interesting:

Occupy Brussels…

EU Staff Threaten Strike Action Over Belt-Tightening

BRUSSELS (AFP)–European Union staff unions on Friday threatened strike action next week to protest belt-tightening measures as the bloc goes on an austerity diet.

A statement from an “Inter-institutional Joint Front” representing the 55,000 staff across the European institutions has called an assembly on Tuesday following a breakdown in conciliation talks with the European Commission.

European staff wages vary widely: from EUR2,650 per month before tax and social welfare payments, to EUR23,000 gross for each of the 27 national EU commissioners.

Staff are concerned by a bid to overhaul staff rules and by a letter signed by 17 of the 27 EU states that criticizes automatic wage adjustments and links the possibility of wage hikes to the economic situation.

The 17 austerity-driven nations also say an increase in retirement age from 63 to 65 isn’t sufficient.

Staff unions on the other hand criticize working conditions on their Facebook page

In this case default = EU sanctioned debt forgiveness,

which, at this point in time, only reinforces the notion that

no one with any fiduciary responsibility should be buying any euro member debt.

This shortens the time frame between now and when things get bad enough for

Germany to permit the ECB to do what it takes to get past the national govt solvency issue.

Germany confirms it is considering more eurozone “orderly defaults”

Berlin/Brussels (DPA) — The German Foreign Ministry on Friday confirmed that Germany was considering the possibility of more eurozone “orderly defaults” beyond that of Greece, as suggested by a paper leaked by the British press.

The Daily Telegraph published a six-page document, attributed to the Foreign Ministry, suggesting that partial bankruptcy must be made possible for all euro members “unable to achieve debt sustainability.”

“There must also be the option of an orderly default (of a struggling euro member) to reduce the burden on taxpayers” in other eurozone members which are paying for its bailout, the document said.

“There is nothing secret about it,” the ministry said Friday, stressing that it contained ideas on which Foreign Minister Guido Westerwelle had already publicly commented upon.

At the start of the euro debt crisis, EU leaders maintained that no country would ever fail to pay back debts. This year the taboo was broken with Greece, as private lenders were ordered to take a 21 per cent hair cut on Greek bonds. The figure was then raised to 50 per cent.

The memo proposed that “orderly default” procedures should be governed by the European Stability Mechanism, the new euro rescue fund which, under current plans, is due to enter into operation in 2013.

The paper also backed strong EU interference in the economic affairs of eurozone budget sinners, proposing that a country not meeting austerity targets could “have concrete budgetary measures imposed upon it,” such as “specific spending cuts” or new taxes.

But commenting on Dutch proposals to create an EU commissioner with direct powers of intervention in national budgetary policies, it warned that “the constitutional provisions on the budgetary autonomy of the Bundestag (German parliament) must be observed in every case.”

Recalling well-known German positions, the document called for EU treaty changes to implement the budget discipline reforms it advocated, which also include the possible freezing of EU regional aid and taking budget sinners before the EU Court of Justice.

But it also accepted that such course of action may not be possible.

“In case (an EU treaty change) is not politically feasible, an alternative treaty between the member states that is legitimate under international law ought to be considered,” it said.

Good to see Dirk at Goldman is pretty much spot on:

German Economic Commentary : Chancellor Merkel not keen on more a proactive ECB stance

Published November 18, 2011

Chancellor Merkel gave a speech in Berlin yesterday where her main message with respect to stabilisation measures was essentially: No! Merkel rejected the introduction of Eurobonds but also any commitment from the ECB’s side to be the lender of last resort for Euro-zone governments.

There are several arguments the German government/Bundesbank are putting forward against a more pro-active stance of the ECB. First, a more pro-active role would not be in accordance with the treaties. Second, it would create moral hazard as it would reduce the incentive for governments to consolidate and reform. Third, debt monetisation, sovereign debt purchases by the ECB, leads to inflation. The latter argument was echoed by the chairman of the council of economic experts Franz, who said in an interview with FAZ newspaper that debt monetisation is a “deadly sin” for a central bank.

These are valid arguments, but only up to a point. In particular the worries about the inflationary impact of debt monetisation are exaggerated. Sovereign debt purchases of a central bank do not necessarily lead to inflation (see the example of Japan, although it can, see the example of Zimbabwe). It can lead to inflation if these purchases are used to finance an expansionary fiscal policy that will lead to strong growth and demand outpacing supply such that price setters will increase their prices. Fiscal policy, however, will be quite restrictive in the Euro-zone in the coming years. Italy, for example, aims at tightening fiscal policy by almost 3% next year on our estimate (we calculate this as the change in the structural primary fiscal balance). And while it remains to be seen whether the fiscal targets will be met, it is a safe bet that fiscal policy will not be expansionary in the Euro-zone for quite some time.

