The U.S. economy is far healthier than the economy of Greece. We aren’t locked into a currency union that deprives us of monetary flexibility. Our government can never run out of money to service its debt because the debt is denominated in currency the government creates.

The most important difference between the U.S. and Greece, however, is not where we are in our economic cycle or our monetary system.

It’s the gap between the productivity of the American economy and the Greek economy.

The core reason why Greece is unable to service its debt without aid from its neighbors is that its economy does not generate enough wealth. Even if Greece somehow put an end to the habitual tax-avoidance of its people, it could not service its debt without truly impoverishing its citizens through unsustainable wealth confiscation.

The dearth of productivity and competitiveness explains, ironically, why Greece’s debts got so large to begin with. It’s people and government wanted to live beyond their means, to spend more than they produced. This is only possible if someone is willing to lend you the money to buy the excess goods and services.

Most Greeks never really realized how unproductive their economy had become. In some sense, access to debt had concealed their long-running economic slump. It seemed that things were humming along just fine.

This is one of the reasons Greeks are so shocked by what is being required by their creditors. It feels as if they are being looted, bossed around, sent orders from German and French bureaucrats. The Greeks just never internalized how dependent their economy had become on the capacity and willingness of more productive economies to lend to them.

The productivity gap, of course, is not the result of nature or the wrath of some angry gods. It is the result of years of policies that made investing in productivity — both through capital investment and increases in skills — irrational. The generosity of the Greek government and the regulatory burdens placed on businesses made the relative rewards from business investment meager.

This is important to keep in mind when considering the proposition that “America is not Greece.” It tells us we must zealously guard our productivity, protect our culture of competition and enshrine market processes almost as if they were the gifts of benevolent gods.

America is not Greece. But if our productivity is sapped by too much regulation, by misbegotten monetary policy, by taxes that undermine incentives to earn, or by government spending that rewards business meeting political rather than market demand, we can become Greece.

America can never be forced to default for lack of money. But our debt burden can become unsustainable — requiring either inflation or voluntary default — if our productivity does not improve as our debt grows.