>

> (email exchange)

>

> On Sat, Nov 6, 2010 at 7:10 AM, wrote:

>

> The yield spreads on Irish and Spanish bonds are blowing out even as we speak, as

> well as those on the rest of the periphery. While all eyes are on the Fed, the real action

> may be in Europe.

>

Agreed! The question remains, is the ECB still there to backstop short term funding. So far seems yes.

It’s entirely a political decision. Think of the euro zone as an under water city, with the ECB controlling the air supply.

Also, I like the next chart. A 9% federal budget deficit is so far been enough to muddle through with very modest GDP growth and stabilize employment, albeit at very low levels. With a proactive fiscal adjustment, it doesn’t get much better until consumer credit expansion kicks in, which could be quite a while.

It also looks to me like a dollar rally that will revive deflation fears might still be in the cards, as it’s been sold mainly based on a misunderstanding of QE.

A Few Thoughts on the Employment Numbers

By Dr. Lacy Hunt, Hoisington Investment Mgt. Co.

The October employment situation was dramatically weaker than the headline 159k increase in the payroll employment measure. The broader household employment fell 330k. The only reason that the unemployment rate held steady is that 254k dropped out of the labor force. The civilian labor force participation rate fell to a new low of 64.5%, indicating that people do not believe that jobs are available, but this serves to hold the unemployment rate down. In addition, the employment-to-population ratio fell to 58.3%, the lowest level in nearly 30 years.

While not actually knowing what happened to the net job change in the non-surveyed small business sector, the Labor Department assumed that 61k jobs were created in that sector. This assumption is not supported by such important private surveys as those from the National Federation of Independent Business or by ADP. Just a month ago the Labor Department had to revise downward the job totals due to a serious overcount of their statistical artifact known as the Birth/Death Model.

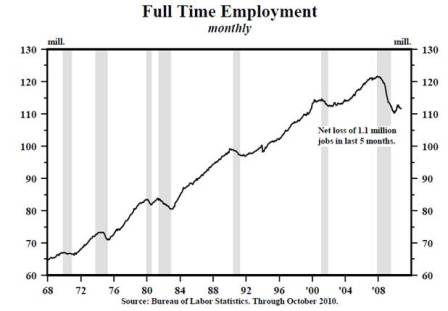

The most distressing aspect of this report is that the US economy lost another 124K full-time jobs, thus bringing the five-month loss to 1.1 million in this most critical of all employment categories. In an even more significant sign, the level of full-time employment in October was at the same level that was reached originally in December 1999, almost 11 years ago (see attached chart). An economy cannot generate income growth by continuing to substitute part-time work for full-time employment. This loss of full-time jobs goes a long way to explain why real personal income less transfer payments has been unchanged since May.

The weakness in real income is probably lost in an environment in which the Fed is touting the gain in stock prices and consumer wealth resulting from the latest quantitative easing (QE), but QE has unintended negative consequences for real household income. Due to higher prices of energy and food commodities, QE may result in less funds for discretionary spending for consumers whose incomes are stagnant. Also, with five-year yields falling below 1%, rates on CDs and other types of short-term bank deposits will decline, also cutting into household income. At the end of the day these effects will be more powerful than any stock-price boost in consumer spending, which, as always, will be very small and slow to materialize.

To have a broad-based recovery, the manufacturing sector must participate. Contrary to the ISM survey, manufacturing jobs fell 7k, the third consecutive drop, resulting in a net loss over the past three months of 35k.

In summary, the latest economic developments indicate a slight worsening of underlying fundamental conditions.