It can also lead to inflation if there is an excessive debt overhang, i.e. the fiscal position of a country is clearly unsustainable. Put differently the expansion of the monetary side is, even in the long run, not backed by a similar expansion of the real side of the economy. As we have argued in the past we see this only as a remote risk.

What the ECB is currently doing under its SMP is essentially swapping one savings instrument (peripheral sovereign debt) for another (cash) as private sector investors, for various reasons, no longer want to hold peripheral debt. But this has no inflationary implications unless one assumes that investors are spending the cash thereby stimulating demand which then leads to inflation. But these investors are not holding cash because they want to increase their spending, but because they think, rightly or wrongly, that cash is more rewarding from an investment point of view.

There are no easy choices and it would have been, no doubt, better if the ECB had never got in the position it is in now. But the current situation demands a careful weighing of the risk involved with any decision taken. The inflationary risk thereby seems to be getting an unduly high weight in the consideration of German policy makers.

Dirk Schumacher

Not long ago France would have conducted a nuclear test to make the point.

Today, it takes a core meltdown to make the point:

Franco-German Spat on Role of ECB Renewed

By Tony Czuczka and Mark Deen

November 18 (Bloomberg) — The failure of European leaders to end the debt crisis with their broadest effort yet has revived a Franco-German dispute over theEuropean Central Bank’s role and fueled investor concerns over policy makers’ economic impotence.

ECB chief Mario Draghi today slammed governments for failing to implement policy commitments as holders of Greek debt began talks in Athens on structuring a 50 percent writeoff that was the cornerstone of a deal pieced together last month at an all-night summit. Officials in Berlin and Paris yesterday swapped barbs and European borrowing costs outside of Germany rose to euro-era records.

The discord highlighted markets’ brushoff of a package that included a scaled-up rescue fund, proposed guarantees of sovereign debt and a bid to attract more international loans. The accord, which finance ministers aim to implement next month, was at least the fourth plan billed as a comprehensive strategy to end the crisis born in Greece in 2009, none of which provided a lasting fix.

“Where is the implementation of these long-standing decisions?” Draghi said in a speech in Frankfurt today. “We should not be waiting any longer.”

Stocks slid, dragging the MSCI All Country World Index to a six-week low. The Stoxx Europe 600 Index decreased 0.7 percent. The premium France pays over Germany to borrow for 10 years jumped to a record 200 basis points yesterday, as yields on bonds of countries from Portugal to Finland, the Netherlands to Austria also rose relative to Germany.

Due to popular demand, I’ve begun outlining a Greek exit strategy to exit the euro currency,

and instead use its own new currency to provision itself:

1. The Greek government would announce that it will begin taxing exclusively in the new currency.

2. The Greek government would announce that it will make all payments in the new currency.

That’s it, deed done!

The govt can now provision itself and continue to function on a sustainable basis.

Now some Q and A:

Q. How will the new currency exchange for euro?

A. The new currency will be freely floating, with exchange between willing buyers and sellers at market prices.

Q. What about the existing euro debt?

A. Announce that it will consider it on a ‘when and if’ basis with no specific payment plans.

Q. What about existing govt contracts for goods and services?

A. They will be redenominated in the new currency.

Q. What about euro bank deposits and euro bank loans?

A. They remain in place.

Q. What about foreign trade?

A. Markets forces will function to adjust the trade balance to reflect foreign desires to accumulate financial assets denominated in the new currency.

To maintain full employment and internal price stability, I would further recommend the following:

1. The govt would fund a minimum wage job for anyone willing and able to work.

2. For any given size government, taxes should be adjusted to ensure the labor force that works for that minimum wage be kept to a minimum.

3. I would recommend the govt levy only a tax on real estate for the following reasons:

a. Compliance is maximized and compliance costs and related issues are minimized- if the

tax isn’t paid the property can be simply sold at auction.

b. Everyone contributes as either an owner of the property or as a renter as the owner’s costs

are ultimately passed through to renters.

c. Transactions taxes are eliminated, thereby removing those restrictions on transactions.

Freedom to transact is the source of that substantial contribution to real wealth.

4. A zero rate policy where govt deficit spending remains as non interest bearing balances held by counter parties at the Bank of Greece, and no govt securities are permitted.

5. All bank deposits in the new currency will be fully insured by the govt.

6. Banks will be govt regulated and supervised, which will include a 15% capital requirement, govt guaranteed liquidity, and a prohibition from any secondary market activity.

Comments welcome with additional questions, thanks!

And this Fed fears deflation a lot more than inflation:

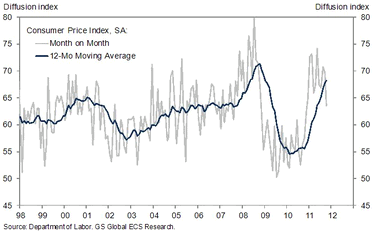

- We see signs that the upside inflation surprises of 2011 have ended. Our new statistical summary of the price components of business surveys such as the ISM, Philly Fed, and NFIB points to decelerating inflation. In addition, our unweighted CPI diffusion index, which measures the breadth of price changes across 178 detailed price categories, fell to its lowest level since late 2010.

Inflation has been above our expectations in 2011, but we expect a substantial part of this surprise to reverse and see core inflation clearly below the Fed’s “mandate-consistent” level of 2% or a bit less by the end of 2012. The reasons are straightforward. There is still a large amount of slack in the US economy; nominal wage inflation remains very low; and much of the inflation pickup of 2011 can be traced to temporary factors such as short-term commodity price pass-through and upward pressure on motor vehicle prices in the wake of the Japanese earthquake. (We do not expect a full reversal of the core inflation pickup because the increase in rent inflation is likely to be more persistent.)

The recent inflation data have started to look more consistent with our view of moderating core inflation. The consumer price index (CPI) excluding food and energy has risen at an annualized rate of just 1.2% over the past two months, the lowest rate since December 2010 Statistically based measures of core inflation such as the Cleveland Fed’s weighted-median and 16% trimmed-mean CPI send a similar message.

Our unweighted CPI diffusion index is also starting to look a bit more benign again. It is constructed by seasonally adjusting all 178 individual CPI categories for which we have sufficient data, calculating the month-to-month change, and then reporting the percentage of categories showing price increases plus half the percentage showing no change. That is, values above 50 indicate that more categories are seeing price increases than decreases; the higher above 50, the greater the breadth of price increases relative to price decreases. (We perform our own seasonal adjustment because the Labor Department only provides seasonally adjusted CPI data for a subset of product categories.) Exhibit 1 below shows our diffusion index. While it is still clearly above the levels of 2009 and 2010, the October 2011 reading was the lowest since November 2010.

Exhibit 1: CPI Diffusion Index Has Started to Slow

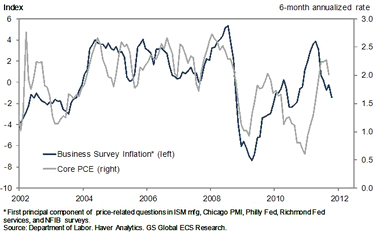

To gain more insight into future inflation trends, we have constructed a new measure that summarizes the inflation signal from various business surveys. Specifically, we calculated the first principal components of the price-related questions in the monthly ISM, Chicago PMI, Philly Fed, NFIB, Kansas City Fed, and Richmond Fed business surveys. These questions refer to prices paid, prices received, or wages and salaries and are generally reported as the difference between the percentage of respondents saying that prices rose in the survey month and the percentage saying that prices fell. (Focusing only on prices paid or prices received indexes does not make a significant difference to the results.)

The results are shown in Exhibit 2 below. In general, our business survey indicator of inflation tracks the ups and downs of the core PCE index–the Fed’s favorite measure of underlying inflation–reasonably well. After a significant acceleration in early 2011, the indicator has declined notably in recent months and is now consistent with a deceleration in core PCE inflation from the recent 2%+ level to somewhere closer to 1.5%. This is also consistent with our forecast that inflation will slow over the next year.

Exhibit 2: Business Survey Inflation Shows Recent Deceleration

With the Republicans now willing to hike taxes out of fear of becoming the next Greece, the odds of the super committee going super big are increasing.

“America has crossed an unthinkable threshold: our national debt now exceeds $15 trillion dollars. That’s more than $48,000 per citizen,” Republican National Committee (RNC) Chairman Reince Priebus said. “In 2009, President Obama promised to cut the deficit in half by the end of his first term. Instead, he further accelerated its growth, producing three years of record deficits.”

SINGAPORE OCT NON-OIL DOMESTIC EXPORTS -5.9 PCT S/ADJ MONTH-ON-MONTH; REUTERS POLL +1.6 PCT

SINGAPORE OCT NON-OIL DOMESTIC EXPORTS TO US FALL 50.6 PCT Y/Y; NON-OIL DOMESTIC EXPORTS TO EU FALLS 30.9 PCT Y/Y

SINGAPORE OCT NON-OIL DOMESTIC EXPORTS -16.2 PCT FROM YEAR AGO; REUTERS POLL -8.0 PCT